On August 1, 2024, Amazon (AMZN) released its Q2 and YTD2024 results. I have never invested in AZMN but negative investor sentiment has prompted me to review its results to determine whether I should initiate a position.

Based on my analysis I conclude this post explaining why I am not initiating an Amazon position.

Business Overview

You are undoubtedly familiar with AMZN, and therefore, I dispense with a review of the company. A better source of information about the business and risks is the 2023 Form 10-K.

Financials

Q2 and YTD2024 Results

Material related to AMZN’s Q2 and YTD2024 earnings release is accessible here.

The difference between AMZN’s current assets and current liabilities is ~$15.135B at the end of Q2 2024. This seems light for a company that generated revenue of $291.290B in the first half of FY2024. There is, however, ~$16B of unearned revenue reflected as a current liability. These funds have been received in advance of AMZN providing/delivering a service. As the services are provided, a portion of this unearned revenue is reflected as income and is deducted from the current liability section of AMZN’s Balance Sheet.

A portion of AMZN’s other long-term liabilities also includes unearned revenue. The following explanation of unearned revenue is found on page 9 of 51 in the Q2 Form 10-Q.

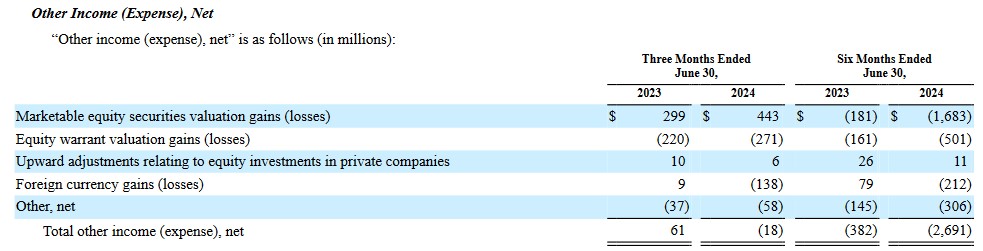

In the first half of FY2024, AMZN reported a ~$2.7B ‘Other Expense, Net’ on its Consolidated Statement of Operations. When looking at the billions of dollars reflected under other line items, we may be inclined to ‘overlook’ ~$2.7B. This, however, has piqued my curiosity.

On page 8 of 51 in the Q2 Form 10-Q we see:

Included in “Other income (expense), net” is a marketable equity securities valuation gain (loss) of $187 million and $391 million in Q2 2023 and Q2 2024, and $(280) million and $(1.6) billion for the six months ended June 30, 2023 and 2024, from our equity investment in Rivian Automotive, Inc. (“Rivian”). As of June 30, 2024, we held 158 million shares of Rivian’s Class A common stock, representing an approximate 16% ownership interest, and an approximate 15% voting interest. We determined that we have the ability to exercise significant influence over Rivian through our equity investment, our commercial arrangement for the purchase of electric vehicles and jointly-owned intellectual property, and one of our employees serving on Rivian’s board of directors. We elected the fair value option to account for our equity investment in Rivian, which is included in “Marketable securities” on our consolidated balance sheets, and had a fair value of $3.7 billion and $2.1 billion as of December 31, 2023 and June 30, 2024.

If you never intended to have Rivian exposure but you invest in AMZN…surprise!

Operating Cash Flow (OCF), CAPEX, and Free Cash Flow (FCF)

AMZN is a highly capital intensive business. In FY2022 and FY2023, for example, net purchases of property and equipment was ~$54B and ~$55B, respectively; these figures include proceeds from property and equipment sales and incentives of ~$5.3B and ~$4.6B. In addition to these net purchases, acquisitions amounted to ~$5.5B and ~$5.9B.

Looking at the Consolidated Statements of Operations, we see Technology and Infrastructure expense in FY2021 – FY2023 totaling $56.052B, $73.213B, and $85.622B.

No matter what statement we look at, AMZN reinvests BILLIONS to grow its business. Reinvesting in the business is AMZN’s primary means by which it allocates capital.

In the FY2014 – FY2023 time frame, AMZN’s:

- OCF was (in B$) 6.84, 11.92, 16.44, 18.43, 30.72, 38.51, 66.06, 46.33, 46.75, and 84.95.

- CAPEX was (in B$) 4.89, 4.59, 6.74, 11.96, 13.43, 16.86, 40.14, 61.05, 63.65, and 52.73.

- FCF was (in B$) -2.72, -1.34, -4.19, 6.65, 18.34, 24.09, 12.44, 4.89, 3.99, and 43.76.

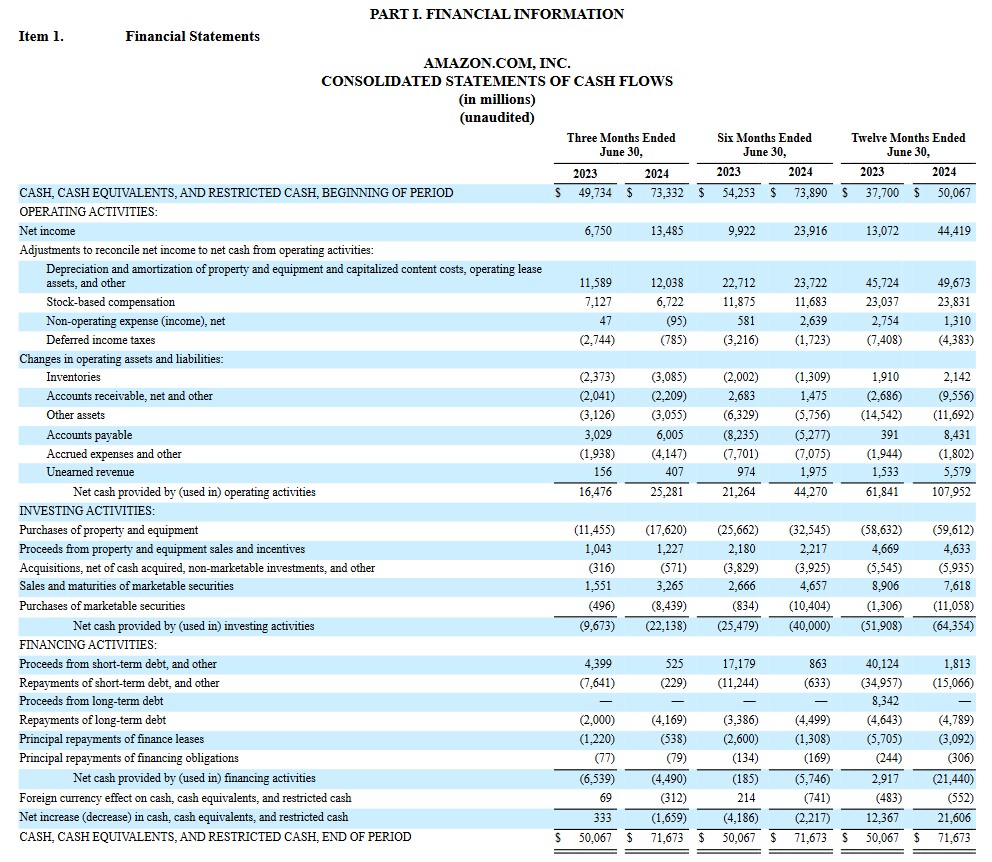

In the first half of FY2024, AMZN generated OCF of ~$44.27B, incurred ~$30.328B of net CAPEX, and generated FCF of ~$13.942B.

Return On Invested Capital (ROIC)

High quality companies often generate a high ROIC. If a company generates a high ROIC, it needs to invest less to achieve a certain growth rate thus reducing the need for external capital.

When a company consistently generates a high ROIC over the long term and it is growing its revenue, it can reinvest a portion of its profits under favorable conditions thereby leading to a compounding effect.

A company that generates $0.15/profit for every $1 invested, for example, achieves a ROIC of 15%. I consider a ~15%+ ROIC to be a reasonable minimum threshold because most of the time, a company’s cost of capital will be lower than this level.

AMZN’s FY2014 – FY2023 ROIC (%) was -0.68, 3.31, 8.42, 7.09, 14.70, 11.72, 14.71, 15.98, -0.60, and 9.82.

AMZN’s ROIC does not consistently exceed my arbitrarily set minimum threshold. There are, however, a sufficient number of ‘pros’ that make it worth considering as a potential investment.

FY2024 Outlook

AMZN does not provide forecasts. On the Q2 earnings call, however, management states:

Looking ahead to the rest of 2024, we expect capital investments to be higher in the second half of the year. The majority of the spend will be to support the growing need for AWS infrastructure as we continue to see strong demand in both generative AI and our non-generative AI workloads.

For the third quarter, specifically, I’d highlight a few seasonal factors to keep in mind.

First, we hosted another successful Prime Day in mid-July. It was our tenth Prime Day and was our largest ever. Prime members globally saved billions of dollars on deals across every product category. From a profitability perspective, we’ve historically seen a headwind to operating margin in Q3 and driven by Prime Day deals as well as the marketing spend surrounding the event.

Additionally, in Q3, we also began to ramp up our capacity to handle Q4 holiday volumes in our fulfillment network. And lastly, we expect an increase in digital content costs quarter-over-quarter from the return of our NFL Thursday night football. We remain heads-down focused on driving a better customer experience, who believe putting customers first is the only reliable way to create lasting value for our shareholders.

Risk Assessment

Some investors fixate on an investment’s potential return and overlook the various risk aspects of the investment to their detriment. This is why I strongly encourage investors to read the ‘Risks’ section of a company’s Form 10-K.

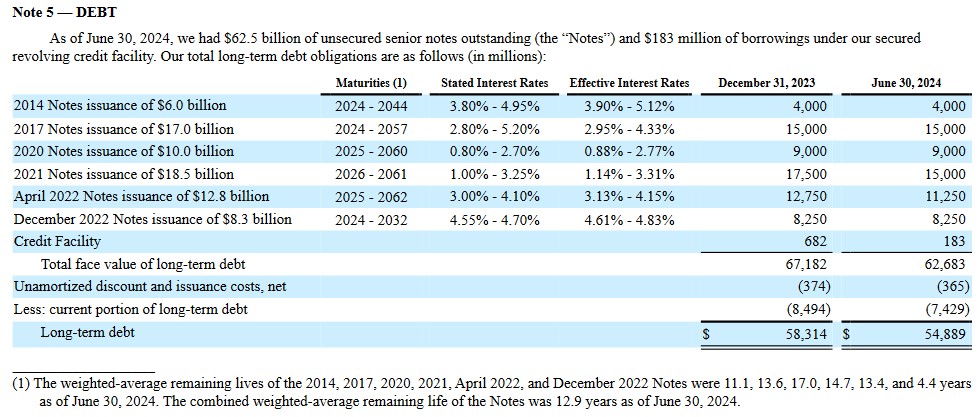

One of the considerations I make in determining if a company is a worthwhile investment is its debt levels and when this debt must be repaid. The following schedule is found on page 15 of 51 in the Q2 Form 10-Q.

Once I have assessed a company’s risk, I look at how the rating agencies perceive a company’s risk.

AMZN’s current domestic long-term unsecured debt ratings and outlook are:

- Moody’s: A1 (stable) last reviewed May 31, 2024. This is the top tier of the upper medium grade within investment grade ratings.

- S&P Global: AA (stable) last reviewed May 31, 2024. This is the middle tier of the high grade within investment grade ratings.

- Fitch: AA- (stable) last reviewed May 31, 2024. This is the bottom tier of the high grade within investment grade ratings.

Moodys’ rating is 2 tiers below that of S&P Global and 1 tier below that of Fitch.

S&P Global and Fitch define AMZN as having as very strong capacity to meet its financial commitments. It differs from the highest-rated obligors only to a small degree.

Moody’s rating defines AMZN as having a strong capacity to meet its financial commitments. It is, however, somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

Capital Allocation

From a capital allocation perspective, companies can:

- distribute dividends;

- repurchase shares; and/or

- reinvest in the business to grow organically and/or make acquisitions.

We know AMZN reinvests heavily to grow the business. Let’s look at how it allocates capital toward dividend distributions and share repurchases.

Dividend and Dividend Yield

AMZN does not distribute a dividend; I envision no change in the foreseeable future.

The weighted average diluted shares outstanding in FY2014 was ~9.3B. In the 3 months ending on June 30, 2024, this has grown to ~10.708B. This increase is because AMZN’s stock based compensation far exceeds share repurchases.

AMZN repurchased ~$0.960B in FY2012, $0 in FY2013 – FY2021, $6B in FY2022, and $0 in FY2023 – YTD2024.

Looking at AMZN’s Consolidated Statements of Cash Flows, stock based compensation in FY2012 – FY2023 was (in $B): $0.833, $1.134, $1.497, $2.119, $2.975, $4.215, $5.418, $6.864, $9.208, $12.757, $19.621, and $24.023. In the first half of FY2024, stock-based compensation was $11.683B and no shares were repurchased.

In February 2016, AMZN’s Board authorized a program to repurchase up to $5.0B of common stock, with no fixed expiration. This was replaced with a $10B repurchase program that the Board authorized in March 2022; this program has no fixed expiration. As of June 30, 2024, AMZN had $6.1B remaining under the repurchase program.

Valuation

AMZN’s FY2014 – FY2023 PE levels are N/A, 951.96, 171.60, 297.58, 84.10, 81.87, 95.23, 65.21, 76.40, and 79.55. N/A is when AMZN reported a loss.

AMZN’s forward-adjusted diluted PE levels using a ~$167.90 share price and the current broker estimates are:

- FY2024: ~35.72 using a mean of $4.70 and a low/high range of $4.10 – $5.49 from 54 brokers.

- FY2025: ~28.7 using a mean of $5.85 and a low/high range of $4.91 – $7.63 from 55 brokers.

- FY2026: ~22.7 using a mean of $7.41 and a low/high range of $5.56 – $8.96 from 29 brokers.

Although some analysts may have yet to update their adjusted diluted EPS estimates, I still think there will be a sizable disparity when all the updates have been made.

AMZN incurs a significant amount of non-cash related expenses annually. I do not, therefore, use GAAP earnings to value AMZN and recommend valuing AMZN using cash flow metrics.

YTD2024, for example, AMZN has incurred almost $50B in depreciation and amortization of property and equipment and capitalized content costs, operating lease assets, and other expenses. In addition, it has incurred ~$23.8B in stock based compensation expenses during the same period. These are non-cash expenses that impact EPS.

In the first half of FY2024, AMZN generated ~$52.6B in FCF (~$108B in net cash provided by operating activities, ~$60B in purchases of property and equipment, and ~$4.6B in proceeds from property and equipment sales and incentives).

The diluted weighted-average shares outstanding in FY2023 is 10.492B and 10.708B in Q2 2024. If AMZN does not repurchase any shares in the remainder of FY2024 and continues to issue shares (stock based compensation), it is quite possible that the diluted weighted-average shares outstanding in FY2024 could be 10.81B.

If AMZN is able to generate ~$52B of FCF in the second half of FY2024, it could report ~$104.6B of FCF in FY2024. Divide ~$104.6B of FCF by 10.81B of shares and we get FCF/share of ~$9.68. The closing share price on August 2 was ~$168 thus giving us an estimated P/FCF of ~17.36. In FY2022 and FY2023, AMZN’s P/FCF was ~14 and ~18.33.

Final Thoughts

I am looking to acquire shares in great companies experiencing temporary headwinds and/or which have fallen out of favor with investors for no justifiable reason. AMZN appears to be such a company.

Money has been rotating out of the Magnificent 7 stocks; AMZN is one of these 7 companies. This has led to a share price decline from the 52-week high of ~$201 reached in early July 2024 to ~$168 on August 2.

Despite the recent ~$33 drop in Amazon’s share price in 1 month, I think there is a reasonable probability for more downside.

I do, however, have concerns regarding an AMZN investment!

Only when the tide goes out do you learn who has been swimming naked. – Warren Buffett

Car repossessions, credit card delinquency, and mortgage refinancing statistics suggest an increasing number of consumers are experiencing financial hardship; the tide appears to be receding.

My sources in the financial sector tell me about an increasing number of homeowners experiencing financial strain. Many tenants have also experienced a shock with rents rising much faster than their income. Some small business owners are telling me that times are more difficult than they have experienced in years.

This makes me wonder how the deteriorating financial state of Amazon’s typical consumer will affect its online marketplace. To what extent were purchases made in recent years ‘nice to have’ purchases versus ‘need to have’ purchases.

We then need to consider AMZN’s capital allocation history and question whether anything will change. How can we make a decent investment return if no cash flow or earnings are being returned to shareholders? This company continues to issue a ‘boatload’ of shares annually under its various stock based compensation programs. How does this help the average investor?

AMZN might be a great company but is it likely to be a decent long-term investment if shares are purchased in this environment?

How the market will behave in the short term is beyond me. Many ‘investors’ who have recently been ‘soaring with the eagles’, however, are going to find themselves in a predicament where the ‘pigeons are doing a number on their head.’

I am not initiating an Amazon position.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I do not have exposure to AMZN.

Disclaimer: I do not know your circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decisions without conducting your research and due diligence. You should also consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.