I last reviewed Zoom Communications (ZM) in this May 27, 2025 post when the most current financial information was for Q1 2026. With the release of Q2 and YTD2026 results following the August 21, 2025 market close, I revisit this existing holding.

Business Overview

Part 1, Item 1 in ZM’s FY2024 Form 10-K (see SEC Filings) provides a comprehensive overview of the business, competition, and risks.

On October 9, 2024, ZM held its Zoomtopia Investor Session. This information provides a good overview of this company’s future potential. The next Zoomtopia is scheduled for September 17 and 18, 2025.

ZM has Class A (publicly traded shares) and Class B shares. The Class A and B shares have 1 and 10 votes per share, respectively.

The Class B shareholders have significant influence over the management and over all matters requiring stockholder approval, including the election of directors and significant corporate transactions, such as a merger or other sale of ZM or its assets, for the foreseeable future. Within the Risk Factors section of ZM’s Form 10-Q and Form 10-K, there is commentary regarding this dual-class structure.

Financials

Q2 and YTD2026 Results

ZM’s Q2 2026 earnings material (including the transcript of management’s commentary on the earnings call) is accessible here.

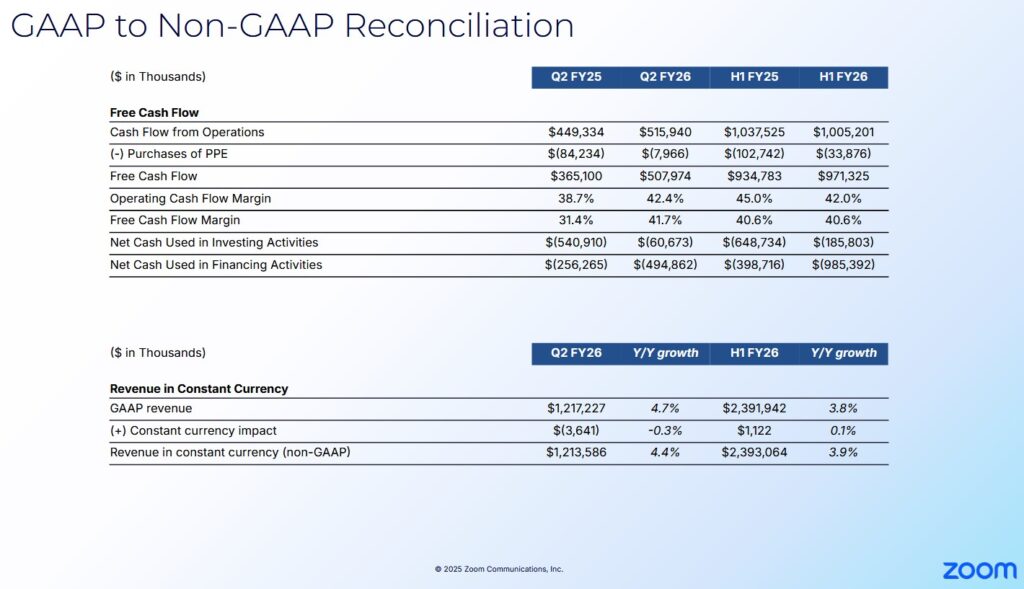

The Q2 2025 and Q2 2026 GAAP to Non-GAAP reconciliation is accessible through the Q2 2026 earnings presentation.

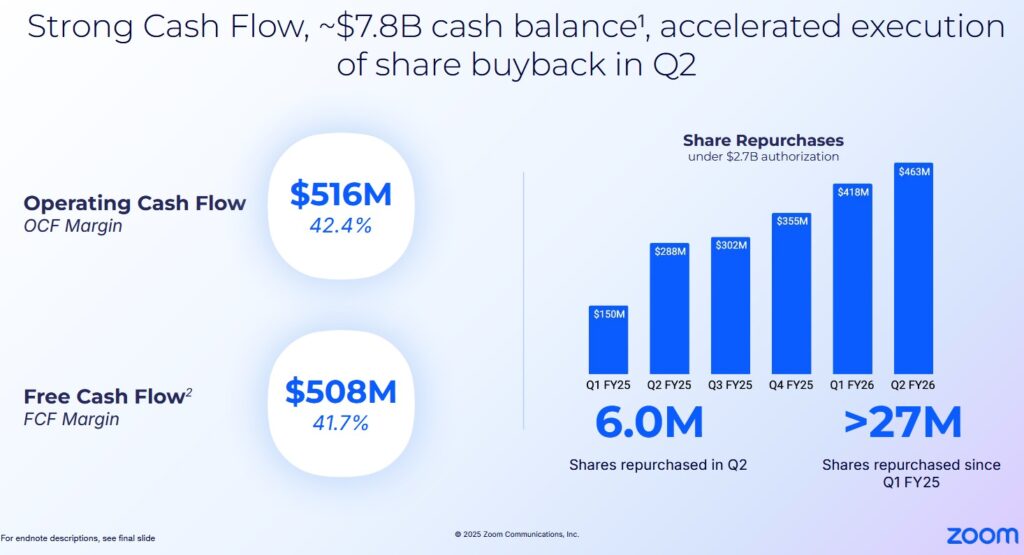

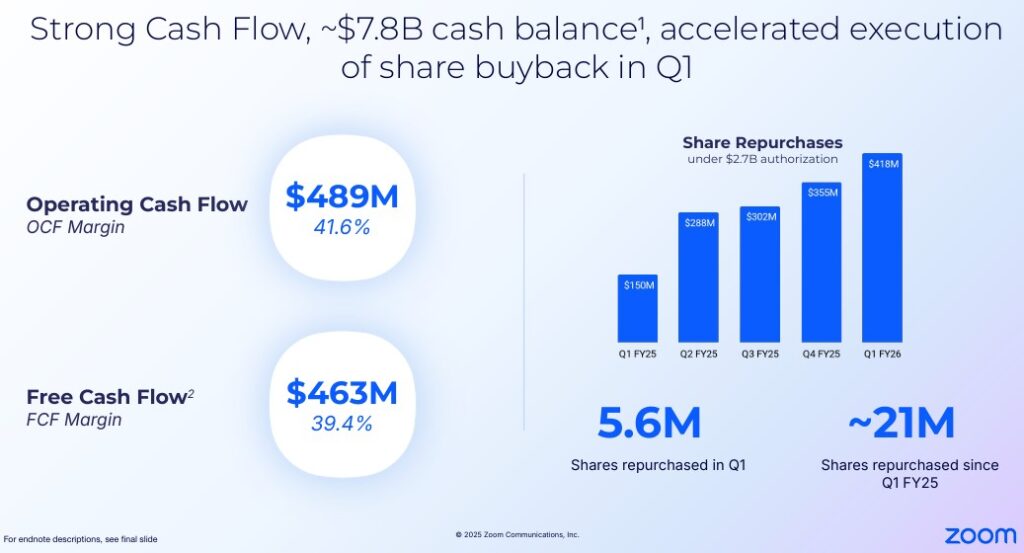

ZM’s cash and cash equivalents and marketable securities at FYE2025 was ~$7.79B, an increase from ~$7B, ~$7.5B, and ~$7.7B at FYE2024, Q2 2025, and Q3 2025. At the end of Q1 2026, this had risen to ~$7.8B and remains at this level at the end of Q2 2026 despite over $0.883B in YTD share repurchases.

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX

In my prior ZM post I touch upon my rationale for deducting stock-based compensation (SBC) to calculate FCF. I, therefore, dispense with explaining this again.

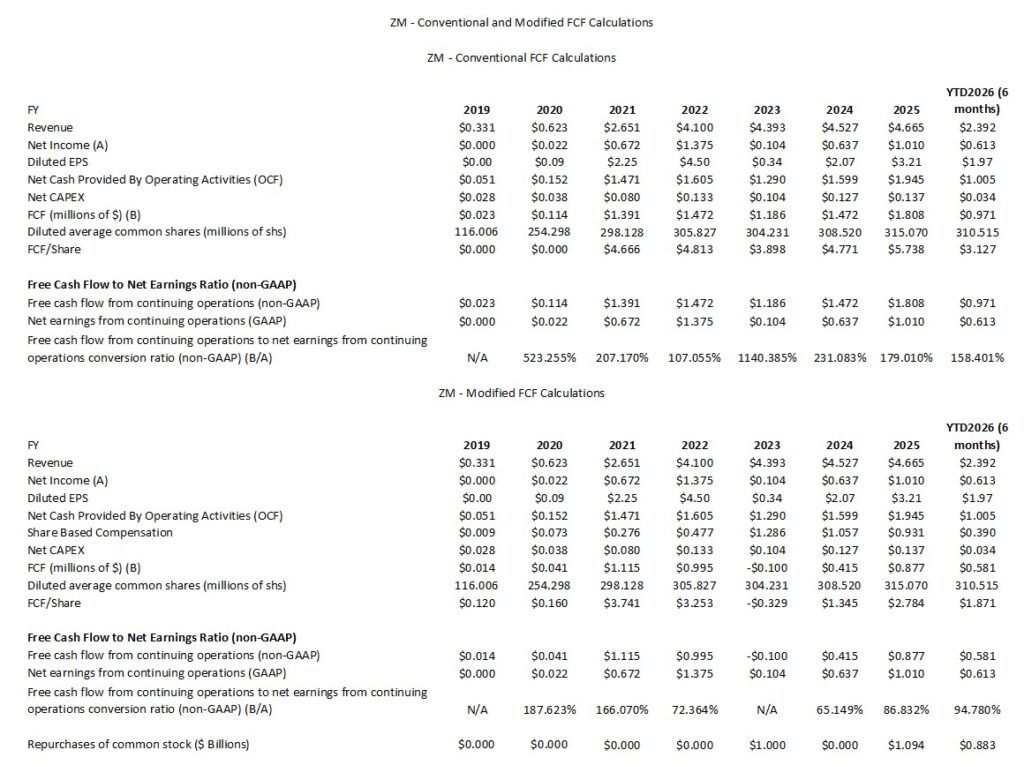

The following compares ZM’s FCF using the ‘conventional’ and ‘modified’ calculation methods.

The following reflects the manner in which ZM calculates FCF for Q2 2025 and Q2 2026.

Capital Allocation

The capital allocation priority is to reinvest in the company; this can include acquisitions. The opportunistic repurchase of Class A shares comes next.

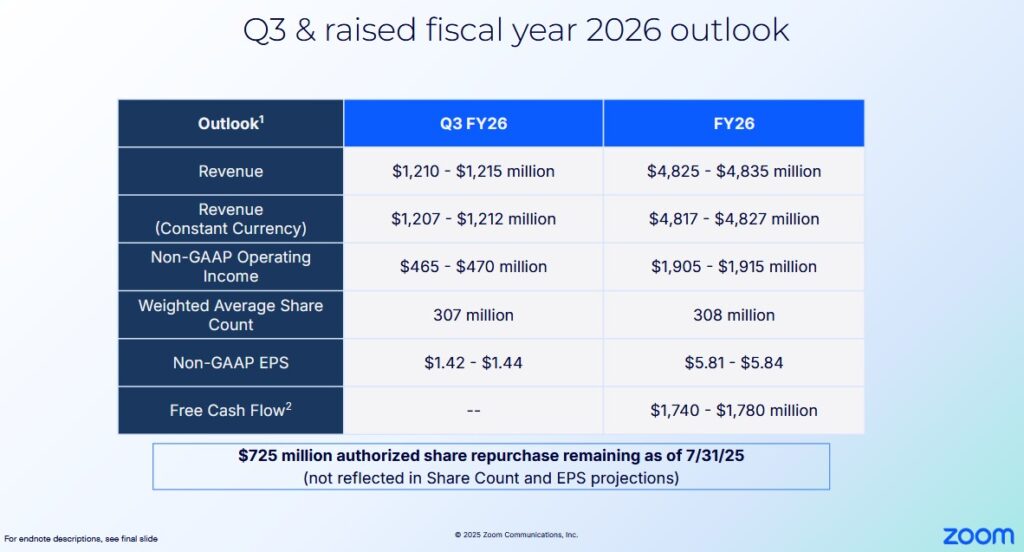

Q3 and FY2026 Outlook

The following reflects ZM’s Q3 and FY2026 outlook.

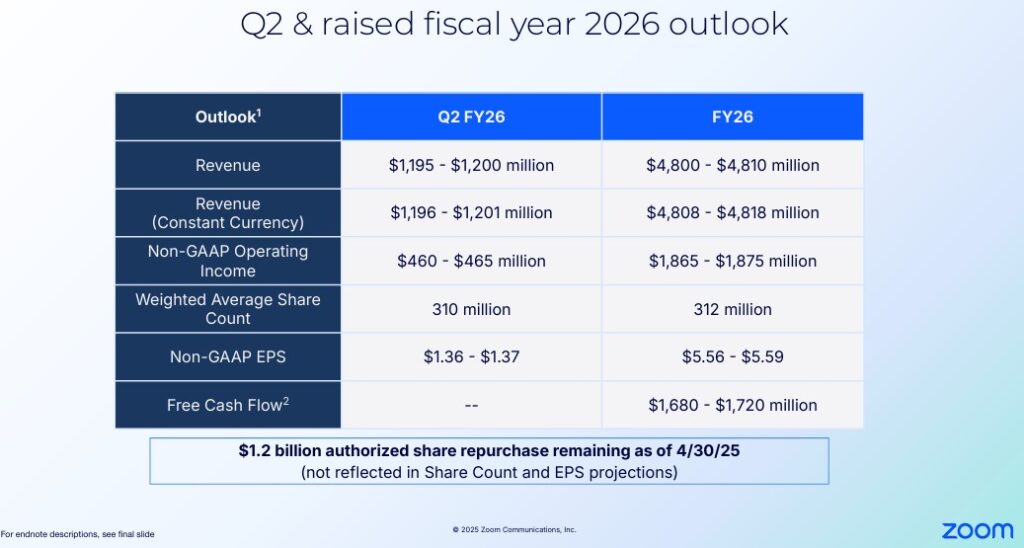

I provide ZM’s prior outlook below for comparison.

Risk Assessment

ZM has no debt to rate.

Dividends and Share Repurchases

Dividend and Dividend Yield

Management specifically states the following in its Form 10-Q and Form 10-K:

We do not intend to pay dividends for the foreseeable future.

We have never declared nor paid cash dividends on our capital stock. We currently intend to retain any future earnings to finance the operation and expansion of our business, and we do not expect to declare or pay any dividends in the foreseeable future. As a result, stockholders must rely on sales of their Class A common stock after price appreciation as the only way to realize any future returns on their investment.

Share Repurchases

One thing I did not like about ZM when I initiated a position on August 22, 2023 was the unsustainable increase in the weighted average outstanding diluted shares (see table above).

Further information about ZM’s Stockholders’ Equity and Equity Incentive Plans is found in each Form 10-Q and Form 10-K.

ZM’s SBC in FY2024 and FY2023, for example, was ~$1.057B and ~$1.286B while share repurchases amounted to $0 and ~$1B. In FY2025, however, SBC amounted to ~$0.931B and the company repurchased ~$1.094B. In the first half of FY2026, SBC was ~$0.39B and ZM repurchased ~$0.883B.

The acceleration in share buyback is evident as more than 27 million shares having been repurchased since Q1 2025.

The diluted weighted-average shares used in computing net income per share attributable to common stockholders is reflected in the table provided in the Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX section of this post. 310.515 million is the weighted average for the first half of the current fiscal year. The weighted average in Q2 2026, however, is 308.224 million and ZM will likely repurchase more shares in the second half of FY2026.

Valuation

Management’s current FY2026 adjusted diluted EPS outlook is $5.81 – $5.84. The August 21, 2025 closing share price was $73.17. Using this share price and the ~$5.825 mid point of management’s outlook, the forward adjusted diluted PE is ~12.56.

Using this current share price and the currently available adjusted diluted EPS broker estimates, ZM’s forward adjusted diluted PE levels are:

- FY2026 – 23 brokers – ~13 using a mean of $5.65 and low/high of $5.55 – $5.88.

- FY2027 – 29 brokers – ~ 12.7 using a mean of $5.78 and low/high of $5.17 – $6.77.

- FY2028 – 14 brokers – ~ 12.2 using a mean of $6.02 and low/high of $4.96 – $7.46.

I place little reliance on broker estimates and almost no reliance on any estimates beyond those for the current fiscal year. This is because much can happen beyond the current fiscal year that can make these estimates irrelevant. Furthermore, the disparity in estimates implies that the brokers which cover ZM have very different outlooks.

Conventional FCF Calculation

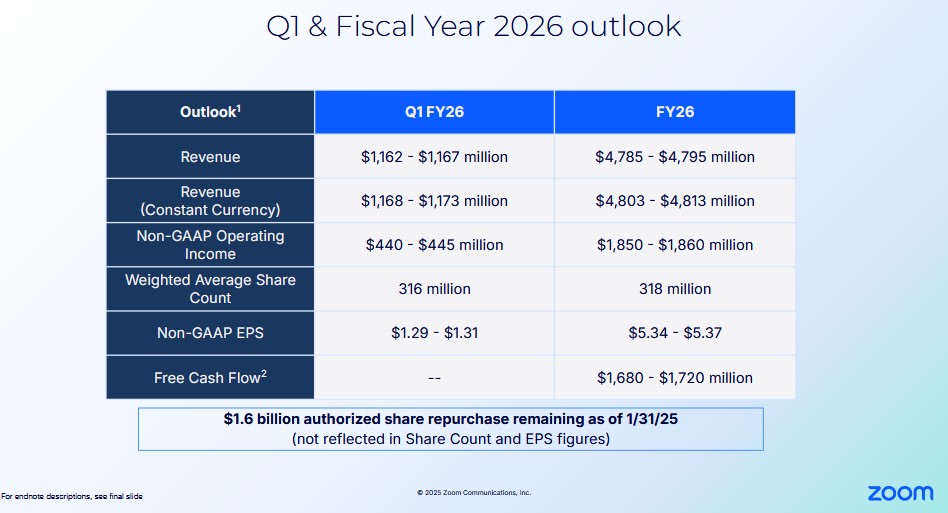

Management’s FY2026 FCF guidance is $1.74B – $1.78B and the diluted weighted average shares outstanding forecast is 308 million (the outlook at the beginning of the year was 318 million). This gives us a FCF/share estimate of ~$5.65 – ~$5.78. Based on a $73.17 share price, the forward P/FCF is ~12.7 – ~13.

ZM, however, still has $0.725B authorized share repurchase remaining at the end of Q2 2026. It is, therefore, entirely possible that the FY2026 diluted weighted average outstanding shares could end up being lower than 308 million!

Modified FCF Calculation

When we deduct YTD2026 SBC of ~$0.39B, we get $0.581B of YTD FCF.

If SBC in the second half of FY2026 is similar to the first half, FY2026 SBC should be ~$0.78B. Deduct this from management’s FY2026 FCF guidance of $1.74B – $1.78B and we get a modified FCF range of ~$0.96B – ~$1B. Divide this by 308 million shares and we get a FCF/share range of ~$2.53 – ~$3.25. Using the a $73.17 share price, we get a P/FCF range of ~22.51 – ~29.

These valuations are more favorable than at the time of my February 25, 2025 and May 27, 2025 posts.

Final Thoughts

ZM has been a terrible investment for investors who disregarded the underlying fundamentals of the business and grossly overpaid to acquire shares between February 2020 – July 2022. Furthermore, the share price has been relatively stagnant since early 2023.

ZM ‘s top line growth is considerably lower than the FY2019 – FY2021 period. If we delve into ZM’s financial results over the past several years, however, we see that the company’s financial position is considerably stronger than a few years ago.

Even if revenue grows at ‘only’ a mid-single digit annually, the company’s cost structure is such that it should generate considerable OCF and FCF (even if it spends close to $1B annually in R&D).

An area of concern when I invested in ZM was its SBC. Fortunately, the company is scaling this back. It peaked at ~$1.286B in FY2023. In the first 6 months of FY2026 it is ~$0.39B.

In conjunction with scaling back SBC, ZM is now aggressively repurchasing shares. Despite $1.976B of share repurchases in Q1 2025 – Q2 2026, ZM continues to have no debt and it has ~$7.8B of cash and cash equivalents and marketable securities.

Given the acceleration of share repurchases, I hope ZM remains undervalued.

I am satisfied with my existing exposure of 1000 ZM shares at an average cost of ~$64.38 in a ‘Core’ account within the FFJ Portfolio. While I currently have no plans to increase my exposure, this is subject to change.

I continue to consider ZM’s fair value to be in the low $90s in the event ZM piques your interest.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long ZM.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.