![]()

When I reviewed CME Group (CME) in my October 25, 2025 post, it had recently released its Q3 and YTD2025 results. In that post I express my optimism that CME will start repurchasing shares. Given this optimism I purchased an additional 100 shares @ $266.875 on January 6, 2026 in a ‘Core’ account in the FFJ Portfolio and disclose this purchase in my January 6, 2026 post.

While CME repurchased shares in FY2025, the amount was only $0.2661B. Subsequent to FYE2025, CME repurchased another $0.276B.

Business Overview

CME operates a derivatives marketplace which offers a range of futures and options products for risk management. It is where market participants turn to manage risk across the most diverse set of benchmark products.

The company’s website and Part 1 of the FY2025 Form 10-K are great source of information to learn more about the company.

Financials

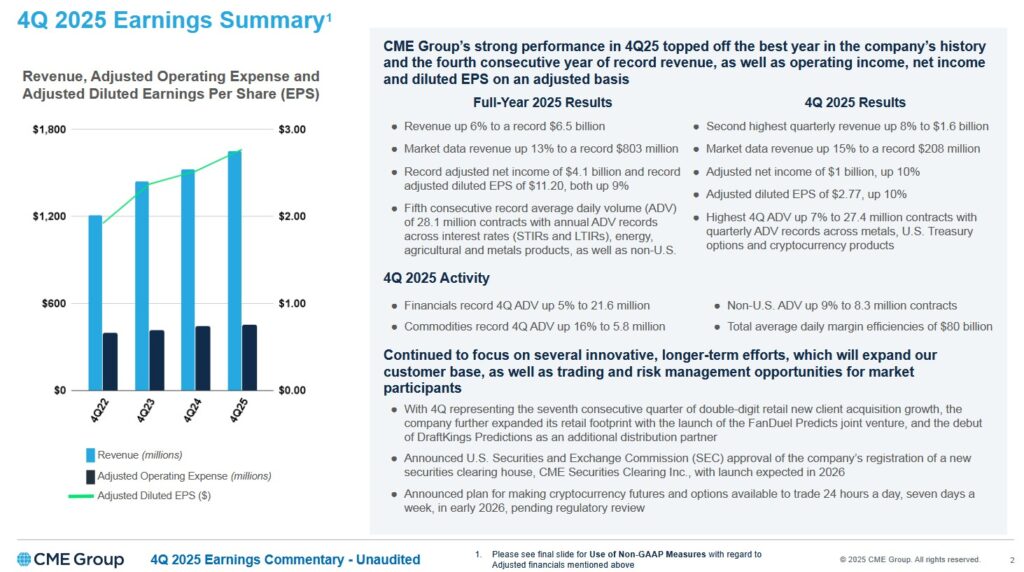

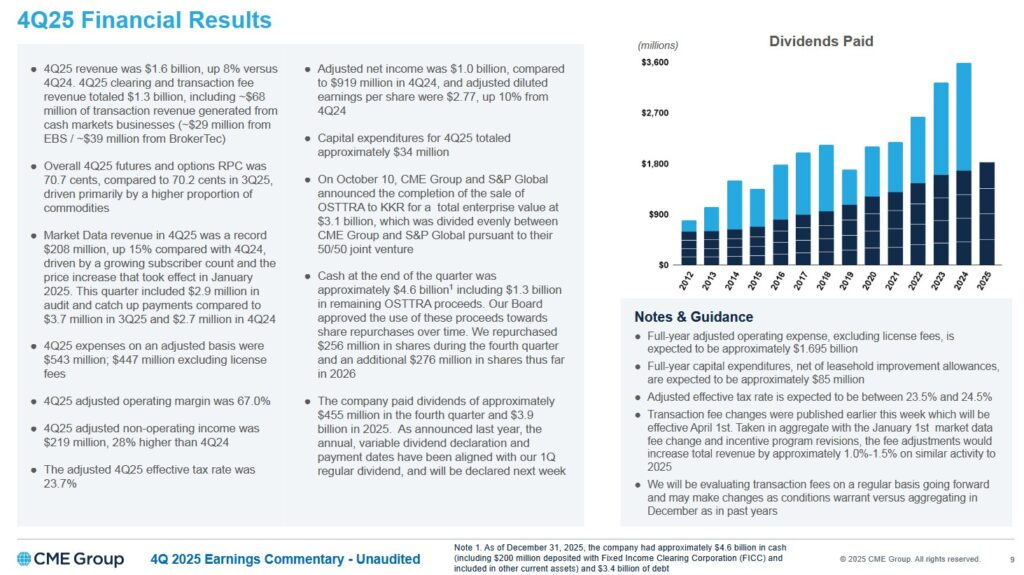

Q4 and FY2025 Results

The Q4 and FY2025 earnings release is accessible through the SEC Filing section of the company’s website.

The following is a summary of CME’s Q4 and FY2025 results.

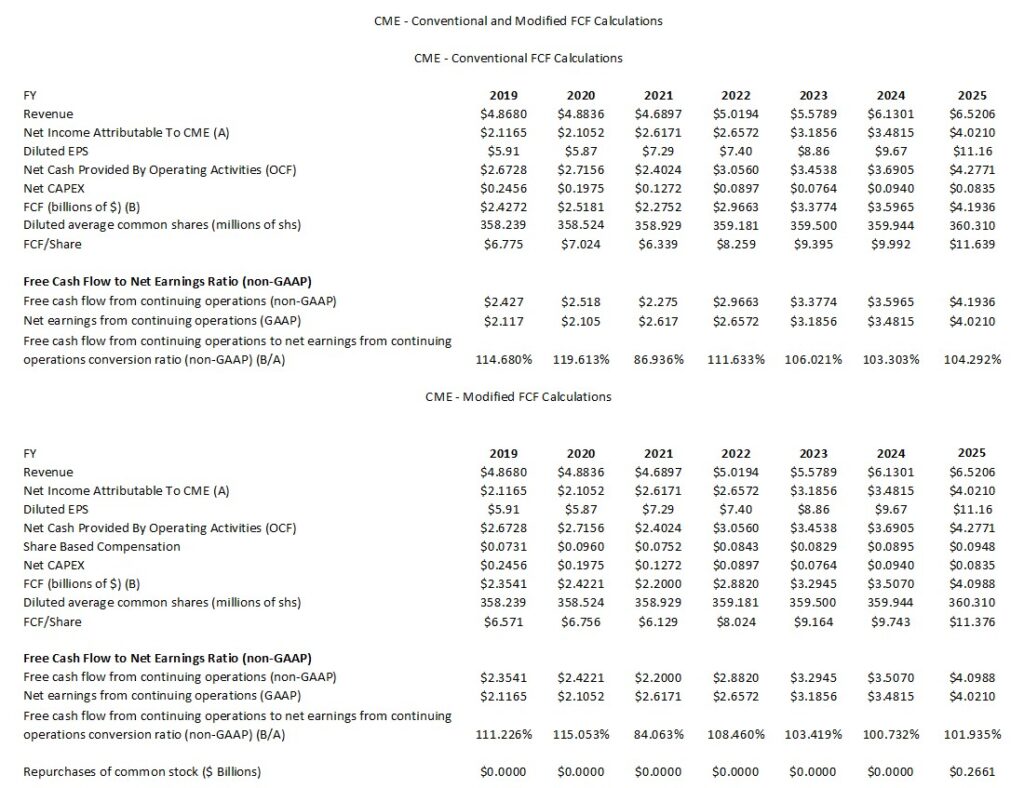

Conventional And Modified Free Cash Flow (FCF) Calculations (FY2019 – FY2025)

FCF is a non-GAAP measure, and therefore, its calculation is inconsistent. Many investors deduct CAPEX from OCF to arrive at FCF. In my How Stock Based Compensation Distorts Free Cash Flow post, I explain why I now also deduct stock based compensation (SBC) that is found in the Consolidated Statements of Cash Flows to determine FCF.

The conventional method only deducts CAPEX from OCF while the more conservative modified method also deducts SBC.

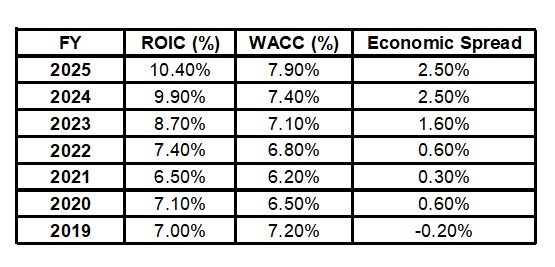

ROIC and WACC

Return on Invested Capital (ROIC) provides an indication of a company’s efficiency. In essence, is a company actually creating value or ‘burning’ cash for the sake of growth?

A company with a higher ROIC is mathematically worth more because it requires less reinvestment to achieve that growth.

A good indication of how well a company is performing is to compare ROIC to the Weighted Average Cost of Capital (WACC). WACC, however, is not a metric officially reported by CME but it can be roughly estimated based on the company’s credit profile and market conditions.

The generally accepted high-level formula used by Wall Street is:

ROIC = NOPAT/Average Invested Capital

with the Net Operating Profit After Tax (NOPAT) formula being Operating Income (EBIT) x (1-tax rate)

This shows how much profit the core business makes while ignoring how much debt the company has.

The Average Invested Capital is the total money tied up in the business.

- The Operating Approach formula is

- The Financing Approach is

CME Group’s ROIC has seen a steady upward trajectory since 2021. This has been driven by record average daily volumes (ADV) as market participants sought hedging tools amid global interest rate volatility. CME’s cost of capital dipped in 2021 during the low-interest-rate environment. It has, however, risen tracking with broader market rate hikes and equity risk premiums.

CME’s cost of capital dipped in 2021 during the low-interest-rate environment. It has, however, risen tracking with broader market rate hikes and equity risk premiums.

FY2025 Guidance

CME does not issue earnings guidance. On the Q4 2025 earnings call, however, management provides the following:

We expect total adjusted operating expenses excluding license fees to be ~$1.695B.

We are dedicated to continuously evolving our product set and offerings, a commitment that requires strategic investment for growth. Total capital expenditures are expected to be ~$85 million, and the adjusted effective tax rate should come in between 23.5%-24.5%.

Risk Assessment

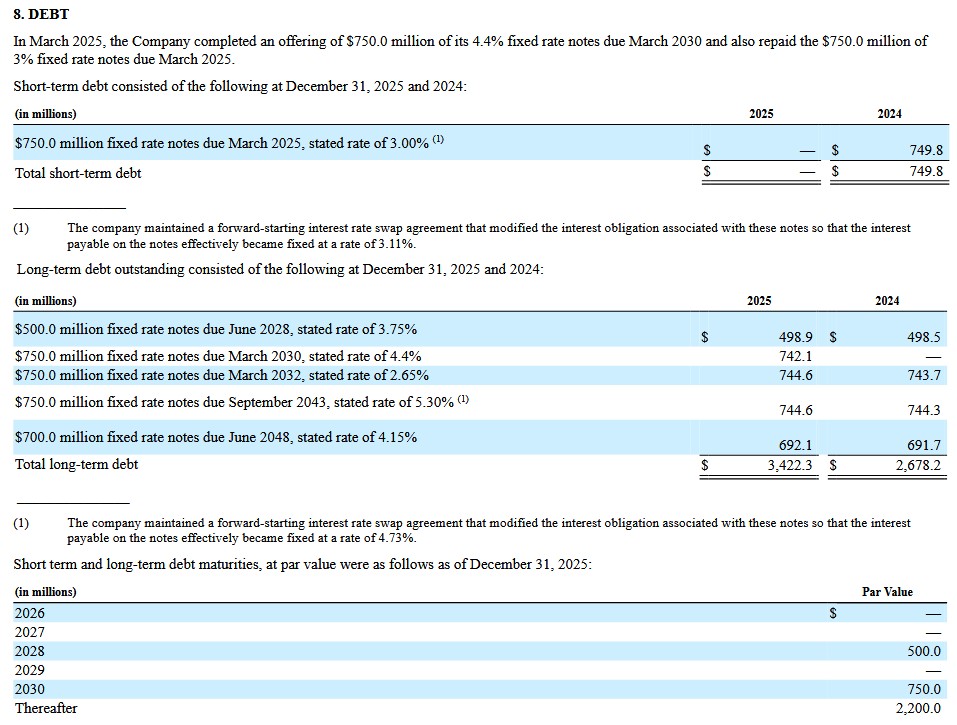

In March 2025, CME completed an offering of $750.0 million of its 4.4% fixed rate notes due March 2030 and also repaid the $750.0 million of 3% fixed rate notes due March 2025. CME now has no debt maturing until FY2028.

CME’s senior unsecured long-term debt ratings are the lowest tier of the high-grade category and are investment grade. These ratings define CME as having a VERY STRONG capacity to meet its financial commitments. It differs from the highest-rated obligors only to a small degree.

- Moody’s: Aa3 with a stable outlook (affirmed May 19, 2025)

- S&P Global: AA- with a stable outlook (affirmed July 18, 2025)

- Fitch: AA- with a stable outlook (affirmed February 2, 2026)

These strong ratings are acceptable for my risk tolerance.

Dividend and Dividend Yield

Dividend distributions continue to take priority over share repurchases with FY2025 distributions being $3.933B.

CME has also declared a $6.15 special dividend to be paid on March 26, 2026 AND it increased its quarterly dividend from $1.25 to $1.30 (also payable on March 26).

The following is reflected in CME’s FY2025 Form 10-K.

We intend to continue to pay a regular quarterly dividend to our shareholders, with a target of between 50% to 60% of the prior year’s cash earnings. The decision to pay a dividend and the amount of the dividend, however, remains within the discretion of our board of directors and may be affected by various factors, including our earnings, financial condition, capital requirements, levels of indebtedness and other considerations our board of directors deems relevant. We are also required to comply with restrictions contained in the general corporation laws of our state of incorporation, which could limit our ability to declare and pay dividends.

CME’s dividend history is accessible here.

In FY2014, the weighted average outstanding diluted shares outstanding (in millions of shares rounded) was 336.063. In FY2025, CME repurchased $0.2661B and the weighted average outstanding diluted shares outstanding amounted to 360.310. Subsequent to FYE2025, CME repurchased $0.276B.

Valuation

In my January 6, 2026 post I reflect the following:

On January 6, 2026, I acquired an additional 100 shares @ $266.875. Using the current forward adjusted diluted EPS broker estimates, CME’s forward adjusted diluted PE levels are:

- FY2025 – 14 brokers – mean of $11.18 and low/high of $10.98 – $11.33. Using the mean estimate, the forward-adjusted diluted PE is ~23.9.

- FY2026 – 14 brokers – mean of $11.67 and low/high of $11.15 – $12.25. Using the mean estimate, the forward-adjusted diluted PE is ~22.9.

- FY2027 – 9 brokers – mean of $12.38 and low/high of $11.66 – $13.26. Using the mean estimate, the forward-adjusted diluted PE is ~21.6.

As I compose this post on March 24, 2026, the share price is ~$303.60. Using the current forward adjusted diluted EPS broker estimates, CME’s forward adjusted diluted PE levels are:

- FY2026 – 13 brokers – mean of $12.10 and low/high of $11.74 – $12.79. Using the mean estimate, the forward-adjusted diluted PE is ~25.1.

- FY2027 – 13 brokers – mean of $12.75 and low/high of $11.98 – $13.56. Using the mean estimate, the forward-adjusted diluted PE is ~23.8.

- FY2028 – 8 brokers – mean of $13.78 and low/high of $12.76 – $14.82. Using the mean estimate, the forward-adjusted diluted PE is ~22.03.

CME’s valuation based on forward adjusted diluted EPS estimates is greater than at the time of my January 6, 2026 post.

CME’s modified FCF conversion ratio is slightly higher than 100% which suggests CME’s P/modified FCF (share) valuation is just slightly better than its P/E. Nevertheless, I think CME is somewhat overvalued with a fair price being ~$255 – ~$265.

Final Thoughts

CME was my 11th largest holding when I completed my 2025 Mid-Year Portfolio Review and it was my 14th largest holding when I completed my 2025 Year-End Investment Holdings Review.

I currently hold 579.83868 shares in in a ‘Core’ account and 414 shares in a ‘Side’ account within the FFJ Portfolio.

On March 26 I will receive $7.45 in dividends per share. After deducting a 15% withholding tax, the net proceeds will be automatically reinvested to acquire additional shares.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long CME.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.