![]()

The return on my Paycom (PAYC) investment has been less than stellar. The company’s underlying fundamentals and growth potential, however, remain sound. Given this, I acquired an additional 100 shares @ $162.1148/share on November 6, 2025 in a ‘Core’ account in the FFJ Portfolio.

I last reviewed this existing holding in my May 8, 2025 post at which time the most current financial information was for Q1 2025. At the time, I did not like PAYC’s valuation. With the release of Q3 2025 results following the November 5, 2025 market close, it is a good opportunity to revisit this existing holding.

Business Overview

PAYC provides cloud-based human capital management (HCM) solution delivered as software-as-a-service (SaaS) for small to mid-sized companies predominantly located in the United States. It is, however, slowly expanding its international capabilities to accommodate US companies with international operations.

PAYC offers functionality and data analytics that businesses need to manage the employment life cycle from recruitment to retirement. Its HCM solution provides a suite of applications in the areas of talent acquisition, including applicant tracking, background checks, on-boarding, e-verify, and tax credit services, and time and labor management, such as time and attendance, scheduling, time-off requests, and labor allocation solutions.

The best sources of information to learn about the company are PAYC’s website and the FY2024 Annual Report/Form 10-K.

Paycom IWant

On July 30, 2025, PAYC announced the launch of IWant, the industry’s first command-driven AI engine that enables all users navigate and access their information within a single database.

When I last reviewed PAYC following the release of Q1 2025 results, purchases of property and equipment was $37.3 million. At the end of Q3 2025, however, CAPEX has shot up to ~$0.1974B. This is because PAYC front-loaded a ~$0.1B CAPEX investment in advanced AI hardware and equipment within its Phoenix and Oklahoma City data centers. This spend is now largely complete and provides the company with a multiyear capacity runway to support its AI initiatives. The reason for front-loading this CAPEX was to match the timing of the introduction of IWant.

The one-time infrastructure costs associated with developing IWant were offset by strong operating cash flow growth. This strong cash flow growth should continue to compound for the foreseeable future.

Financials

Q3 and YTD2025 Results

Details of PAYC’s Q3 and YTD2025 results are accessible here and the Q3 2025 Form 10-Q is available here.

In FY2022 – FY2024, PAYC’s research and development (R&D) expenses amounted to $0.1483B, $0.199B, and $0.2426B. YTD2025, the R&D expense is $0.2112B with funding predominantly provided from cash generated through normal business operations.

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX

PAYC deducts CAPEX from its net cash provided by continuing operating activities to determine its FCF. I address my rationale for also deducting share based compensation (SBC) when determining FCF in my How Stock Based Compensation Distorts Free Cash Flow post.

NOTE: In my November 4, 2024 post I explain why FY2024 SBC is negative.

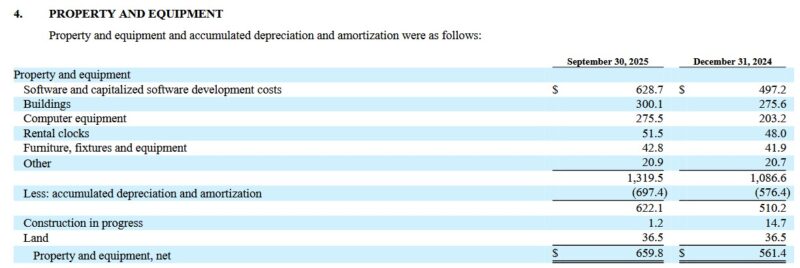

At FYE2019, PAYC’s net property and equipment was ~$0.2385B. At the end of Q3 2025 it is ~$0.66B. This ~$0.4215B increase has been financed almost exclusively from cash flow generated from normal business operations. The company has no debt on its balance sheet!

PAYC has invested almost $1.1B in R&D between FY2019 – Q3 2025, increased property and equipment by more than $0.4B (see above), has repurchased more than $0.775B of its shares (FY2019 – Q3 2025) and repurchased more shares after Q3 2025, and disbursed $0.2139B in the form of dividends since the first disbursement in June 2023. These figures alone total ~$2.5B…and this comes from a company that has generated only ~$9.1B of total revenue in FY2019 – Q3 2025.

FY2025 Outlook

The current FY2025 outlook is:

- Total revenue of $2.45B – $2.55B, representing YoY growth of ~9% at the midpoint.

- Recurring and other revenue growth of ~10% YoY.

- Interest on funds held for clients of ~$0.113B.

- Adjusted EBITDA of $0.872B – $0.882B, representing a margin of ~43% at the midpoint.

- Full year GAAP and non-GAAP tax rates of 27% and 26%, respectively.

- Stock compensation of ~7% of revenues.

PAYC’s FY2025 outlook when I wrote my May 8, 2025 post was:

- Total revenue of $2.023B – $2.038B, representing YoY growth of ~8% at the midpoint.

- Recurring and other revenue growth of ~9% YoY. Management expects the highest growth to occur in Q4.

- Interest on funds held for clients of ~$0.110B.

- Adjusted EBITDA of $0.843B – $0.858B, representing a margin of ~42% at the midpoint.

- Full year GAAP and non-GAAP tax rates of 28% and 27%, respectively.

- Stock compensation of ~8% of revenues.

PAYC’s FY2025 outlook released on February 12, 2025 was:

- Total revenue of $2.015B – $2.035B, representing YoY growth of ~8% at the midpoint.

- Recurring and other revenue growth of ~9% YoY.

- Interest on funds held for clients of ~$0.110B.

- Adjusted EBITDA of $0.820B – $0.840B, representing a margin of ~41% at the midpoint.

Risk Assessment

At the end of Q3 2025, PAYC had ~$0.375B in cash and cash equivalents. Current liabilities before client funds obligation (excluding deferred revenue of ~$29.9 million) was ~$0.2287B thereby leaving cash and cash equivalents ~$0.1463B more than all current liabilities.

PAYC has no long-term debt other than operating leases.

Dividends and Share Repurchases

Dividend and Dividend Yield

PAYC has a brief dividend history having distributed its first quarterly dividend on June 12, 2023.

On November 3, 2025, PAYC issued a press release regarding the declaration of a $0.375/share regular quarterly cash dividend. It will be paid on December 8, 2025, to stockholders of record as of the close of business on November 24, 2025.

Share Repurchases

As a retail investor with a finite amount of capital to deploy, I rely heavily on a company’s ability to efficiently allocate capital. While many investors may not appreciate share prices that come under pressure, I want share price weakness and valuation improvements on the condition that a company’s financial performance and outlook remain strong.

In the case of PAYC, share price weakness presents an opportunity for the company to aggressively repurchase shares at attractive valuations. On the Q3 2025 earnings call, management states:

We still have ~$1.1B remaining under our buyback authorization as of October 31, 2025, and the revolving credit facility of $1B available for us to execute on.

In the Q3 2025 Form 10-Q we see the following:

In August 2022, our Board of Directors authorized a stock repurchase plan allowing for the repurchase of up to $1.1B of shares of our common stock in open market transactions at prevailing market prices, in privately negotiated transactions or by other means in accordance with federal securities laws, including Rule 10b5-1 programs. The stock repurchase plan was set to expire on August 15, 2024. In July 2024, our Board of Directors increased and extended the stock repurchase plan, such that $1.5B is available for repurchases through August 15, 2026. As of September 30, 2025, there was $1.22B available for repurchases under our stock repurchase plan.

During the nine months ended September 30, 2025, we repurchased an aggregate of 1,176,494 shares of our common stock at an average cost of $222.05 per share, including 172,642 shares withheld to satisfy tax withholding obligations for certain employees upon the vesting of equity incentive awards. Our payment of the taxes on behalf of those employees resulted in an aggregate cash expenditure of $42.4 million and, as such, we generally subtract the amounts attributable to such withheld shares from the aggregate amount available for future purchases under our stock repurchase plan. In October 2025, we repurchased an additional 501,094 shares of our common stock at an average cost of $199.86 per share, including 659 shares withheld to satisfy tax withholding obligations for certain employees upon the vesting of equity incentive awards.

PAYC could enter into an accelerated share repurchase agreement (ASR) if the Board deems this to be an appropriate means by which to enhance shareholder value. The use of an ASR would allow it to efficiently repurchase shares, locking in cash deployment upfront while shifting market risk of share price fluctuations to the investment bank. They are often used when companies believe their stock is undervalued or want to consolidate ownership quickly. This strategy ultimately helps enhance shareholder value and supports strategic corporate actions.

Using an ASR, PAYC would quickly repurchase a large block of its outstanding shares through an investment bank. It would pay the bank upfront, and the bank would deliver most of the shares immediately by borrowing them, typically from institutional investors like mutual funds or pension funds. The bank would then gradually purchase shares from the open market to return the borrowed shares over an agreed period.

The purpose of an ASR is to reduce the number of shares outstanding faster than through traditional buybacks; this often boosts EPS and potentially strengthens a company’s share price.

This type of transaction is governed by a legally binding agreement between the company and the investment bank, outlining the repurchase amount, timeframe, price adjustment mechanisms based on volume-weighted average price (VWAP), and other terms.

Valuation

NOTE: I have no idea to what extent PAYC is likely to repurchase additional shares over the remainder of FY2025. As such, my valuation estimates exclude any possible MAJOR share repurchases.

On November 6, 2025, PAYC’s share price closed @ ~$164 and I acquired shares @ $162.1148.

In the first 3 quarters of FY2025, GAAP EPS was $6.02. The company’s 4th quarter is generally the strongest. Erring on the side of caution, however, my assumption is that it will only generate $2.00 of GAAP EPS in Q4. My FY2025 GAAP EPS assumption is, therefore, $8.02.

Using my November 6 $162.1148/share purchase price, the forward diluted PE is ~20.2.

Broker adjusted diluted EPS estimates are likely to change over the coming days. For now, however, using my purchase price and the current forward-adjusted diluted EPS broker estimates, the forward adjusted diluted PE levels are:

- FY2025 – 19 brokers – ~17.5 using the mean of $9.27 and low/high of $9.13 – $9.70.

- FY2026 – 19 brokers – ~16.1 using the mean of $10.08 and low/high of $9.30 – $10.70.

- FY2027 – 12 brokers – ~14.3 using the mean of $11.31 and low/high of $10.10 – $12.37.

YTD2025, PAYC’s FCF is $0.2855B and $0.1937B. If it can generate a similar amount in Q4 2025 as the average of the prior 3 quarters, the FY2025 FCF should be ~$0.3807B (~$0.2855B + (33.33% of $0.2855B) and ~0.2583B (conventional and modified calculation methods where if deduct SBC to determine the modified FCF).

The company has disclosed the repurchase of additional shares subsequent to the end of Q3 2025 AND FY2025 CAPEX spend is now largely complete. With further weakness in the share price, I anticipate PAYC is still aggressively repurchasing shares.

PAYC may reduce the FY2025 diluted weighted average number of outstanding shares from 56.4 million. For now, however, I prefer to err on the side of caution and estimate the weighted average diluted shares outstanding for the year will be ~56.4 million.

YTD FCF is ~$0.2855B and ~$0.1937B (see table in the Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX section of this post). If it can increase FCF to ~$0.38B and ~$0.259B and we divide these figures by ~56.4 million, we get FCF/share of ~$6.74 and ~$4.60. Using my $162.1148/share purchase price, the forward P/FCF is ~24.05 and ~35.2.

As noted earlier, my FY2025 FCF estimate was completely off the mark. When I wrote my prior post, I saw no indication that PAYC would invest ~$0.1B in advanced AI hardware and equipment within its data centers. As a result, my prior FCF valuation estimates are to be ‘thrown out the window’.

My PAYC valuation calculations in my prior post were as follows.

Following the release of Q1 2025 earnings, PAYC’s share price has surged and is ~$246.60 as I compose this post on May 8. Broker estimates are currently under revision with several estimates already having been raised considerably. The current forward-adjusted diluted EPS broker estimates and forward adjusted diluted PE levels are:

- FY2025 – 18 brokers – ~27.9 using the mean of $8.85 and low/high of $8.51 – $9.16.

- FY2026 – 17 brokers – ~25 using the mean of $9.88 and low/high of $9.34 – $10.62.

- FY2027 – 6 brokers – ~22.2 using the mean of $11.12 and low/high of $10.80 – $11.45.

In Q1 alone, PAYC generated ~$144.8 million and ~$122.6 million of FCF calculated using the conventional and modified calculation methods. I estimate that PAYC will generate ~$550 million and ~$490 million of FCF in FY2025 using the conventional and modified calculation methods.

The diluted weighted average shares outstanding in Q1 was 56.3 million. I anticipate the diluted weighted average shares outstanding in FY2025 will be ~56.2 million.

My expectation is for PAYC to generate ~$9.80 and ~$8.72 of FCF/share in FY2025 using ~$550 million and ~$490 million of FCF for FY2025 using the conventional and modified calculation methods ($0.55B/56.2 million and $0.49B/56.2 million).

With shares currently trading at ~$246.60, my forward P/FCF estimates are ~25.2 and ~28.3.

Final Thoughts

I think the November 6 sell-off (a ~10.7% share price decline from the November 5 close) is overdone. I am, however, grateful for this pullback.

In my May 8, 2025 post I conclude that ‘What were once undervalued shares are now overvalued.’

Based on management’s current FY2025 outlook and broker estimates (~21.5 times FY2025 the mean forward adjusted diluted EPS broker estimate) I think shares are once again undervalued with a fair price being ~$200. Given this, I have increased my exposure by purchasing 100 shares on November 6, 2025 @ $162.1148.

The following are my prior most recent PAYC purchases:

- 100 shares on February 8, 2024 @ $192.8999

- 50 shares on February 9, 2024 @ $188.60

- 100 shares on March 4, 2024 @ $178.185

- 100 shares on May 2, 2024 @ $163.03

Following my November 6 purchase, my PAYC exposure is 800 shares in a ‘Core’ account within the FFJ Portfolio.

When I completed my 2025 Mid-Year Portfolio Review, PAYC was my 22nd largest holding. Using the November 6 ~$164 closing share price, PAYC may no longer be a top 30 holding.

Automatic Data Processing (ADP), Paychex (PAYX), and Paycom (PAYC) have all come under pressure of late. Now that shares in all 3 companies are attractively valued, I have recently increased my exposure in all three.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long PAYC.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.