Select your asset manager investment wisely if you are remotely considering investing in an asset manager!

On September 27, I published my Consider Investing In Asset Managers post in which I disclosed exposure to BlackRock (BLK), Brookfield (BAM.to and BN.to), and Blackstone (BX).

My rationale for investing in these firms is that I want private equity and private credit (PE) exposure. I am not, however, prepared to invest directly in any of their portfolio companies.

In that September 27 post (and prior asset management related posts), I state that industry consolidation is inevitable. This is borne out in PwC’s ‘2023 Global Asset and Wealth Management Survey‘ wherein it is estimated that 1 in 6 asset and wealth management companies globally are likely to disappear or be acquired by 2027. This is twice the normal turnover rate.

Given the shakeout expected to transpire over the coming years, I choose to limit my exposure to some of the largest publicly listed asset managers. These asset managers have established a reputation that draws investors and investment opportunities. They can enter into transactions most asset managers can not even entertain.

If anything, these asset managers stand to benefit from industry consolidation.

In this post, I provide additional context as to why you must select your asset manager investment wisely.

Industry Outlook

In 1980, there were ~24 PE funds. This increased to ~6,600 with the onset of a low interest rate environment around the beginning of the 2010s. By 2022, there were 17,000+ PE firms in the US. To put things in perspective, PE firms collectively managed ~$579B of assets under management (AUM) in 2000. By 2022, this figure had surged to ~$7.8T.

As noted above, my exposure to asset managers is currently limited. All 3 firms noted above are massive.

- BLK recently released its Q3 2024 results and disclosed it has ~$11.5T in assets under management (AUM).

- BAM.to and BN.to and BX each have in excess of $1T of AUM and their plans are to double AUM over the next few years.

These are great asset managers. In an industry with over 17,000 PE firms, however, many will undoubtedly be ‘trash bins’.

PE Backed Companies Face More Defaults And Liquidity Stress Ahead

On October 10, 2024, Moody’s released its report stating that PE portfolio companies have defaulted twice as much as speculative-grade issuers without a PE presence since 2022. Most defaults were distressed exchanges and some were re-defaulters!

The following are from Moody’s report.

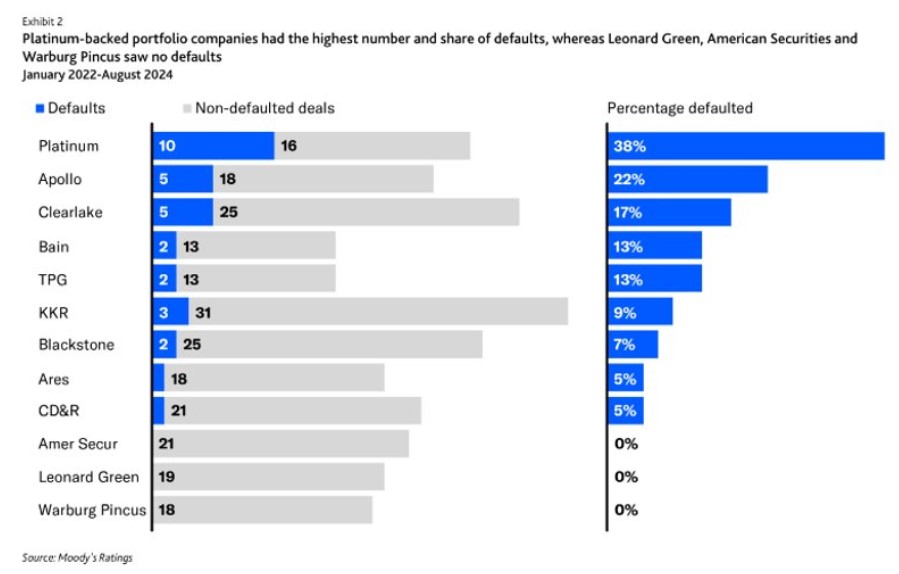

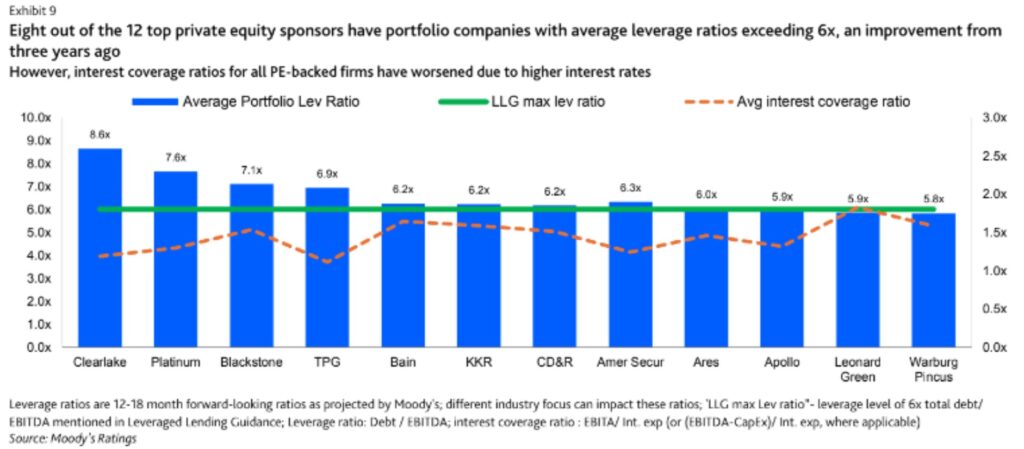

Imagine investing in one or more of Platinum’s, Apollo’s, or Clearlake’s funds.

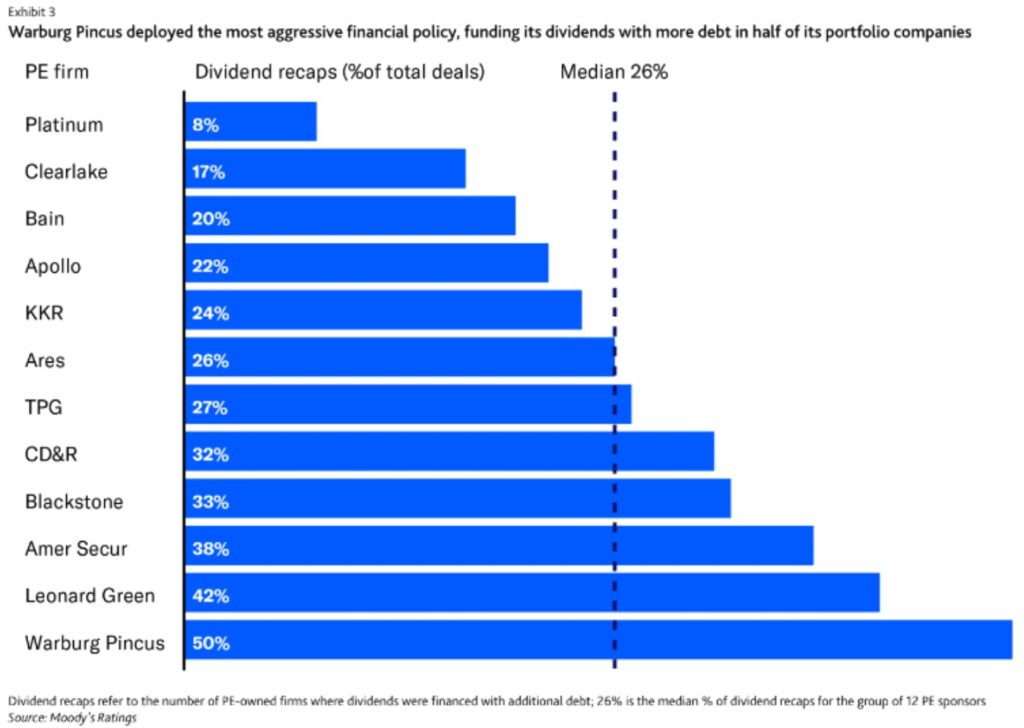

Some asset managers have paid out debt-funded dividends to their equity holders in 2020 – 2024. This dividend recapitalization process is one in which a company incurs new debt in order to pay special dividends to private investors or shareholders. The money sucked out of the portfolio company increases the interest payment obligation at the expense of reinvesting in the business for growth.

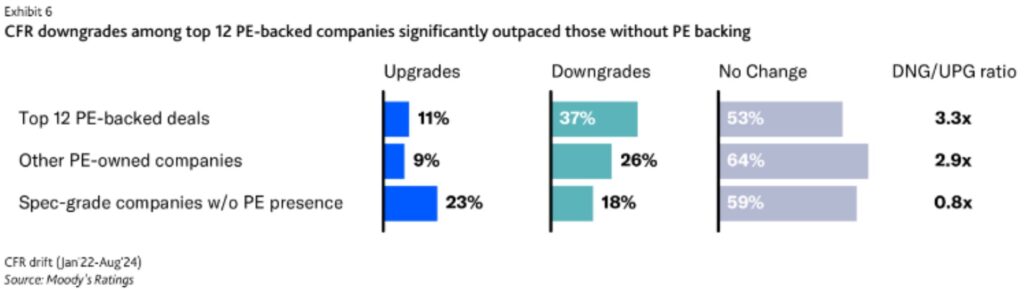

Moody’s analysis also found that in the two years to August 2024, portfolio companies of the top dozen buyout groups defaulted at a rate of 14.3%. This is twice as high as that for companies not backed by private equity.

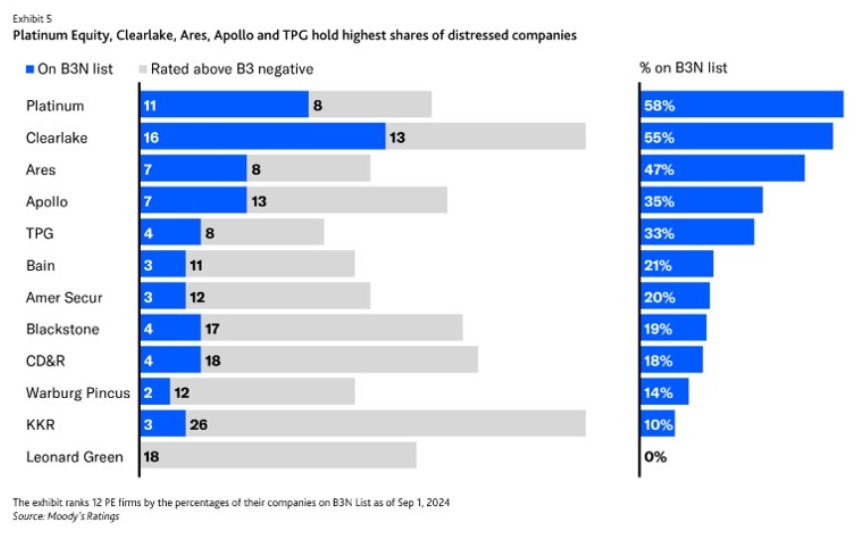

Platinum and Clearlake are not alone. Apollo Global and Ares Management have also had less than stellar buyouts. Nearly 25% of the Apollo-owned companies that Moody’s rates have defaulted since 2022 and ~47% of Ares-backed companies analyzed by Moody’s are distressed.

The rapid increase in interest rates decimated valuations that had soared during the pandemic. Balance sheets of thousands of highly leveraged private equity-backed companies were hammered. For example, in January 2022 – August 2024, more than 33% of the Platinum-owned companies rated by Moody’s underwent restructuring or a debt default. Clearlake’s portfolio fared better as ‘only’ ~17% suffered the same outcome.

Some PE firms, Clearlake is one example, have become an active user of ‘continuation funds’. This is when the group sells the company to itself and other investors.

Rating Agency Challenges

I analyze financial statements before investing in a company to determine whether the company satisfies my risk tolerance. Nevertheless, I also look at how the rating agencies perceive a company’s credit risk to determine if our respective assessment is similar.

I do not invest in any PE funds because I know I could not properly determine the risk of the underlying companies. It appears that I am not alone in this regard. The fast-growing market for private credit has complicated matters for rating agencies since such loans are more difficult to track an analyze than more traditional forms of borrowing.

Julia Chursin, VP at Moody’s, recently indicated:

Private credit can mask some issues in a PE firm’s portfolio. There could be some opaque credit risk which is absorbed by the private credit sector, although they claim they only pick good ones.

Final Thoughts

BX has portfolio companies with 7.1x total debt/EBITDA. I do not think the hundreds of portfolio companies are all this highly leveraged, however, otherwise S&P Global and Fitch would not assign A+ ratings to BX.

BLK and Brookfield also maintain investment grade ratings.

Perhaps I could earn higher rates of return were I to invest directly in some of the portfolios of these asset managers. I, however, do not have the risk tolerance required to do so and am prepared to forego the potential additional upside.

In a universe of 17,000+ asset managers, there will inevitably be great and horrible industry participants. Be sure to select your asset manager investment wisely if you decide to invest in an asset manager,

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long BLK, BX, BN.to and BAM.to.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.