Veeva Systems (VEEV) is no longer a bargain unlike when I wrote various previous posts that are accessible through the Archives section of this site. In several of those posts, I disclosed my decision to acquire undervalued VEEV shares within a ‘Core’ account in the FFJ Portfolio.

When I published my most recent VEEV post on March 6, 2025, I stated that VEEV no longer appeared to be a ‘bargain’. At the time, the most current financial information was for Q4 and FY2025.

Following the May 28 market close, VEEV released its Q1 2026 results and revised FY20026 outlook (the company has a January 31 fiscal year end).

As I compose this post on May 29, VEEV’s ~$279 share price has surged ~$45 from the prior day’s close.

Despite VEEV’s attractive long-term prospects, I do not consider this to be an opportune time to acquire additional shares.

Business Overview

VEEV is the leading provider of industry cloud solutions for the global life sciences industry. Its offerings span cloud software, data, and business consulting and are designed to meet customers’ unique needs and their most strategic business functions ranging from R&D through commercialization. These solutions help life sciences companies develop and bring products to market faster and more efficiently, market and sell more effectively, and maintain compliance with government regulations.

The best way to learn about the company is to review the company’s website and Part 1 in the most recent Form 10-K found in the SEC Filings section of the company’s website.

In 2019, VEEV set an ambitious target of achieving $3B of annual revenue by 2025. This is disclosed in the Financial Analyst and Investor Day presentation that is accessible through the News and Events section within the Investor portal on the company’s website.

In Q1 2026, VEEV achieved its 2025 revenue run rate goal of $3B. Building on this foundation and the strong start to FY2026, VEEV is focusing on its 2030 goals to double revenue to $6B. This goal was announced on

Financial Review

Q1 2026

Material related to the Q1 2026 earnings release is accessible here.

VEEV spends a considerable amount on research and development (R&D). In Q1 2026, its R&D expense amounted to ~$0.184B versus ~$0.163B in Q1 2025.

To date, this R&D investment has enabled it to develop small products into fast-growing assets when viewed from the perspective of customer penetration and new customer wins; the company has had a number of top 20 pharma wins across its platform.

The impact tariffs are likely to have on a company’s operations is a topic raised on all recent earnings calls.

VEEV’s management does not anticipate any material impact from tariffs on its near-term financial performance. Its subscription services (85% of sales and 90% of operating income) are largely immune to volatility because they are either on an annual or long-term basis. Professional services and other revenue could have exposure to macro uncertainty. The Q1 2026 results, however, do not suggest any weakness in FY2026 as borne out by the company having just slightly raised professional services revenue guidance.

I strongly encourage you to read management’s prepared remarks for its Q1 2026 earnings call. Nevertheless, I provide the following from the prepared remarks for ease of access.

Macroenvironment

Recent changes and uncertainty in U.S. policies are causing some distractions and potential challenges as we look ahead. In general, lack of clarity on tariffs and geopolitical tensions are not good for economic activity, especially for global industries like life sciences that depend on stable environments due to their long investment cycles. There is uncertainty around the recent executive order on drug pricing and FDA staffing changes and shortages may impact FDA drug approval timelines and policies.

It’s a highly dynamic environment. Persistent pressure and uncertainty could result in greater conservatism in large biopharma and negatively impact the funding environment for emerging biotechs. Discussions with customers are starting to reflect this general unease. However, we have not seen a material change to our financial results or pipeline at this time.

To the positive, as we have seen in the past, high quality and profitable companies like Veeva benefit from a flight to quality in uncertain times with customers and employees. When core capability projects are delayed due to uncertainty, it creates pent-up demand that will be fulfilled at some point in the future. We also see continued scientific innovation in the industry which will fuel long-term growth.

Our annual guidance takes into consideration all the things we see at this time, and we remain committed to our 2030 revenue targets.

Achieving Our Long-Term Goals and Crossing $3 Billion

Veeva has a history of setting and achieving ambitious long-term goals to advance the company and the industries we serve. In 2019, we set a goal to achieve a $3 billion revenue run rate in calendar 2025, which we crossed this quarter.

We now have a $6 billion revenue run rate goal for life sciences in 2030. I am encouraged by the progress we are making as we look to double the positive impact we can have on the industry and for patients.

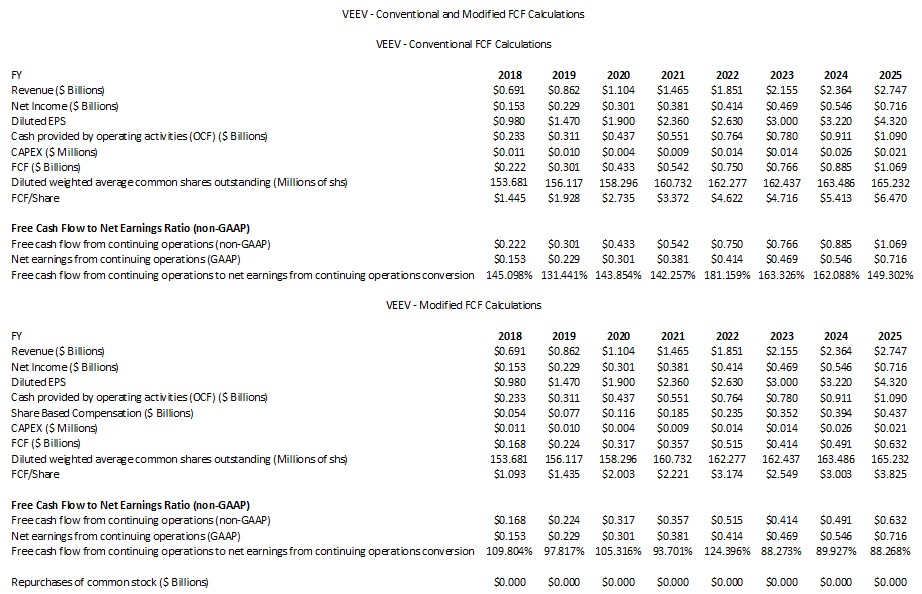

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX

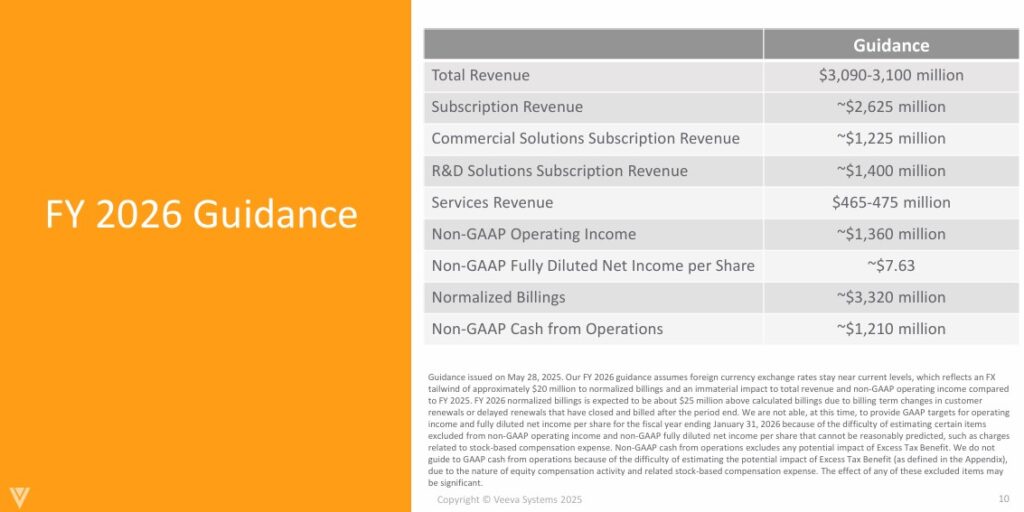

VEEV reports the following annual OCF over the past few years. Its previous FY2026 OCF guidance was ~$1.170B and the non-GAAP OCF margin was 38%.

VEEV deducts CAPEX from OCF to calculate its FCF. In prior posts, however, I explain my rationale for also deducting share-based compensation (SBC) from a company’s OCF.

The following reflects VEEV’s FCF using the conventional and modified methods.

In Q1 2026, VEEV’s Net cash provided by operating activities was ~$0.877B, CAPEX was ~$6 million, and the weighted average diluted shares outstanding was 166.229 million.

In Q1 2025, VEEV’s Net cash provided by operating activities was ~$0.7635B, CAPEX was ~$8.5 million, and the weighted average diluted shares outstanding was 164.4 million.

Its stock based compensation (SBC) in Q1 2026 was ~$0.1122B versus ~$0.096B in Q1 2025.

The Net cash provided by operating activities is ~$0.1135B (~$0.877B – ~$0.7635B) higher in Q1 2026 versus Q1 2025. The increase in CAPEX and SBC, fortunately, is only ~$15 million.

SBC and not CAPEX has a material impact when calculating VEEV’s FCF.

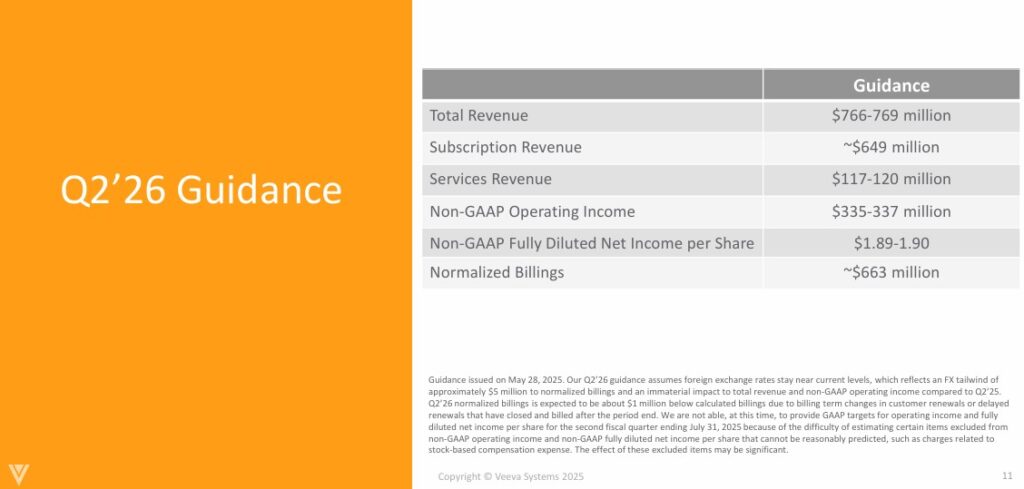

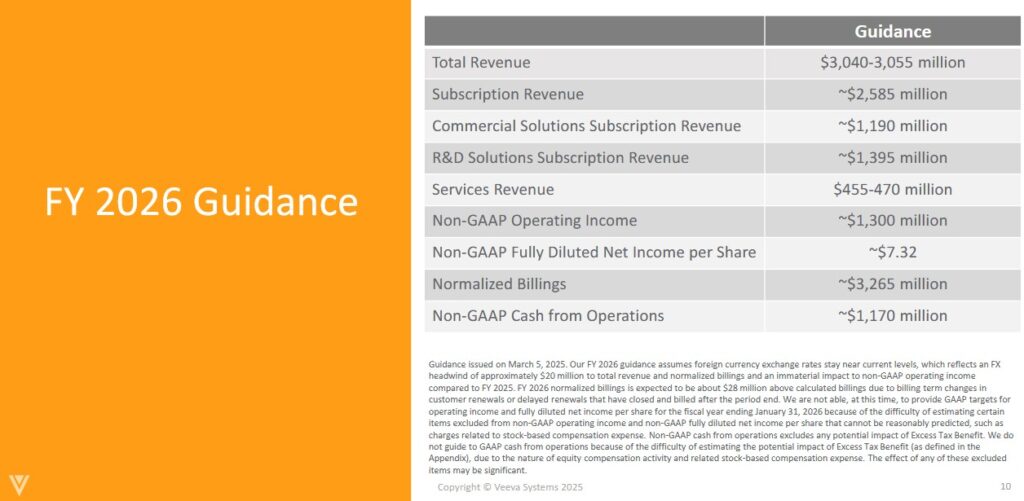

Q2 and FY2026 Outlook

The following reflects VEEV’s current outlook.

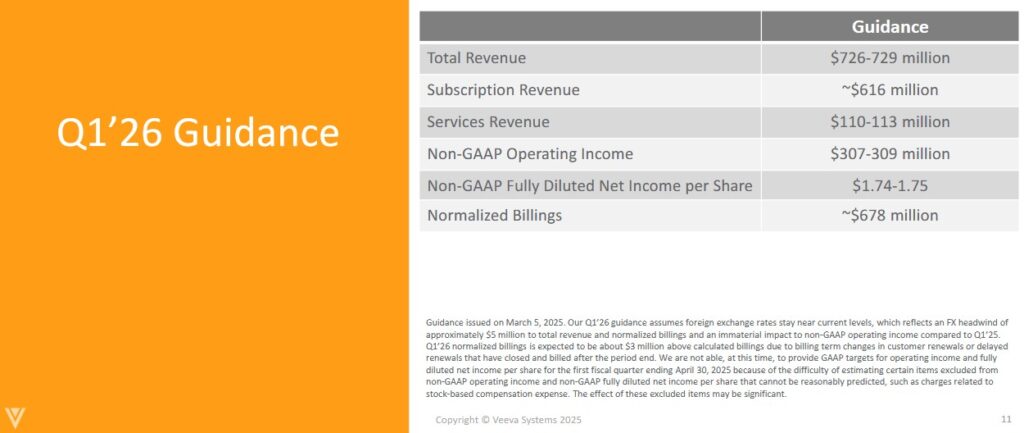

The following reflects VEEV’s prior outlook.

Risk Assessment

VEEV has no debt to rate.

At the end of Q1 2026, VEEV had ~$1.965B in cash and cash equivalents and ~$4.103B in short-term investments for a total of ~$6.068B. In comparison, it had:

- ~$1.119B and ~$4.031B for a total of ~$5.15B at FYE2025; and

- ~$0.703B and ~$3.324B for a total of ~$4.027B at FYE2024.

Its total liabilities at the end of Q1 2026 was ~$1.554B of which ~$1.246B was deferred revenue leaving ~$0.308B in all other liabilities. In comparison, it had:

- ~$1.507B in total liabilities of which ~$1.274B was deferred revenue leaving ~$0.233B in all other liabilities at FYE2025; and

- ~$1.266B in total liabilities of which ~$1.050B was deferred revenue leaving ~$0.216B in all other liabilities at FYE2024.

Deferred revenue represents funds received from clients in advance of services being provided.

VEEV satisfies my risk-averse investor profile.

Dividends and Dividend Yield

VEEV does not distribute a dividend.

The weighted average number of diluted shares outstanding (in millions rounded) in FY2021 – 2025 is 160.7, 162.2, 162.4, 163.5, and 165.2. At the end of Q1 2026, this had risen to 166.2.

If I have one concern about VEEV, it is the extent to which it compensates employees by way of SBC. VEEV typically does not repurchase shares to offset the shares it issues annually as part of its employee compensation structure. At some point, the increase in the weighted average number of diluted shares outstanding will need to be addressed.

VEEV’s CEO sits on Zoom Communications’ (ZM) Board. ZM has lowered the extent to which it compensates employees by way of SBC and it has relatively recently begun to repurchase shares. At some point, I anticipate that VEEV may begin to use its cash horde to repurchase shares.

Valuation

Broker earnings estimates are currently under revision. At the moment, however, the following are VEEV’s forward adjusted diluted PE levels using the current broker estimates and a ~$279 share price.

- FY2026 – 29 brokers – mean of $7.50 and low/high of $7.17 – $7.76. Using the mean estimate, the forward adjusted diluted PE is ~37.2.

- FY2027 – 29 brokers – mean of $8.24 and low/high of $7.58 – $8.69. Using the mean estimate, the forward adjusted diluted PE is ~33.9.

- FY2028 – 12 brokers – mean of $9.38 and low/high of $8.56 – $10.10. Using the mean estimate, the forward adjusted diluted PE is ~29.7.

I place no reliance on earnings estimates beyond the current fiscal year (FY2026).

VEEV’s FY2026 outlook calls for ~$1.21B of Operating Cash Flow. If we estimate that FY2026 annual CAPEX is similar to the last couple of fiscal years, we can conservatively use $30 million to determine FCF.

Under the conventional method of calculating FCF (OCF less CAPEX) we get ~$1.18B.

VEEV does not repurchase shares so being conservative, we can estimate that the weighted average number of diluted shares outstanding in FY2026 will increase by ~2 million shares. In FY2025, the weighted average was ~165.232 million shares so in FY2026, we can anticipate ~167.232 million.

Divide $1.18B of FCF by ~167.232 million shares and we get FCF/share of ~$7.06. With shares currently trading at ~$279, the forward P/FCF is ~39.5.

If we estimate SBC of ~$0.480B for FY2026 representing an increase of ~$43 million which is consistent with the past couple of fiscal years, we can deduct this amount from the ~$1.18B of FCF calculated under the conventional method. Under the modified method, FCF becomes ~$0.7B. Divide this by ~167.232 million shares and we get FCF/share of ~$4.19. With shares currently trading at ~$279, the forward P/FCF is ~66.6.

The following were my prior calculations using the broker estimates and a ~$242 share price:

- FY2026 – 31 brokers – mean of $7.11 and low/high of $5.06 – $7.45. Using the mean estimate, the forward adjusted diluted PE is ~34.1.

- FY2027 – 25 brokers – mean of $7.88 and low/high of $5.87 – $8.55. Using the mean estimate, the forward adjusted diluted PE is ~30.7.

- FY2028 – 6 brokers – mean of $8.96 and low/high of $8.46 – $9.39. Using the mean estimate, the forward adjusted diluted PE is ~27.

VEEV’s FY2026 outlook calls for ~$1.17B of Operating Cash Flow versus ~$1.090B in FY2025. If we estimate that FY2026 annual CAPEX will be similar to the last couple of fiscal years, we can conservatively use $30 million to determine FCF.

Under the conventional method of calculating FCF (OCF less CAPEX) we get ~$1.06B.

VEEV does not repurchase shares so being conservative, we can estimate that the weighted average number of diluted shares outstanding in FY2026 will increase by ~2 million shares. In FY2025, the weighted average was ~165.232 million shares so in FY2026, we can anticipate ~167.232 million.

Divide $1.06B of FCF by ~167.232 million shares and we get FCF/share of ~$6.02 versus ~$6.47 in FY2025. With shares currently trading at ~$242, the forward P/FCF is ~40.2.

If we estimate SBC of ~$480 for FY2026 representing an increase of ~$43 million which is consistent with the past couple of fiscal years, we can deduct this amount from the ~$1.06B of FCF calculated under the conventional method. Under the modified method, FCF becomes ~$0.58B. Divide this by ~167.232 million shares and we get FCF/share of ~$3.47 versus ~$3.825 in FY2025. With shares currently trading at ~$242, the forward P/FCF is ~69.7.

VEEV is a good example of the extent to which SBC impacts valuations based on FCF !

Final Thoughts

VEEV was not a top 30 holding when I completed my 2024 Mid Year Portfolio Review. It, however, was my 28th largest holding when I completed my 2024 Year End Portfolio Review.

My average cost on 500 shares in $207.2545. Purchasing another 200 shares at ~$279 would raise my average cost to ~$227.75 which is still well below VEEV’s fair value.

Although VEEV has a promising outlook and the probability of it doubling its revenue to $6B by 2030 is realistic, investor behavior suggests that we are now in another period of ‘irrational exuberance’.

In my March 6, 2025 post I wrote:

I intend to increase my VEEV exposure, however, shares currently trade at ~$242 and a fair value is ~$250. This suggests a sub-4% upside before VEEV reaches fair value which is insufficient if the current rate of inflation is ~2% – 3%. I would like to acquire additional shares if the share price retraces to ~$220 or lower. At this level, VEEV’s P/FCF using the conventional FCF method of calculation would be ~36.5 (~$220/~$6.02).

Recent results now suggest a fair value is closer to ~$275 – ~$280. With shares trading at ~$279, shares already appear to be fairly valued.

I could justify adding to my exposure in VEEV despite a ~33% YTD share price surge IF its valuation was appealing. VEEV’s current valuation, however, is even less attractive than at the time of my March 6, 2025 post. I will, therefore, bide my time and look for other investment opportunities.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long VEEV.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.