In prior BlackRock (BLK), Blackstone (BX), and Brookfield (BN.to and BAM.to) posts accessible through the Archives section of this site, I touch upon why you should consider investing in asset managers.

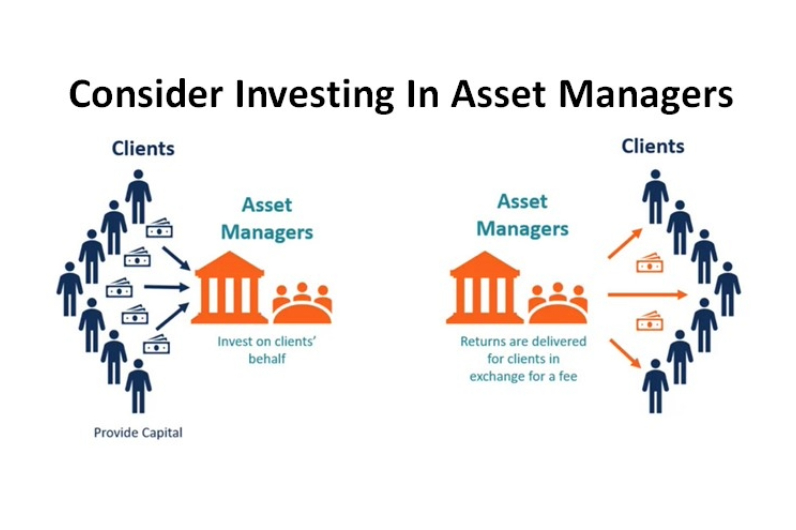

What Are Asset Managers?

In September 2024, KKR (a leading global investment manager) published an excellent perspective of the past, present, and future of the industry. Based on its 48 years of experience in the Alternative Asset space, KKR concludes that:

each asset class has unique characteristics in terms of expected return, risk, yield, liquidity, and capital requirements that require a closer look to better understand the different benefits that each asset class can bring to a portfolio. Some of the asset classes may serve more of a growth and capital appreciation purpose, while others may protect portfolios against inflation and/or provide stable income. Some strategies may offer a combination. Moreover, the spectrum of characteristics is wide and getting even wider, as the industry finds new ways to deliver value to its end-users, many of whom are looking for approaches to ensure a heightened sense of retirement security. Against this backdrop, we think that sharpening one’s understanding of portfolio construction with and without Alternatives as well as across the different categories of such investments is increasingly essential to delivering robust performance outcomes in the years ahead.

We can not, therefore, treat all alternative asset investments equally. One alternative asset may be suitable while another is not.

Before proceeding further, I stress that most alternative asset investments are illiquid. It is, therefore, essential that any commitment be below one’s liquidity needs… and with a healthy margin of safety.

Industry Growth Potential

In 2018, this industry had ~$9T of assets under management (AUM). This grew to ~$15T in 2022 which is less than ~11% of total global GDP and ~2.4% of total global financial assets. Estimates suggest this industry could grow to more than $24T AUM in 2028. Even if these estimates are overstated by ~$4T, there is still ample growth opportunity.

Despite this growth potential, the asset management industry is extremely competitive and a shakeout is occurring.

In July 2023, PwC released the findings of its ‘2023 Global Asset and Wealth Management Survey‘. One of the PwC’s conclusions is that ~1 in 6 asset and wealth management companies globally are likely to disappear or be acquired by 2027. This is twice the normal turnover rate!

Given this, it is imperative we ‘hitch our wagon to the right horse’.

Why I Invest In Asset Managers

An alternative asset is a financial asset that does not fall into one of the conventional investment categories. The list includes:

- private equity or venture capital;

- hedge funds;

- managed futures;

- art and antiques;

- commodities;

- cryptocurrencies;

- derivatives contracts; and

- real estate.

I have no desire to invest in the first 7 alternative assets listed above. Secondly, we sold our investment properties a few years ago to simplify our affairs. Given the current real estate market conditions in many parts of Canada, I strongly suspect many real estate investors wish they had exited their holdings at least a couple of years ago.

I still want alternative asset exposure, however, and thus choose to invest in asset managers through the ownership of their common stock.

Although I could invest in their funds, I choose not to because investments can go horribly wrong.

- BX was forced to limit redemptions in recent years when investors scrambled to exit their alternative asset investments.

- BAM.to defaulted on several hundred million dollars of office building mortgages.

Imagine having invested directly in these particular funds!

Remember that most alternative assets managed by these asset managers are illiquid in nature. Generally, the plan is to exit the investment – often 5 – 10 years later. Much can happen in this time frame!

What may have appeared to be a good acquisition in a very low interest rate environment can turn ugly in a rising interest rate environment. Some companies become saddled with having to shovel cash into debt payments thus leading to some private equity clients pressing to receive their long-delayed payouts.

Financial engineering can only go so far. Lately, it has not been working as well as it once did. Asset managers are increasingly having to adopt a more hands-on approach. This sometimes means having to build 5- and 10-year strategic growth plans for the companies they own and sometimes having to help them market and sell products.

Another concern is when an asset manager decides to load up one of its acquisitions with debt for the purpose of returning cash to investors.

Some recent large debt-funded dividend payouts by a private equity firm include payouts related to office supply store Staples, European home security giant Verisure and railroad Genesee & Wyoming.

Belron is another recent example.

This is the world’s biggest windshield repair company. It owns the Safelite brand in the US and Autoglass in the UK and is half owned by listed Belgian conglomerate D’Ieteren Group.

Discussions with lenders are currently underway to raise €8.1B through new bonds and loans. If negotiations are successful, it would be one of the largest debt-fuelled dividend payouts in private equity history. The plan is to use the cash to pay a €4.4B dividend to an investment group that includes Clayton, Dubilier & Rice and Hellman & Friedman, BlackRock and GIC, and the Singaporean sovereign wealth fund.

This debt-funded dividend payout comes at a time when buyout groups are struggling to return cash to their investors. This struggle is the result of the sluggish pace of mergers and acquisitions and lacklustre flotation prospects that limit the ability to exit investments.

Should negotiations lead to the intended dividend distribution, Belron’s overall debt will nearly double from less than €5B to almost €9B. According to S&P Global, the ratio of Belron’s debt to EBITDA will jump to about 5.8 from 3.3 in 2023.

While investors will receive 35% of their original capital returned through dividends without having sold down any of their investment, this still leaves 65% to be recouped. Belron, however, will be a much weaker company!

Final Thoughts

I have ZERO appetite to invest in the alternative assets listed earlier.

Furthermore, I do not have the intestinal fortitude to invest directly in funds managed by asset managers.

Some private equity investments will be a ‘home run’, others will generate the projected returns, and others will fall short. I don’t want to find out the hard way that I invested in a fund where the returns fall short.

In addition, if I were to invest directly in a particular fund, I might be able to withstand a delayed payout. I can’t say the same for the other investors who invest in the same fund as me. I do not want exposure to a fund with panicking investors.

As noted in prior asset manager posts, I have no idea what investments are held in the various funds. I am essentially ‘flying blind’ when I invest in asset managers, and therefore, want diversified exposure.

By investing directly in BLK, BX, BN.to, and BAM.to, I benefit from the fee structure; asset managers generate fees even when a fund’s return falls short of the target return!

The asset management industry is expected to experience a shake-out over the coming years. I, therefore, limit my exposure to asset managers that can participate in transactions most industry participants can not possibly entertain. Although I do not have exposure to KKR & Co. (KKR) and Apollo Global Management (APO), they are two asset managers in which I would consider having exposure.

When I completed my 2024 Mid Year FFJ Portfolio Review, BX was my 11th largest holding, BLK was my 21st largest holding, and BAM.to/BN.to (combined) were my 23rd largest holding; I do not know their current ranking unless I perform a similar analysis. In my August 8, 2024 Brookfield Asset Management Exposure Increased post, however, I disclose the purchase of an additional 500 shares at CDN~$53.814. I suspect these asset managers are now all amongst my top 20 holdings.

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long BLK, BX, BN.to, and BAM.to.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation. I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.