![]()

When I retired at 56 in 2016 I was adamant that I would never return to the workforce. My plan was to focus on investing to continually increase our net worth.

So far, things have gone according to plan. I do not, however, know what the future holds which is why Walmart (WMT) has been a core holding for several years.

There are several other companies with the potential to generate long-term total investment returns that are superior to WMT. Investing in WMT, however, gives me peace of mind that this portion of our investment portfolio faces little risk of being suddenly completely wiped out.

In essence, assessing WMT’s risk is relatively straightforward meaning I can focus on analyzing its valuation.

In early 2025, my wife and I withdrew funds from our Registered Retirement Savings Plans (RRSPs). Our tax accountants, however, strongly encouraged us to make a further withdrawal in October 2025 as part of our RRSP meltdown strategy. After analyzing the holdings within our RRSPs, we sold a portion of our WMT holdings because we considered shares to be richly valued. I disclose the sale in this WMT post.

For the benefit of non-Canadians, a RRSP is a Canadian tax advantaged investment account designed to help individuals save for retirement with significant tax advantages. Contributions to a RRSP are tax-deductible, thus reducing taxable income for the year. The investments within the account grow tax-deferred until withdrawal.

While I sold WMT shares, the plan is to opportunistically replace the sold shares.

This is an opportune time to revisit this existing holding given the November 20 release of Q3 and YTD2026 results.

Business Overview

Read Part 1 Items 1 and 1A in the FY2025 Form 10-K that is accessible through the SEC Filing section of the company’s website.

The store units and square footage metrics provide an indication of just how massive WMT is. Despite the extent of its global presence, WMT has ample opportunity to expand its operations!

WMT To Switch Listing From NYSE To NASDAQ

WMT recently announced that it is switching its stock listing from the New York Stock Exchange (NYSE) to the Nasdaq Stock Market (NDAQ) effective December 9, 2025. This change marks the largest exchange transfer in history by market capitalization.

The main reason for this move is WMT’s strategic transformation into a technology-forward, people-led, and tech-powered company. By switching to NDAQ which is known for its strong emphasis on technology and innovation, WMT aims to align its public market presence with its evolving identity, which increasingly revolves around automation, artificial intelligence, and advanced omnichannel retail strategies.

According to senior management, the move signals to investors and the market that WMT is setting new standards for integrating AI and technology in retail, making the company more attractive to growth and tech-focused investors.

I view this switch as a non-issue. A company being added to the NASDAQ100 or the S&P500 often results in greater investor interest and typically has a positive bearing on a company’s stock price. Just switching from one exchange to the other, however, probably won’t have much of an impact on WMT’s share price over the long-term. Investors wanting exposure to WMT likely don’t really care on which exchange shares are listed. As for exchange traded funds (ETFs), a NASDAQ specific ETF might now add WMT but a S&P specific ETF may drop WMT.

I have exposure to NDAQ and Intercontinental Exchange (ICE), which owns the NYSE, so this switch is irrelevant from my perspective.

Financials

Q3 and YTD2026 Results

WMT’s Q3 2026 material is accessible here.

Many retailers are struggling due to rising operational costs, inflation, changing consumer behavior, and the pressure of online competition. Notable retailers facing difficulties include Target, Party City, Walgreens, Macy’s, CVS Health, Kohl’s, and Big Lots. Even Home Depot (which I recently covered in this post) and Lowe’s are experiencing challenges as consumers concerned about their ‘next paycheque’ dial back spending.

WMT has a meaningful presence in Canada where rising bankruptcies linked to high consumer debt, rising costs, and e-commerce growth is challenging traditional stores. A number of Canadian retailers have gone out of business or have ‘one foot in the grave’. The causes include unsustainable debt, competition from large US players like Costco and WMT, the rise of e-commerce, and fixed costs like expensive leases. Examples include:

- Hudson’s Bay Company, one of Canada’s oldest retailers, filed for creditor protection, driven largely by ~$1B in debt and slowing consumer spending.

- Toys “R” Us announced the closure of at least 38 stores across Canada in 2025, shrinking its footprint significantly and with more stores up for sale.

- Understance, a Canadian lingerie brand, announced plans to close all its physical stores in Vancouver, Calgary, and Toronto by December 2025, ending its brick-and-mortar retail experiment.

- Other retailers facing insolvency or restructuring include apparel brands like Frank and Oak, Hakim Optical (eyewear), Ricki’s, Cleo, Comark Holdings, and Oak + Fort.

In total, retail insolvencies surged by about 73% YoY as of early 2025, with elevated bankruptcy and proposal filings for retailers.

Retailers, in general, are passing on their higher costs to consumers. WMT, however, is finding ways to control price increases. This is attracting new middle and upper class customers who would have never, for whatever reasons, considered shopping at WMT.

On the Q3 earnings call, management states:

As we look at our customers and members here in the U.S., they’re still spending with upper and middle income households driving our growth.

We continue to benefit from higher income families choosing to shop with us more often. Middle income households have been steady, and while lower income families have been under additional pressure of late, were encouraged by how our teams are meeting them with greater value across necessities and doing what we can to help them stretch their dollars further.

For the quarter, like-for-like inflation in Walmart U.S. was 1.3% with food and general merchandise up low single digits.

We continue working to resist the upward pressure on our cost of goods and to manage our mix.

We have about 7,400 active rollbacks in Walmart U.S. right now, with more than half of those in the grocery category. Often, our 90-day rollbacks lead to a permanent price reduction, a new EDLP. Since the beginning of the year, more than 2,000 rollbacks have become the new everyday price. We’ll keep strengthening our ability to save people time and money, and we’ll keep spending ways to keep our prices as low as possible and being strategic in our pricing actions. Everyone wants value.

Inventory management is always important, and it’s especially important in this environment as we reduce markdown risk to help fund stronger price gaps.

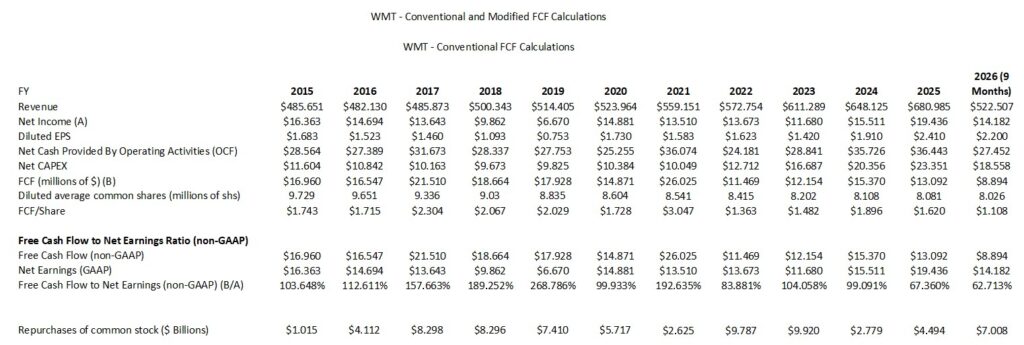

Conventional Free Cash Flow (FCF) Calculations (FY2020 – FY2025 and YTD2026)

FCF is a non-GAAP measure, and therefore, its method of calculation is open to debate. Most companies subtract capital expenditures (CAPEX) from Net Cash Provided by Operating Activities found in the Consolidated Statement of Cash Flows.

I generally analyze a company’s FCF from ‘conventional’ and ‘modified’ perspectives. The ‘conventional’ calculations do not deduct share-based compensation (SBC) while the ‘modified’ calculations deduct SBC. In several posts, I touch upon why I deduct SBC when analyzing a company’s FCF.

I am unable to determine WMT’s SBC (no reference is made in the Consolidated Statement of Cash Flows). I, therefore, I merely analyze WMT’s FCF from a conventional perspective.

The diluted EPS, diluted average common shares, and FCF/share account for the 3-for-1 February 26, 2024 stock split.

The Net CAPEX deducts ‘Proceeds from disposal of property and equipment’ from ‘Payments for property and equipment’.

The YTD2026 results are only for the first 3 quarters of the current fiscal year.

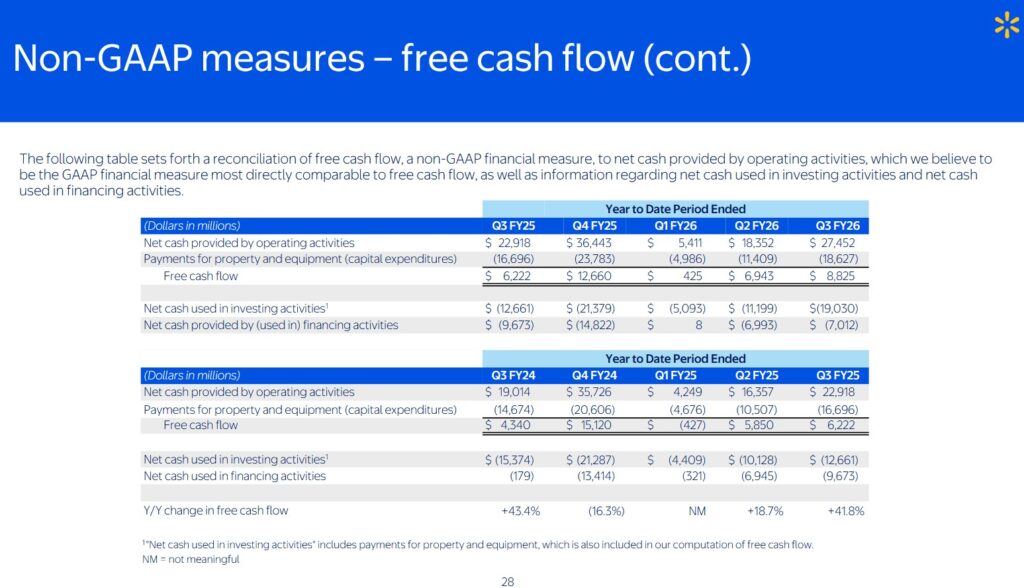

As evidence of the inconsistency in calculating a company’s FCF, I provide the following from WMT’s Q3 2025 earnings presentation.

We see that WMT’s YTD2026 FCF totals total ~$8.825B versus my calculation of ~$8.894B. The ~$0.041B variance is because I add back ~$0.069B of proceeds from disposal of property and equipment.

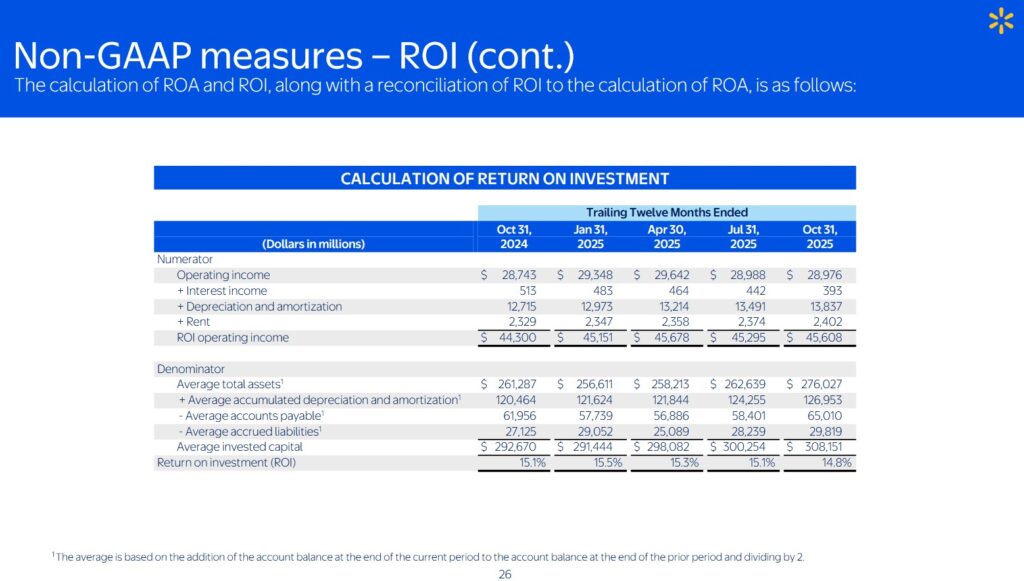

Return On Invested Capital (ROIC)

High quality companies often generate a high ROIC. If a company generates a high ROIC, it needs to invest less to achieve a certain growth rate thus reducing the need for external capital.

When a company consistently generates a high ROIC over the long term and it is growing its revenue, it can reinvest a portion of its profits under favorable conditions thereby leading to a compounding effect. I would much rather invest in a growing company that can reinvest to create greater shareholder value than to invest in a company that has limited growth opportunities and thus chooses to distribute a growing dividend.

A company that generates $0.15/profit for every $1 invested, for example, achieves a ROIC of 15%. I consider a ~15%+ ROIC to be a reasonable minimum threshold because most of the time, a company’s cost of capital will be lower than this level.

WMT’s ROIC calculation has slipped below 15%. Investors, however, should not be alarmed. Management, undoubtedly, pays particularly close attention to this metric. The appropriate measures are likely being taken to address this deteriorating trend.

Capital Allocation

In my prior post I reflect the following comment made by WMT’s management on the Q2 2026 earnings call:

I think we’re very fortunate to be a company that has so many opportunities to invest a dollar for high returns.

As I’ve said before, though, every dollar has to compete for that highest return. And I think we’re fortunate to have opportunities to invest in ourselves in things like technology, AI, supply chain automation to drive returns in some cases, in the 20% range. Because we generate a fair amount of free cash flow we have an opportunity to be balanced there. And in the most recent quarter, we also were aggressive in buying back more stock. Year-to-date, we bought back over $6 billion of our shares, and that’s 50% more than we did all of last year.

And so as the market dislocated a little bit with some of the concerns around tariffs earlier in the year, we were more aggressive, and we’ll continue to be aggressive buyers of our stock when we see prices dislocate because of all the things that you’ve heard today.

We have a lot of conviction in our plan. We like where we’re going. We like our strategy, and we believe that that’s going to generate returns well in excess of what we’ve done historically.

Nothing regarding WMT’s capital allocation has changed since that call.

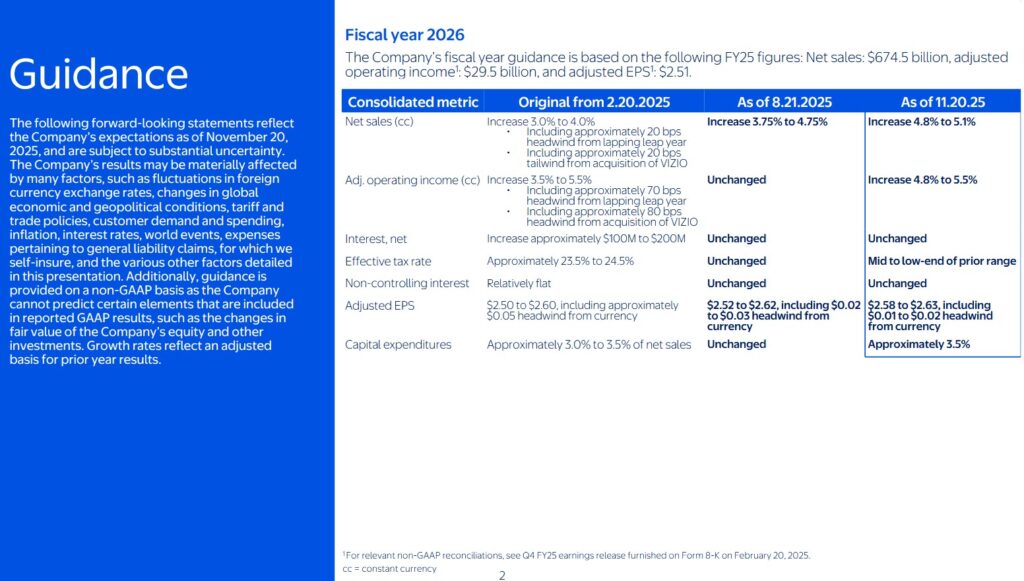

Q4 and FY2026 Guidance

The following reflects WMT’s most recent guidance.

On the Q3 earnings call, management states:

Recall at our Investor Day in April, on the heels of the tariff announcements, we said that we’re going to play offense. We said that we would look to gain share. Despite some of the obvious headwinds, we’re not giving up on our goal of growing profits faster than sales.

Given the YTD performance and our outlook for Q4, we’re raising our guidance for sales and operating income for the year.

Full year sales in constant currency is expected to grow between 4.8% – 5.1%, up from 3.75% – 4.75% prior. This reflects our confidence in our team’s ability to continue driving share gains in Q4. Fourth quarter constant currency sales guidance is for growth of 3.75% – 4.75%. Notably, if currency exchange rates stay where they are today for the entire fourth quarter, we would expect a $1.1B benefit to reported sales growth.

For operating income, we expect full year growth in a range of 4.8% – 5.5% on a constant currency basis, with Q4 growth in a range of 8% – 11%. Currency is expected to be an approximate 100 bps benefit to fourth quarter reported operating income growth.

Importantly, despite 150 bps of headwinds from the VIZIO acquisition and lapping leap year, as well as higher-than-expected claims expense, we still expect to grow operating income faster than sales for the year, which aligns with our longer-term financial framework.

For Q4, our operating income guide reflects the timing shift of Flipkart’s BBD event as well as the lapping of wage investments in Sam’s Club U.S. Business mix will continue to be a margin benefi and we expect merchandise category mix to continue to be a headwind.

For adjusted EPS, we expect the full year to be $2.58 – $2.63 with Q4 in of $0.67 – $0.72.

The consumer environment remains dynamic, and we continue to monitor customer member behavior alongside tracking the macro environment.

Risk Assessment

Some investors fixate on an investment’s potential return and overlook the various risk aspects of the investment to their detriment. This is why I strongly encourage investors to read the ‘Risks’ section of a company’s Form 10-K.

The Q3 2026 Form 10-Q is currently unavailable as I compose this post, and therefore, I continue to provide the above which is extracted from the Q2 2026 Form 10-Q.

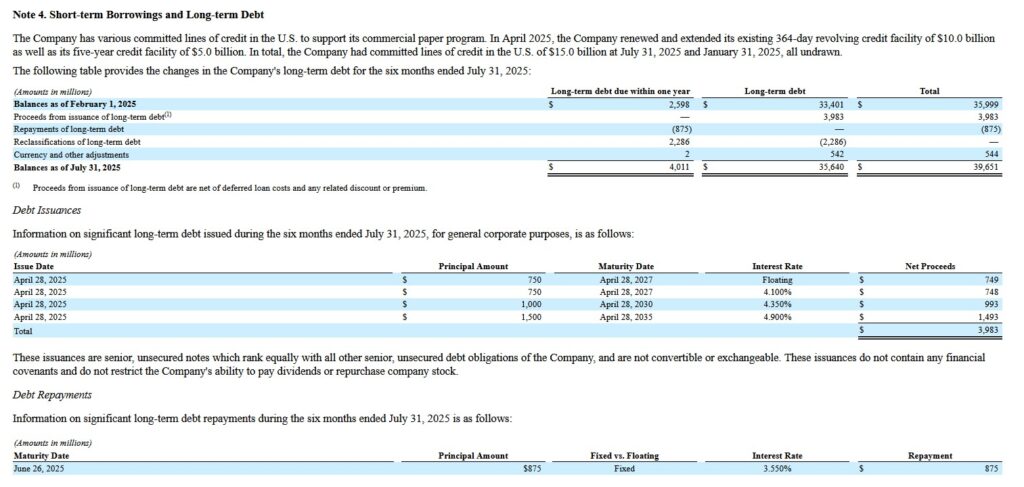

At the end of Q3, however, short-term borrowings amounted to $8.401B and long-term debt amounted to $34.445B for a total of $42.846B versus $39.651B at the end of Q2. Although a $3.195B variance is meaningful when viewed in isolation, it is not significant when we step back and look at the big picture. Investors should not be alarmed by this increase.

I try to assess a company’s risk independently from how the rating agencies perceive a company’s risk. Nevertheless, I do look at their ratings to ascertain whether our opinion about a company’s risk is similar.

WMT’s current domestic long-term unsecured debt ratings and outlook are:

- Moody’s: Aa2 (stable) last reviewed October 13, 2022.

- S&P Global: AA (stable) last reviewed April 22, 2025.

- Fitch: AA (stable) last reviewed October 7, 2025.

All 3 ratings are the middle tier of the high-grade investment-grade category.

These ratings define WMT as having a very strong capacity to meet its financial commitments. It differs from the highest-rated obligors only to a small degree.

Dividend and Dividend Yield

WMT’s dividend history is accessible here. WMT declared a 3 for 1 stock split in February 2024. Investors should not get the idea that WMT cut its quarterly dividend in early 2024.

The table in the Conventional Free Cash Flow (FCF) Calculations (FY2020 – FY2025 and YTD2026) section of this post reflects the extent to which WMT has been reducing the weighted average shares outstanding.

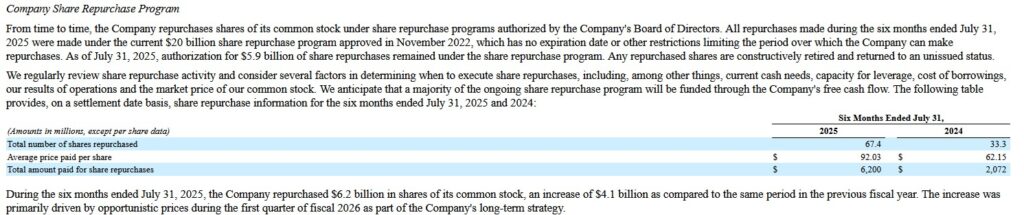

The following is from WMT’s Q2 2026 Form 10-Q.

In the first 6 months of FY2026, WMT repurchased ~$6.2B of its its outstanding shares. By the end of Q3 2026, this had risen to $7.008B. I anticipate WMT will continue to allocate some of its capital toward share repurchases.

Valuation

The following reflects my assessment of WMT’s valuation at the time of my October 18 post:

WMT’s FY2026 outlook calls for non-GAAP EPS of ~$2.52 – ~$2.62. Using the current ~$107.73 share price, the forward adjusted diluted PE is ~41.1 – ~42.75.

Its valuation using the current broker guidance is:

- FY2026 – 36 brokers – mean of $2.61 and low/high of $2.55 – $2.71. Using the mean, the forward adjusted diluted PE is ~41.3.

- FY2027 – 37 brokers – mean of $2.93 and low/high of $2.75 – $3.14. Using the mean, the forward adjusted diluted PE was ~36.8.

- FY2028 – 22 brokers – mean of $3.27 and low/high of $3.04 – $3.67. Using the mean, the forward adjusted diluted PE was ~33.

WMT has generated FCF of ~$6.984B in the first half of FY2026. If it generates a comparable amount of FCF in the second half of FY2026, it should generate ~$14B for the year. Furthermore, let’s assume the weighted average shares outstanding for the year declines to 7.9B. This gives us ~$1.77 of FCF/share or a P/FCF of ~60.9.

If WMT were to generate ~$14B of FCF and the weighted average shares outstanding for the year were to decline to 7.7B, we get ~$1.82 of FCF/share giving us a P/FCF of ~59.2.

Should the share price drop to ~$90, and we use ~$1.80 FCF/share, the P/FCF becomes ~50. Using ~$2.61 in FY2026 adjusted diluted EPS, and ~$90/share, the P/E is ~34.5.

We now know that WMT has generated $2.20 and $1.91 of YTD diluted EPS and adjusted diluted EPS in the first 3 quarters of Fy2026 and the revised outlook is for $2.58 – $2.63 of adjusted diluted EPS. I envision FY2026 diluted EPS will likely be ~$2.85 – ~$2.91.

Using the November 29 $107.11 closing share price, the forward adjusted diluted PE is ~40.7 – ~41.5.

Its valuation using the current broker guidance is:

- FY2026 – 38 brokers – mean of $2.63 and low/high of $2.56 – $2.75. Using the mean, the forward adjusted diluted PE is ~40.7.

- FY2027 – 37 brokers – mean of $2.95 and low/high of $2.75 – $3.15. Using the mean, the forward adjusted diluted PE was ~36.3.

- FY2028 – 26 brokers – mean of $3.28 and low/high of $3.05 – $3.71. Using the mean, the forward adjusted diluted PE was ~32.7.

WMT has generated FCF of ~$8.894B in the first 3 quarters of FY2026. The company, however, typically generates ~27% – ~30% of its annual revenue in Q4. I am, therefore, inclined not to merely increase WMT’s YTD FCF by just ~33.33% (~$8.894B /3 = ~4.96B) and will stick with my ~$14B of FCF for the year estimate I used in my October 18 post.

In Q3, the weighted-average common shares outstanding was 8.011B. I anticipate WMT will repurchase additional shares in Q4. However, rather than assume 7.9B as the weighted average shares outstanding for the year, I am revising my estimate to 8B.

Using my $14B FY2026 FCF estimate and 8B shares, the FCF/share is likely to be ~$1.75. Divide the current $107.11 share price by ~$1.75 and the P/FCF is ~61.2.

If my FY2026 $14B FCF estimate comes in closer to ~$12.5B, for example, and the share count comes in closer to 7.9B, the FCF/share is ~$1.58. Divide the current $107.11 share price by ~$1.58 and the P/FCF is ~67.8.

If we suspend reality and assume WMT generates $20B of FCF in FY2026 and the share count comes in at 7.5B, we get ~$2.67 of FCF/share. Divide the current $107.11 share price by ~$2.67 and the P/FCF is ~40.1.

Should the share price drop to ~$90, and we use ~$1.75 FCF/share, the P/FCF becomes ~51.4. Using a ~$90 share price and ~$2.67 of FCF/share, the P/FCF is ~33.7.

If I use ~$2.61 in FY2026 adjusted diluted EPS and ~$90/share, the P/E is ~34.5.

Whatever way I look at WMT from a valuation perspective, shares appear to currently be very richly valued.

Final Thoughts

My thoughts on WMT’s valuation are the same as in my October 18 post. WMT’s valuation is rich, and therefore, I have no immediate plans to increase my exposure.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long WMT.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.