I last reviewed Nasdaq (NDAQ) in this July 26, 2025 post at which time the most current financial information was for Q2 and YTD2025. With the release of Q3 2025 results on October 21, 2025, this is an opportune time to revisit this relatively small existing holding.

I last reviewed Nasdaq (NDAQ) in this July 26, 2025 post at which time the most current financial information was for Q2 and YTD2025. With the release of Q3 2025 results on October 21, 2025, this is an opportune time to revisit this relatively small existing holding.

Business Overview

The best way to learn about NDAQ is to review its website. Part 1 Items 1 (Business) and 1A (Risk Factors) in the FY2024 Form 10-K are also a great sources of information.

Financials

Q3 and YTD2025 Results

The information presented within NDAQ’s Q3 2025 Form 10-Q and earnings presentation is accessible on the company’s website.

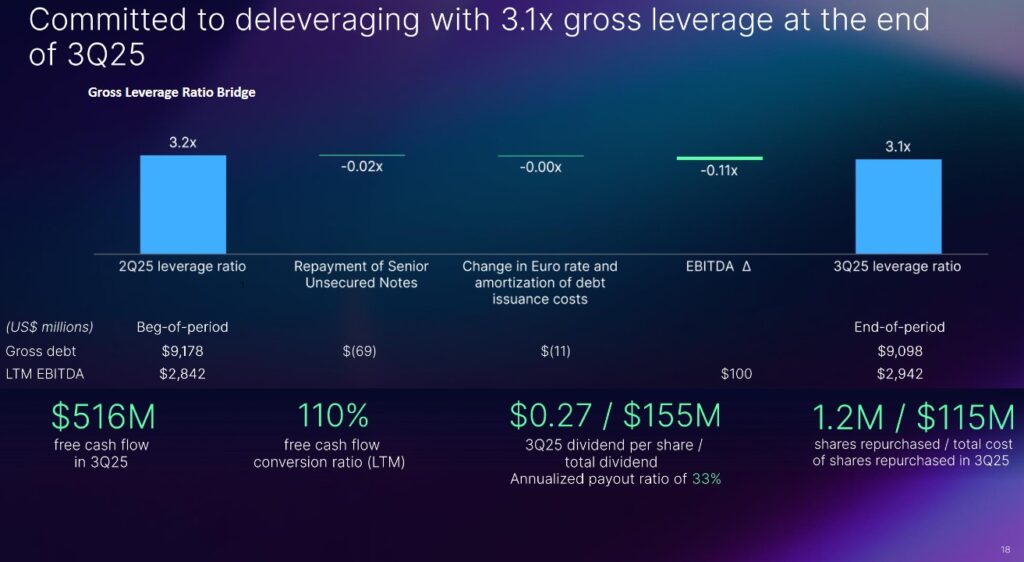

In its continued commitment toward deleveraging, NDAQ repurchased $69 million of debt and reached a gross leverage ratio of 3.1x at the end of Q3. This is an improvement of 0.1x from Q2.

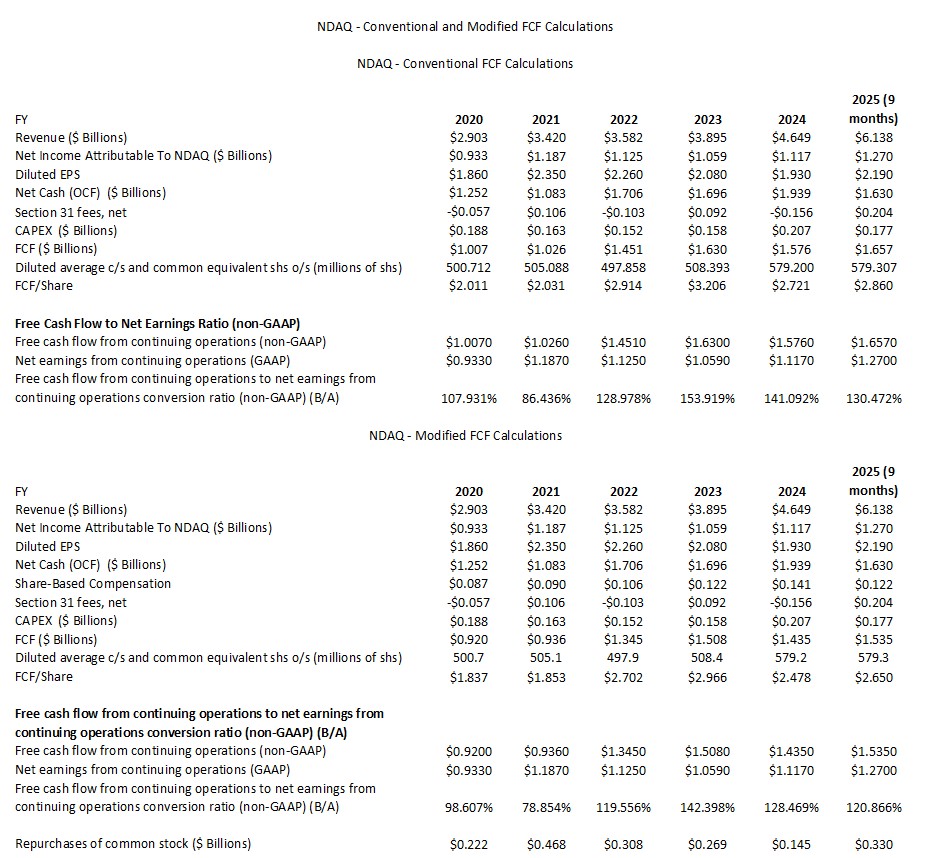

Conventional And Modified Free Cash Flow (FCF) Calculations (FY2019 – FY2024 and YTD2025 (9 months))

FCF is a non-GAAP measure, and therefore, the manner in which it is calculated is inconsistent. Many investors deduct CAPEX from OCF to arrive at FCF. In my How Stock Based Compensation Distorts Free Cash Flow post, I explain why I now also deduct stock based compensation (SBC) that is found in the Consolidated Statements of Cash Flows to determine FCF.

The variance in the FCF results NDAQ presents differs from online sources. This is because NDAQ makes a moderate adjustment to account for mandatory net Section 31 fees.

Net Section 31 fees are typically added back when determining FCF because FCF is intended to represent the cash generated by a company’s core operating performance, excluding fees and charges that are either non-operating or not reflective of the company’s ongoing cash-generating ability.

Section 31 fees are regulatory transaction fees imposed by the SEC on certain securities transactions to fund its oversight activities. These fees are operating outflows but are often considered non-core or pass-through items, not regular operating expenses managed by the business’s own cost structure.

NDAQ’s FCF calculations for FY2022 – YTD2025 (9 months) are found below.

I provide the following for the purpose of viewing FY2020 and FY2021 FCF levels.

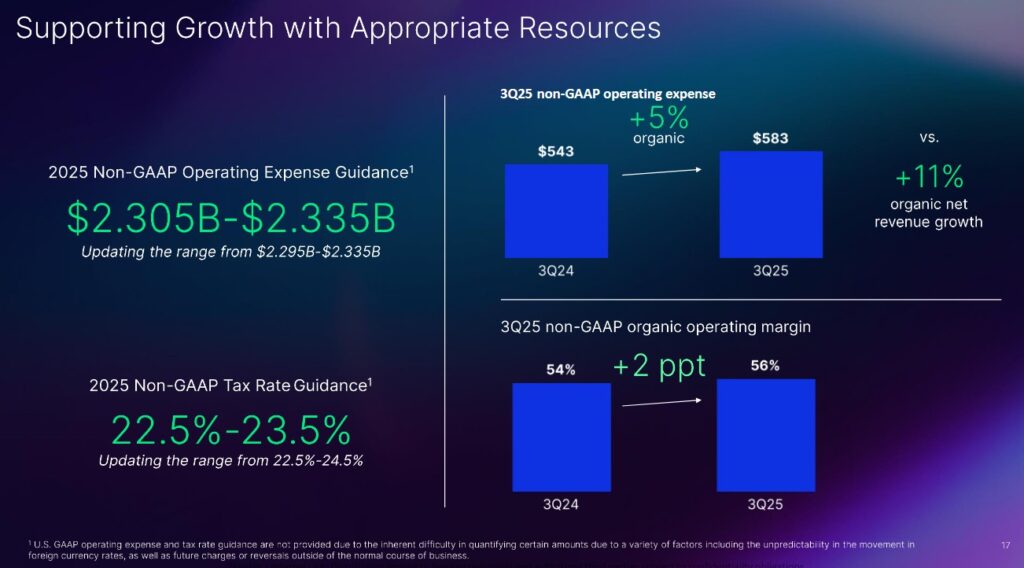

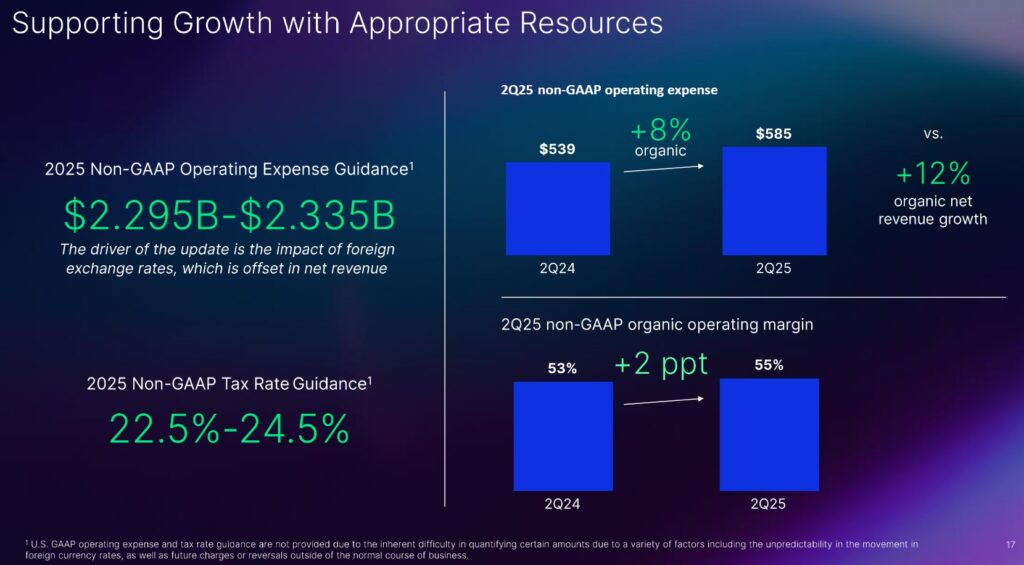

FY2025 Guidance

Organic expense expectations for the year are now expected to be ~$2.305B – ~$2.335B (previously $2.295B – $2.335B). This update reflects NDAQ’s:

- strong revenue growth throughout the year;

- continued investments in technology and people; and

- the recent sale of Solovis to Insight Partners.

By the end of Q3 2025, NDAQ surpassed its expanded net expense efficiency program target of $0.14B with over $0.15B in cost reduction actions.

The previous 2025 non-GAAP tax rate guidance of 22.5% – 24.5% is an appropriate expected tax range but NDAQ is lowering its FY2025 tax guidance to 22.5% – 23.5% due to some discrete items.

The following is NDAQ’s previous non-GAAP operating expense guidance and non-GAAP tax rate guidance.

Risk Assessment

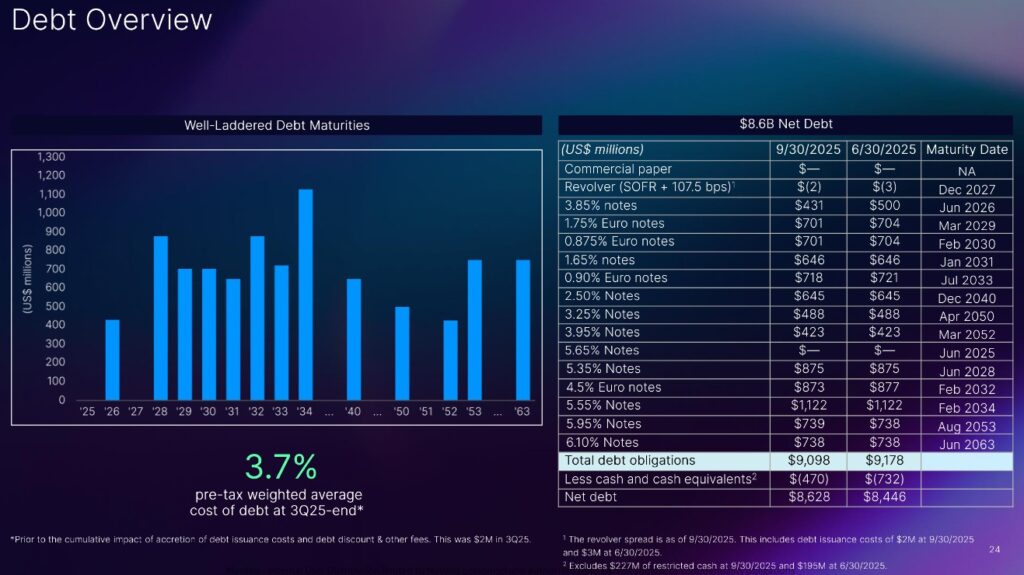

NDAQ provides debt information on its website.

Moody’s lowered NDAQ’s long-term issuer rating to Baa2 from Baa1 in June 2023 when NDAQ announced it had signed an agreement to acquire Adenza Group. On March 31, 2025, Moody’s upgraded NDAQ’s domestic unsecured long-term debt credit rating from Baa2 to Baa1.

In November 2021, S&P Global raised NDAQ’s domestic unsecured long-term debt credit rating from BBB to BBB+ but then lowered it to BBB on June 12, 2023 for the same reason as Moody’s. On August 12, 2025, S&P Global raised NDAQ’s local currency long-term rating to BBB+ with a stable outlook from BBB with a positive outlook.

Both ratings are the top tier of the lower medium grade investment grade category. The ratings define NDAQ as having adequate capacity to meet its financial commitments. However, adverse economic conditions or changing circumstances are more likely to lead to a weakened capacity of the obligor to meet its financial commitments.

NDAQ’s leverage is now 3.1x and it expects to reach 3.0x by FYE2025.

The next maturity date of one of NDAQ’s credit facilities is June 2026 at which time $0.5B is to be repaid. NDAQ now has greater flexibility in how it wants to deploy its capital.

The following reflects NDAQ’s leverage ratio at the end of Q1 and Q2 2025.

The following reflects NDAQ’s net debt position at the end of Q3 2025.

Dividends, Share Repurchases, and Stock Splits

Dividend and Dividend Yield

NDAQ’s dividend history is accessible here.

In Q3 2025, NDAQ distributed a $0.27/share dividend for a total of $0.155B, representing a 34% annualized payout ratio. This is slightly below NDAQ’s 35% – 38% payout ratio targeted for the next 3 or 4 years.

On October 21, NDAQ declared a regular quarterly dividend of $0.27/share on the its outstanding common stock. The dividend is payable on December 19, 2025 to shareholders of record at the close of business on December 5, 2025.

Some investors pay particularly close attention to dividend metrics. The focus, however, should be in total potential investment return.

Share Repurchases

In September 2023, NDAQ’s Board approved an increase in its share repurchase authorization to a total of $2B. At the end of Q2 2025, the remaining aggregate authorized amount under the existing share repurchase program was $1.5B. In Q3, NDAQ only repurchased ~1.2 million shares for $0.115B.

Debt reduction has been a priority following the Adenza acquisition. NDAQ, however, has continued its share repurchases to offset employee stock compensation.

Management previously communicated that after reaching the leverage target level, the vast majority of remaining FCF would be applied toward share buybacks. In addition, management has stated that it does not anticipate making any significant acquisition-related capital allocation decisions that would deter the company from sizable stock buybacks over the coming years.

Stock Splits

NDAQ initiated a 3 for 1 stock split in 2022.

Valuation

In my prior post I wrote:

NDAQ’s share price as I compose this post on July 25 is ~$95. Management does not provide earnings guidance, and therefore, I extrapolate YTD2025 results and use the current forward adjusted diluted EPS broker estimates to estimate NDAQ’s valuation. NDAQ’s forward adjusted diluted PE levels are:

- FY2025 – 18 brokers – mean of $3.32 and low/high of $3.18 – $3.41. Using the mean estimate, the forward-adjusted diluted PE is ~28.6.

- FY2026 – 18 brokers – mean of $3.70 and low/high of $3.45 – $3.86. Using the mean estimate, the forward-adjusted diluted PE is ~25.7.

- FY2027 – 13 brokers – mean of $4.14 and low/high of $3.81 – $4.38. Using the mean estimate, the forward-adjusted diluted PE is ~23.

In the first half of FY2025, NDAQ generated $1.969 and $1.829 of FCF calculated using the conventional and modified methods. If NDAQ can generate ~$4.00 and ~$3.70 for the year, the forward P/FCF using a ~$95 share price is ~23.75 and ~25.7.

NDAQ’s FCF conversion ratio has been greater than GAAP earnings in recent years and the variance between diluted earnings and adjusted diluted earnings is not that material. It is not surprising, therefore, that NDAQ’s valuation using FCF is somewhat superior to when EPS are used.

NDAQ’s valuation at the time of prior review has been lower than the current valuation. This is not surprising given the appreciation in NDAQ’s share price over the past 1.5 years far exceeds the appreciation in its underlying results.

Gauging a company’s valuation is heavily dependent on our assumptions. A significant component of NDAQ’s revenue and earnings is derived from its Market Services and Capital Access Platforms. The performance of these business segments is inherently volatile so trying to predict how NDAQ is likely to perform a few years into the future strikes me as being a crapshoot. I am, therefore, very reluctant to rely on earnings estimates beyond the current fiscal year.

Having said this, investor interest in equity investing remains robust and a greater degree of trading activity bodes well for NDAQ’s results!

NDAQ’s share price at the October 23, 2025 market close is ~$88.82. Using the current forward adjusted diluted EPS broker estimates, NDAQ’s forward adjusted diluted PE levels are:

- FY2025 – 19 brokers – mean of $3.41 and low/high of $3.26 – $3.47. Using the mean estimate, the forward-adjusted diluted PE is ~26.

- FY2026 – 19 brokers – mean of $3.78 and low/high of $3.60 – $3.95. Using the mean estimate, the forward-adjusted diluted PE is ~23.5.

- FY2027 – 14 brokers – mean of $4.22 and low/high of $4.04 – $4.45. Using the mean estimate, the forward-adjusted diluted PE is ~21.

In the first 3 quarters of FY2025, NDAQ generated $2.86 and $2.65 of FCF calculated using the conventional and modified methods. If NDAQ can generate ~$3.90 and ~$3.50 for the year, the forward P/FCF using a ~$88.82 share price is ~22.8 and ~25.4. These levels are slightly superior to those at the time of my prior review.

NDAQ’s FCF conversion ratio has been greater than GAAP earnings in recent years and the variance between diluted earnings and adjusted diluted earnings is not that material. It is not surprising, therefore, that NDAQ’s valuation using FCF is somewhat superior to when EPS are used.

Final Thoughts

In my June 13, 2023 post, I disclose initiating a 500 share position in a ‘Core’ account in the FFJ Portfolio @ ~$51/share on June 12, 2023. I acquired another 100 shares at ~$50.75 on July 19 and disclose this purchase in this July 20, 2023 post. With the automatic reinvestment of dividend income, I now hold 613 shares. My NDAQ exposure is relatively small and is not remotely close to being a top 30 holding.

My Final Thoughts reflected in a prior post remain the same.

When I initiated my NDAQ position, I noted that the success of the Nasdaq 100 index made NDAQ sensitive to the volatile technology sector thus leading to volatile quarterly results. To reduce this volatility, NDAQ undertook a strategic review which led to the beefing up of its anti-financial-crimes business (now known as regulatory technologies).

Sensing that NDAQ’s strategic direction would lead to more stable results (higher annual recurring revenue (ARR)), I envisioned an increase in NDAQ’s earnings multiple once NDAQ achieved its deleveraging objectives.

The benefits from the Adenza acquisition, however, will not happen overnight. NDAQ has higher interest costs resulting from the issuance of additional debt to assist in the financing of the acquisition. Its earnings are also spread over a larger number of shares; Thoma Bravo likely negotiated the receipt of NDAQ shares as partial compensation for the Adenza sale with the expectation that NDAQ’s future value would be much higher.

In the short-term, investors should expect muted results from NDAQ. Once it reduces its Gross Debt / Non-GAAP EBITDA to target levels and the Adenza business is demonstrating steady growth, I expect NDAQ’s financial picture will permit it to aggressively resume share repurchases. This should contribute to stronger future EPS results.

Although I am receptive to increasing my NDAQ exposure, I can not justify doing so at the current valuation. I want NDAQ’s share price to retrace to at least the low $80s before I consider increasing my exposure.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long NDAQ.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.