My last Accenture (ACN) review is in this September 26, 2025 post following the release of FY2025 results. In that post I disclose my September 25 purchase of 100 shares @ ~$236.25.

With the release of Q1 2026 results and updated FY2026 guidance on December 18, I revisit this existing holding.

Business Overview

ACN is a leading global professional services company that helps the world’s leading organizations build their digital core, optimize their operations, accelerate revenue growth and enhance services. It works across every major market with more than 9,000 clients, including the world’s largest companies and 75% of the Fortune Global 100 and 500.

ACN is arguably the world’s leading professional services company with 783,691 employees at November 30 serving clients in more than 120 countries.

ACN’s deep relationship with the world’s largest enterprises and a robust partnership ecosystem sets it apart from many industry participants. It does, however, face a challenge in retooling its sizable workforce for artificial intelligence-based transformation projects. Its deep understanding of enterprise IT should, however, expand its footprint as AI adoption increases.

Given the current business environment, some industry participants will likely cease to exist over the next few years. New industry participants, however, are being created as employees from existing industry participants decide to enter the fray and create their own firms. Many existing and new professional services companies, however, do not have the resources to compete directly with ACN.

The demand for consulting services typically diminishes when economic and business conditions become difficult. During challenging times, clients/prospects look to scale back expenses. Consulting services are often ‘high on the chopping block’. Despite being an industry leader, ACN is susceptible to clients/prospects scaling back their ‘consulting spend’.

Having said this, management states the following on the Q1 2026 earnings call:

Clients continue to prioritize their most strategic and large-scale transformational programs, which convert to revenue more slowly but position us at the center of their reinvention agendas. The pace of overall spending and discretionary spend in our market is at the same levels we have seen over the last year. We are delivering strong results and taking market share in this environment because reinvention is critical to our clients, and our clients know we deliver real reinvention with real outcomes.

The best way to learn about ACN is to:

- review the company’s website; and

- read the FY2025 Form 10-K that is accessible through the SEC Filings section of the company’s website.

Financial Results

Q1 2026 Results

Form 8-K and Form 10-Q found within SEC Filings section of ACN’s website reflect Q1 2026 results.

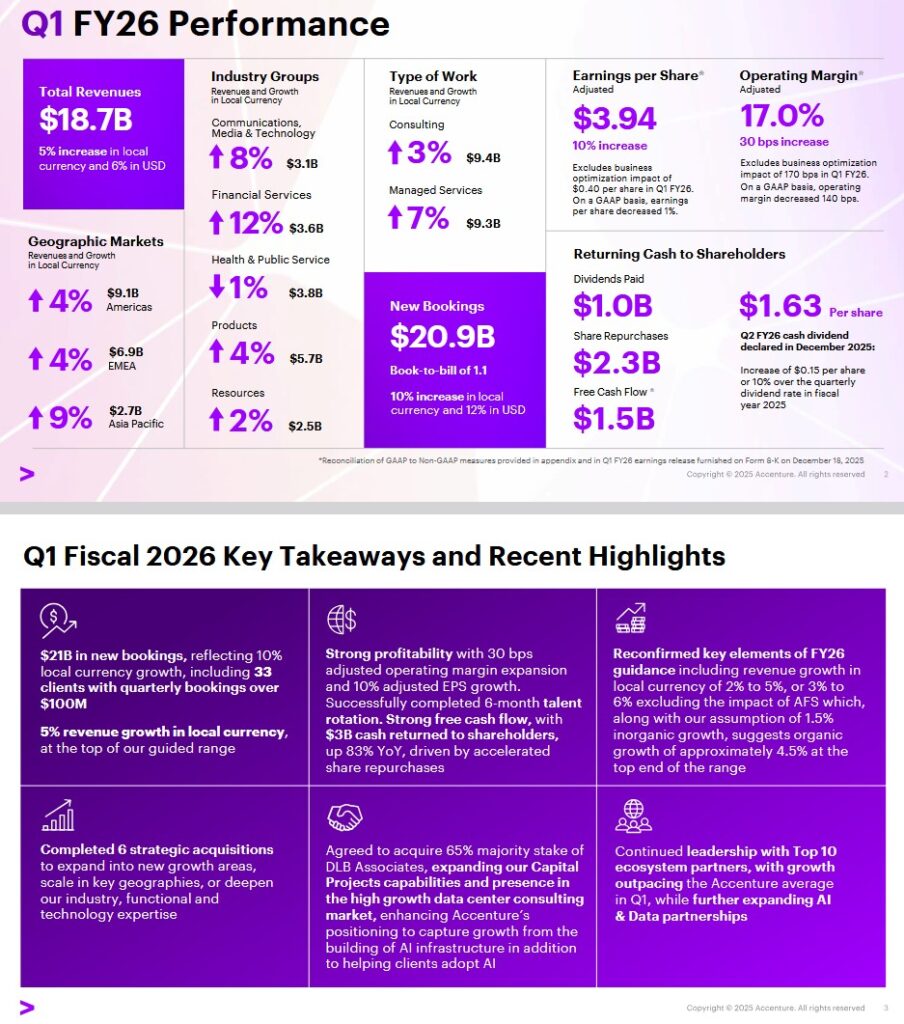

The following is from the Q1 2026 earnings presentation.

On the Q1 2026 earnings call, management states:

ACN had bookings of $20.9B, including 33 clients with quarterly bookings greater than $100 million. We delivered revenue of $18.7B, growing 5% in local currency at the top of our guided range, with broad-based growth across markets and both types of work. And we continue to strengthen our competitive position by taking significant market share on a rolling four-quarter basis against our basket of our closest global publicly traded competitors, which is how we calculate market share.

The demand for AI is both real and rapidly maturing. We’ve now reached a point where advanced AI is being embedded in some way across nearly everything we do, and many of our clients are focusing on moving beyond standalone proofs of concept or initiatives. We’re shifting to more scaled end-to-end solutions that integrate multiple forms of AI.

Growth was led by banking and capital markets, industrials, and software and platforms, partially offset by a decline in public service. Revenue growth was driven by the United States. In EMEA, we delivered 4% growth in local currency, led by growth in banking and capital markets, insurance, and life sciences. Revenue growth was driven by the United Kingdom and Italy. In Asia-Pacific, revenue grew 9% in local currency, led by growth in banking and capital markets, communications and media, and public service. Revenue growth was led by Japan and Australia.

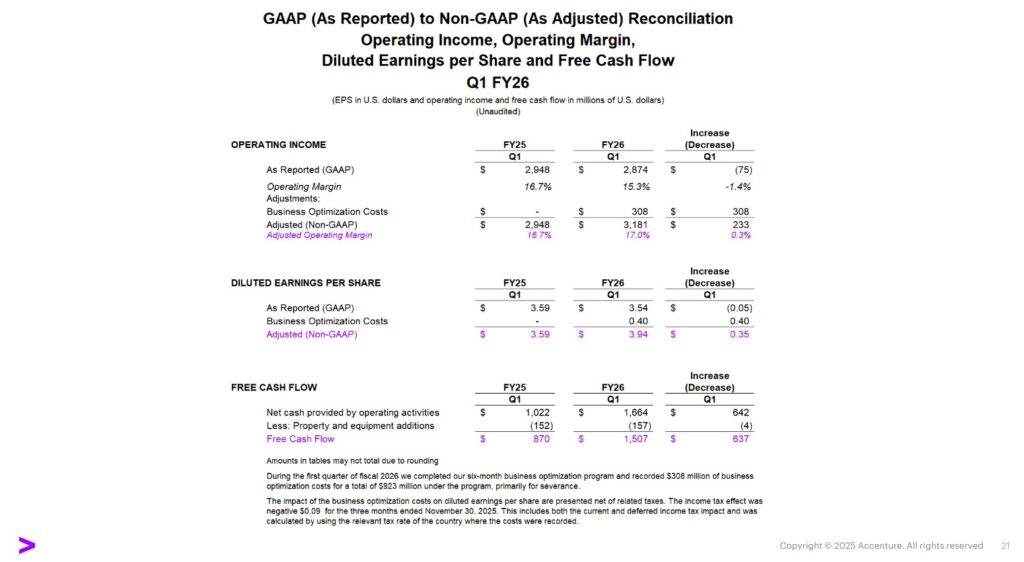

I want to briefly update you on the business optimization actions we initiated last quarter and completed in Q1 as part of executing our talent strategy. This quarter, we recorded $308 million in costs, primarily related to employee severance, bringing the total for these actions over the past six months to $923 million.

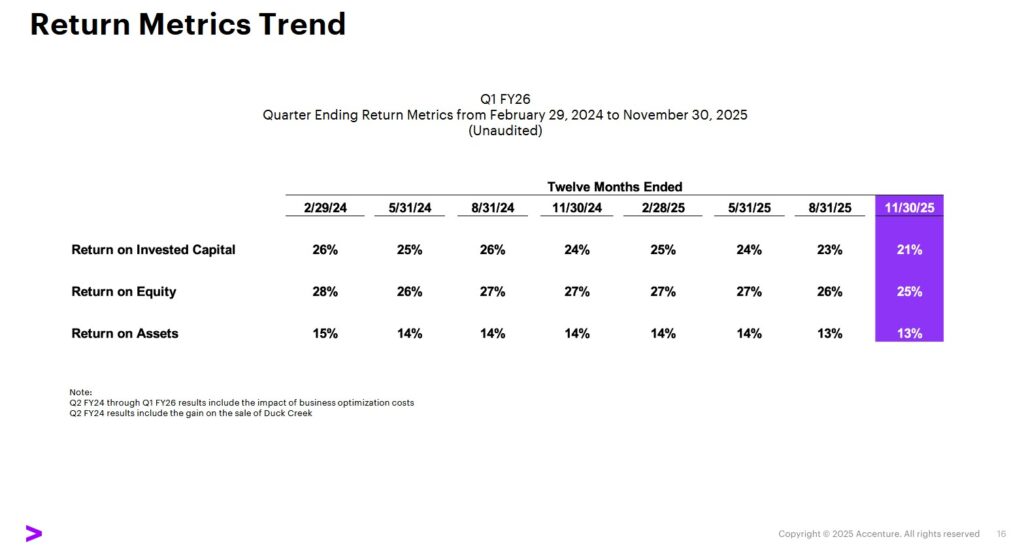

Although the trend in ACN’s return metrics is uninspiring, I am not alarmed. It still generates an attractive ROIC, ROE, and ROA; the most recent return metrics are found below and are accessible in supporting materials. I have the utmost confidence senior management is closely monitoring these return metrics.

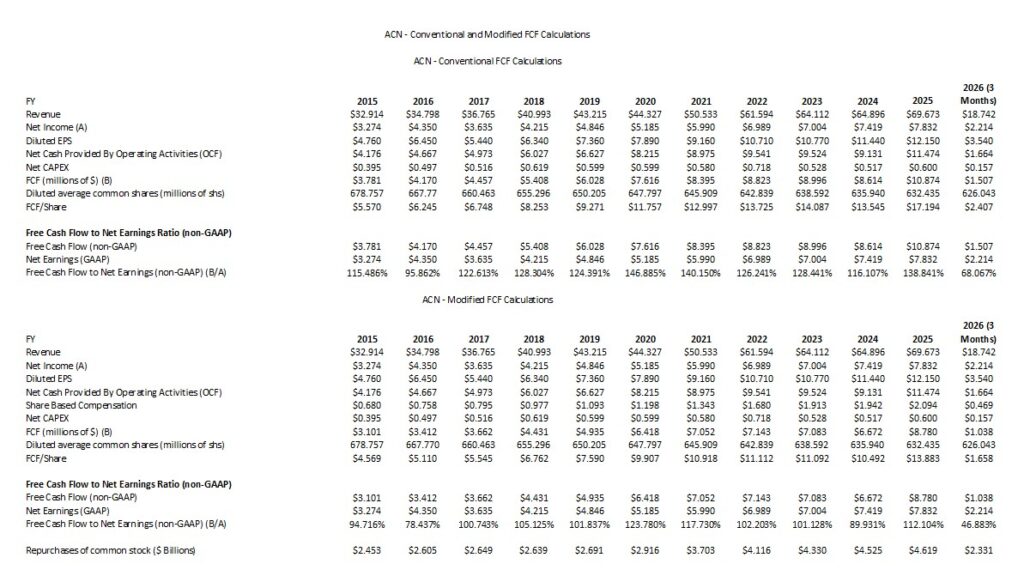

Conventional And Modified Free Cash Flow (FCF) Calculations (FY2015 – FY2025 and Q1 2026)

In my September 28, 2024 How Stock Based Compensation Distorts Free Cash Flow post, I touch upon how a company’s FCF can be distorted. In several subsequent posts, I take a conservative approach when looking at a company’s FCF.

FCF is a non-GAAP measure, and therefore, the manner in which it is computed is open to debate. Most companies subtract capital expenditures (CAPEX) from Net Cash Provided by Operating Activities found in the Consolidated Statement of Cash Flows. They do not, however, deduct share-based compensation (SBC). Given the magnitude of ACN’s SBC, I think it is prudent to deduct it.

We see that the magnitude of ACN’s SBC has a material impact on the company’s FCF. The following reflects how ACN calculates FCF.

The following reflects how ACN calculates FCF.

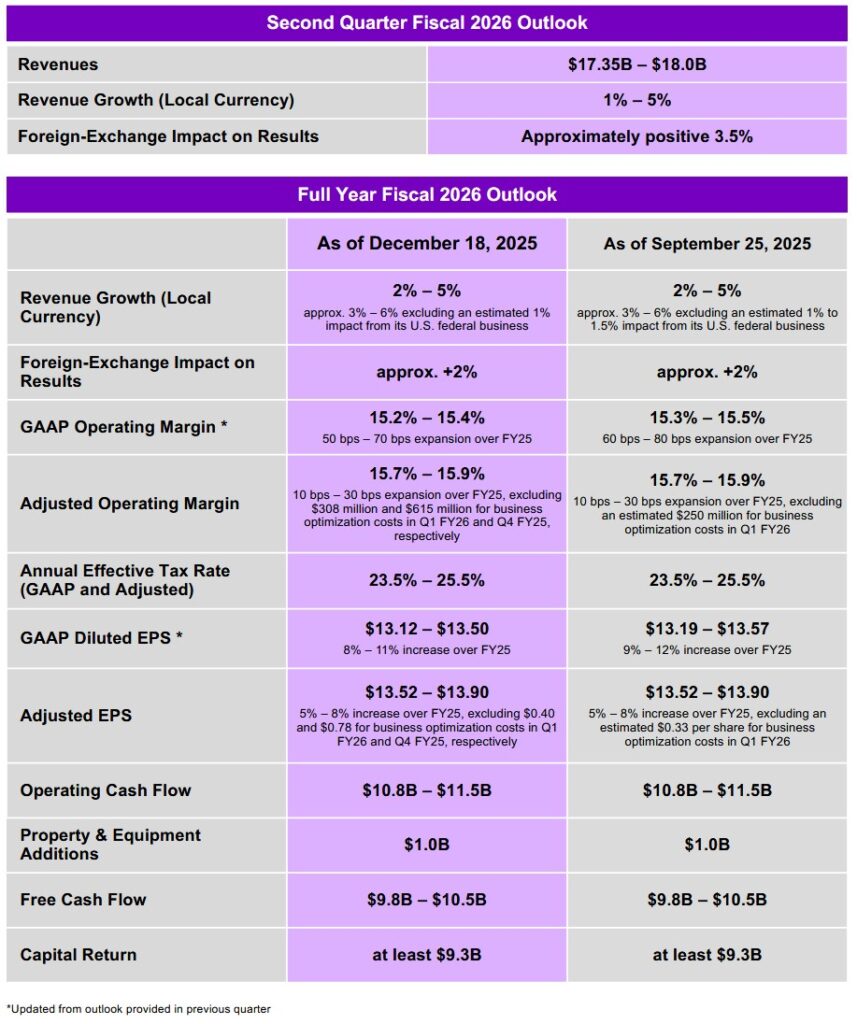

FY2026 Outlook

The following reflects ACN’s prior and current FY2026 outlook.

Risk Assessment

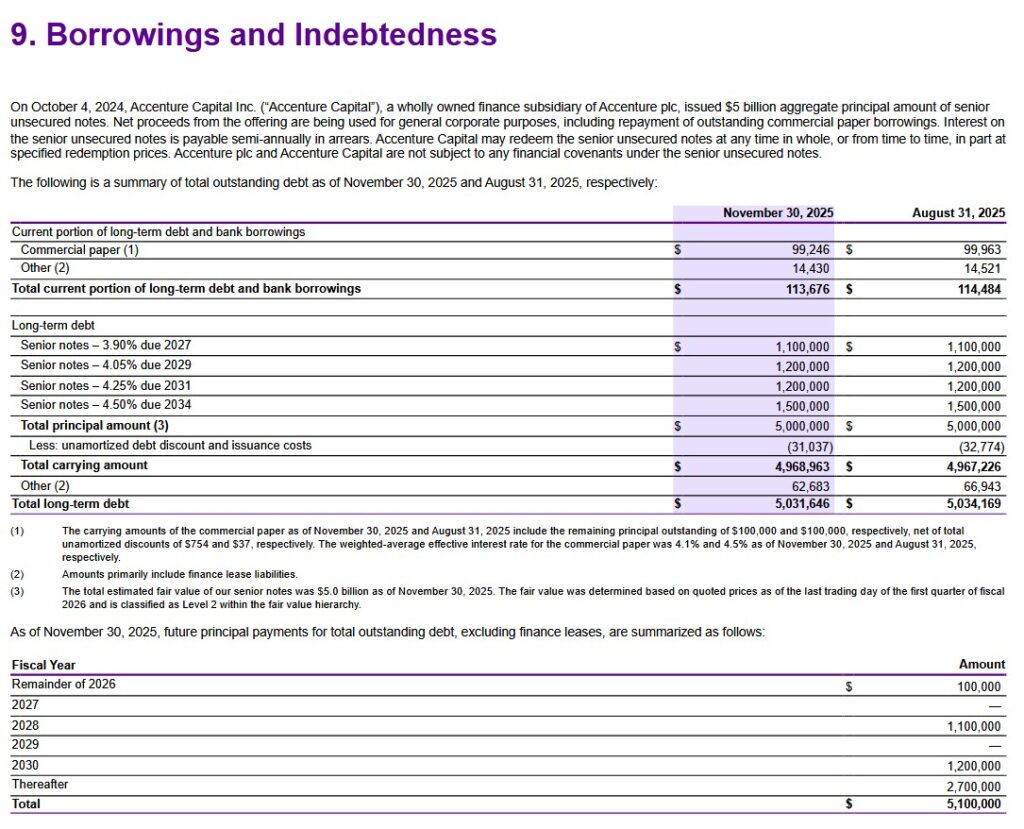

The risk aspect of an investment is important. This is why I am particularly interested in the maturity schedule of a company’s long-term debt as well as the interest rates (amongst other things).

At the end of Q1 2026, ACN’s current portion of long-term debt was $113.676 million and the long-term portion was ~$5.032B. These values are relatively similar to what ACN reported at the end of FY2025 (see below).

For years, ACN operated with more cash than debt. In FY2025, it issued debt across four tranches to shift from relying solely on cash-on-hand. The reasoning for issuing this debt was to:

- fund ACN’s aggressive acquisition strategy. In FY2025, ACN invested $1.5B in strategic acquisitions. The plan is to deploy ~$3B to acquire smaller AI boutiques before the Big Four (Deloitte, PwC, EY, and KPMG) or IBM can acquire them.

- offset the impact of significant restructuring charges in FY2025.

This issuance, executed through its subsidiary Accenture Capital Inc. in October 2024 (the start of FY2025), was driven by the following strategic financial objectives.

- build a ‘digital core’ for clients, specifically in Generative AI, Cloud, and Data services;

- provide liquidity to acquire boutique firms and specialized technology providers globally without depleting operational cash.

ACN generates strong FCF which it can return to shareholders in the form of dividends and share repurchases. The firm’s intention is to return more of its FCF to shareholders. By using low-cost debt, it can maintain these high returns while investing heavily in internal growth and R&D.

Unless ACN’s ability to generate strong cash flow takes a dramatic turn for the worse, meeting the staggered long-debt debt maturities should pose no issue.

ACN’s Aa3 long term issuer rating was affirmed by Moody’s on October 1, 2024 with a stable outlook. This is the bottom tier of the high grade investment grade category.

S&P last reviewed ACN on April 24, 2025 at which time it affirmed its AA- rating with a stable outlook. This is the bottom tier of the high grade investment grade category.

Moody’s and S&P Global define ACN as having a very strong capacity to meet its financial commitments. It differs from the highest-rated obligors only to a small degree.

Dividends

ACN distributes a quarterly dividend (see history).

On November 14, 2025, a quarterly cash dividend of $1.63 per share was paid to shareholders of record at the close of business on October 10, 2025. These cash dividend payments totaled $1B.

ACN has just declared another quarterly cash dividend of $1.63/share for shareholders of record at the close of business on January 13, 2026. This dividend, payable on February 13, 2026, represents a 10% increase over the $1.48 quarterly dividend a year ago.

Dividend metrics are of very little relevance in my investment decision making process. If they are important to you, you may wish to check with your broker about the the dividend withholding tax rate and whether the ACN dividends are eligible for automatic dividend reinvestment.

Share Repurchases

On September 22, 2025, ACN’s Board approved $5B in additional share repurchase authority bringing the total outstanding authority to $7.851B.

Looking at the table reflected in the Conventional And Modified Free Cash Flow (FCF) Calculations (FY2015 – FY2025) section of this post, we see that the diluted weighted average shares outstanding in FY2015 was 678.757 million (versus 629.4 million in Q4 2025 and 626.043 million in Q1 2026).

During Q1 2026, ACN repurchased/redeemed 9.5 million shares for a total ~$2.23B at an average price of $245.32 per share, including 9.1 million shares repurchased in the open market.

The total remaining share repurchase authority at November 30, 2025 was ~$5.6B.

The FY2026 outlook calls for a return of at least $9.3B. If it returns ~$4.2B to shareholders in the form of dividends, it is likely that ~$5.1B will be returned in the form of share repurchases. ACN’s share price remaining under pressure bodes well for share repurchases!

Valuation

ACN’s diluted EPS and adjusted diluted EPS guidance for FY2026 is $13.19 – $13.57 ($13.38 mid-point) and $13.52 – $13.90 ($13.71 mid-point), respectively. Using the mid-points and current ~$270 share price, the forward diluted PE is ~20.2 and the adjusted diluted PE is ~19.7.

Using the current broker adjusted diluted EPS estimates, ACN’s forward-adjusted diluted PE levels are:

- FY2026 – 25 brokers – ~19.5 based on a mean of $13.82 and low/high of $13.30 – $14.16.

- FY2027 – 25 brokers – ~18.2 based on a mean of $14.87 and low/high of $14.31 – $15.24.

- FY2028 – 16 brokers – ~16.8 based on a mean of $16.09 and low/high of $15.24- $16.82.

Given that ACN has just released its results and guidance, we can expect these estimates to change over the coming days.

Although I try to gauge a company’s valuation on estimated future earnings, my preference is to gauge a company’s valuation based on estimated FCF.

The company’s FCF/EPS ratio is generally well in excess of 100% when calculated using the conventional method and roughly 100% when calculated using the modified method. This is because ACN’s annual SBC is sizable.

ACN’s FY2026 FCF outlook remains at ~$9.8B – ~$10.5B (conventional method calculation). In FY2023, FY2024 and FY2025, the diluted weighted average shares outstanding was 638.592 million, 635.94 million, and 632.435 million (629.418 million in Q4 2025 and 626.043 million in Q1 2026).

The company continues to target $9.3B through dividends and share repurchases in FY2026. In Q1, it distributed $1.01B in dividends. The company is repurchasing shares but also issues shares to its employees. We also need to consider that after the next 3 quarterly $1.63/share dividend distributions, ACN will likely increase its quarterly dividend (perhaps another 10% bringing the dividend to ~$1.79). I, therefore, estimate that the total dividend distribution in FY2026 could be ~$4.2B. If this materializes, ACN may repurchase ~$5.1B of its shares in FY2026.

This is certainly not an exact science. It, however, seems reasonable that the FY2026 diluted weighted average shares outstanding could be ~626.71 ((629.418 + 624 by FYE2026)/2).

Taking the ~$10.15B mid point of management’s FY2026 FCF outlook and ~626.71 million shares, we get ~$16.20 in FCF/share. Divide ~$270 by ~$16.20 and the P/FCF is ~16.7.

My preference is to calculate P/FCF using the ‘modified FCF’ method which takes into consideration SBC.

ACN’s FY2025 and FY2024 SBC was ~$2.094B and ~$1.942B. If it increases to $2.25B in FY2026 and we deduct this from the ~$10.15B mid point of management’s FY2026 FCF outlook, we get a FY2026 FCF outlook of ~$7.9B. Divide this by ~626.71 million shares and we get ~$12.61 in FCF/share. Divide ~$270 by ~$12.61 and the P/FCF is ~21.4.

I reflect the following in my September 26, 2025 post.

ACN reported FY2025 diluted EPS of $12.15 – well below the $12.77 – $12.89 forecast. On the bright side, however, ACN’s FY2025 FCF of ~$10.874B is favorable relative to management’s ~$9B – ~$9.7B outlook (conventional method calculation).

When I initially tried to estimate ACN’s valuation, I used ~632 million as my FY2025 weighted average diluted shares outstanding. The actual figure was just over 632.4 million.

My prior valuation estimates are ‘blown out of the water’ given the significant disparity between management’s prior outlook and the actual results.

Management’s FY2026 adjusted diluted EPS outlook is $13.52 – $13.90. Using my ~$236.25 September 25 purchase price, the forward adjusted diluted PE range is ~17 – ~17.5.

Using the current broker adjusted diluted EPS estimates, ACN’s forward-adjusted diluted PE levels are:

- FY2026 – 24 brokers – ~17.2 based on a mean of $13.76 and low/high of $13.48 – $13.94.

- FY2027 – 22 brokers – ~15.9 based on a mean of $14.88 and low/high of $13.98 – $15.69.

- FY2028 – 11 brokers – ~14.7 based on a mean of $16.07 and low/high of $14.84- $16.67.

Revisions to these estimates are currently in progress and are likely to continue over the coming days.

The company’s FCF/EPS ratio is generally well in excess of 100% when calculated using the conventional method and roughly 100% when calculated using the modified method. This is because ACN’s annual SBC is sizable.

ACN’s FY2026 FCF outlook is ~$9.8B – ~$10.5B (conventional method calculation). In FY2023, FY2024 and FY2025, the diluted weighted average shares outstanding was 638.592 million, 635.94 million, and 632.435 million (629.418 million in Q4 2025).

As noted in the Share Repurchases section of this post, I anticipate ACN will repurchase ~$5.1B of its shares in FY2026. It will, however, issue shares to its employees. If it can repurchase shares at attractive valuations, we could see the Q4 2026 weighted average shares outstanding being close to 624 million thus giving us a FY2026 average of ~626.71 ((629.418 + 624)/2).

Taking the ~$10.15B mid point of management’s FY2026 FCF outlook and ~626.71 million shares, we get ~$16.20 in FCF/share. Divide ~$236.25 by ~$16.20 and the P/FCF is ~14.6.

My preference is to calculate P/FCF using the ‘modified FCF’ method which takes into consideration SBC.

ACN’s FY2025 and FY2024 SBC was ~$2.094B and ~$1.942B. If it increases to $2.25B in FY2026 and we deduct this from the ~$10.15B mid point of management’s FY2026 FCF outlook, we get a FY2026 FCF outlook of ~$7.9B. Divide this by ~626.71 million shares and we get ~$12.61 in FCF/share. Divide ~$236.25 by ~$12.61 and the P/FCF is ~18.8.

I reflect the following in my July 29, 2025 post at which time I initiated my ACN position.

In the first 9 months of FY2025, ACN generated $9.90 of diluted EPS and the current FY2025 diluted EPS outlook is $12.77 – $12.89. Using my recent ~$284.58 purchase price, the forward diluted PE range is ~22.1 – ~22.3.

Using the current broker adjusted diluted EPS estimates, ACN’s forward-adjusted diluted PE levels are:

- FY2025 – 19 brokers – ~22.1 based on a mean of $12.88 and low/high of $12.81 – $13.02.

- FY2026 – 20 brokers – ~20.6 based on a mean of $13.80 and low/high of $13.48 – $14.16.

- FY2027 – 13 brokers – ~19 based on a mean of $14.97 and low/high of $14.37- $15.55.

Although I look at brokers’ earnings estimates, all estimates beyond the current fiscal year have no bearing on my investment decision making process. My reasoning is that I have no confidence that anybody can consistently and accurately determine a company’s performance as we go further out on the calendar. The variance in the brokers’ earnings estimates clearly indicates there is no consensus on ACN’s future performance.

EPS can also be distorted by various means. My preference, therefore, is to gauge a company’s valuation using FCF.

ACN’s FY2025 FCF outlook is ~$9B – ~$9.7B (calculated under the conventional method). In FY2023, FY2024 and Q3 2025, the diluted weighted average shares outstanding was 638.592 million, 635.94 million, and 630.457 million. ACN plans to acquire additional shares in Q4 so if the FY2025 weighted average is reduced to ~632 million, we can expect ACN’s FY2025 FCF/share to be ~$14.24 – ~$15.35. Using my recent ~$284.58 purchase price, the P/FCF is ~18.5 – ~20.

As noted earlier, however, my preference is to calculate P/FCF using the ‘modified FCF’ method which takes into consideration SBC.

ACN’s YTD2025 SBC is ~$1.654B or ~$0.551B/quarter. If ACN’s FY2025 SBC amounts to $2.205B (~$1.654B + ~$0.551B) and we deduct this from management’s ~$9B – ~$9.7B FY2025 FCF outlook, the FY2025 FCF is ~$6.795B – ~$7.495B. We arrive at FCF ~$10.75 – ~$11.86 when we divide this range by ~632 million shares. Using my recent ~$284.58 purchase price, the P/FCF is ~24 – ~26.5.

Final Thoughts

My current exposure is 800 shares in a ‘Core’ account in the FFJ Portfolio at a ~$267.8545 average cost.

My final thoughts are the same as in my prior post. I continue to welcome opportunities when great companies temporarily fall out of favor and hope ACN’s share price weakens.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long ACN.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation. I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.