Intuitive Surgical (ISRG) is redefining the future of surgery with innovation. Its da Vinci platform ranks as being one of the most disruptive technologies in medtech history thus leading to the company’s remarkable success in rewarding long-term shareholders.

I last reviewed ISRG in this January 25, 2025 post at which time shares were trading at ~$584; I concluded ISRG’s valuation did not warrant the purchase of additional shares.

In various prior ISRG posts, I caution that its share price is volatile; the 52 week range as I compose this post on June 10, 2025 is $413.82 – $616.00. As luck would have it, ISRG’s share price fell to the mid $400s in early April. I, therefore, acquired additional shares for a young investor I am helping on their journey to financial freedom and disclose the purchase in my FFJ Portfolio – April 2025 post.

I now disclose my June 9 purchase of an additional 50 shares @ $519.22 thus increasing my average cost from $279.49 to $303.48. My exposure, excluding shares held by the young investor, now stands at 500 shares in one of the ‘Core’ accounts within the FFJ Portfolio.

Business Overview

Please review the company’s website and FY2024 Form 10-K if you are unfamiliar with the company.

The Q1 2025 Form 10-Q also contains a wealth of information.

Research and Development

ISRG’s success has not gone unnoticed thus attracting an increase in competition. The company, however, is continually improving upon its technology (the cumulative research and development (R&D) amounts to $3.023B in FY2022 – FY2024 and another $0.316B in Q1 2205). This heavy R&D investment is an indication that ISRG is not resting on its laurels.

ISRG continues to expand its manufacturing operations and supply chain capabilities to support the mid-2025 broad launch of da Vinci 5. In the broad launch, ISRG will incorporate the latest fully integrated hardware and software.

As robotic-assisted surgery advances, integrating force feedback into retained practice could enhance precision and improved recovery across disciplines. This technology is a breakthrough feature in the da Vinci 5 robotic surgical system. It allows surgeons to feel the push and pull forces exerted on tissue during surgery, enhancing precision and control.

The force feedback instruments are currently in limited supply but the company expects broad availability at the end of 2025.

Information about this technology is accessible on the company’s website.

Expansion

In Q1 2025, ISRG opened 2 new facilities at its Sunnyvale, California headquarters that significantly expand its US manufacturing and R&D footprint. A new 912,000 square foot facility will contain da Vinci systems manufacturing and R&D teams. A second 315,000 square foot facility will contain its Ion manufacturing and R&D team. Along with its recently opened factory in Pestre Corners, Georgia that manufactures X and Xi Systems, these new facilities provide space for ISRG to grow over the midterm.

Over the remainder of FY2025, ISRG continues to expect to open new manufacturing facilities in Germany and Bulgaria and to expand instrument manufacturing capacity in Mexico.

These new manufacturing facilities give ISRG supply availability, quality and cost advantages from scale and factory automation.

In determining whether to invest in ISRG, investors should consider that ISRG has self-funded all its CAPEX and R&D.

Given ISRG’s growth plans, it is not surprising to see a 12% pro forma operating expense increase relative to Q1 2024; the increase is because of a higher headcount, higher facilities-related costs, and higher legal fees. Headcount, for example, increased by just over 500 employees of which ~50% were in manufacturing roles to support revenue growth.

Tariff Impact

Tariff costs are capitalized into inventory and are then recognized within cost of sales as products are sold. ISRG expects the tariff impact to increase each quarter over the remainder of FY2025. Given this, ISRG has updated its pro forma gross margin estimate to 65% – 66.5% of revenue versus 67.4%, 66.4%, and 67.5% in FY2022 – FY2024.

This revised gross profit margin range does not reflect any potential additional tariffs or any potential inflationary impact on labor cost or the cost of procured components. To the extent that tariffs have a durable impact on sales and/or demand for its products, ISRG states that it will consider the implementation of a range of mitigating operational actions over time. For now, however, ISRG does not expect any such mitigating operational actions to have a significant beneficial impact in FY2025.

On the Q1 earnings call, management states that given the trade environment, financial pressures faced by hospitals, and macro risks, many global customers and prospects are likely to reprioritize capital budgets and/or extend time lines to invest in robotic programs.

In 2024, ISRG manufactured 98% of its robotic systems in the United States, 70% of its endoscopes in Europe, and ~80% of instruments and accessories in Mexico.

It sources raw materials and other components that go into its finished products from suppliers globally. The net result of the company’s manufacturing footprint and global customer demand is that ISRG is a significant US manufacturer and is a significant net US exporter.

In order of magnitude, ISRG characterize tariffs into 3 buckets.

Bucket #1

The tariffs relating to imports into China: Chinese tariffs of 125%.

The import of components from Chinese-based suppliers into the US: US tariffs of 145%.

Bucket #2

Imports into the US of procured components from US-based suppliers and imports of endoscopes from ISRG factories in Europe: 10% baseline tariffs with an increase in tariff rates after the current 90-day pause period elapses.

Bucket #3

Most of ISRG’s products manufactured in Mexico are certified under the requirements of USMCA. They are not, therefore, subject to current U.S. input tariffs. A small portion, however, does not currently meet the requirements and thus incur a 25% tariff upon import to the US.

Assuming the current and proposed tariff arrangements remain in place, ISRG now expects the impact to its FY2025 Income Statement to be additional cost of ~1.7% of revenue, plus or minus 30 bps.

Naturally, the impact of tariffs will vary with the:

- volume of capital sales in China;

- mix of procured components from outside the US suppliers; and

- proportion of products manufactured in Mexico that are certified under the US-Mexico-Canada agreement.

Financials

Q1 2025 Results

ISRG’s Q1 2025 results are reflected in the April 22 Form 8-K and Q1 2025 Form 10-Q which are accessible through the SEC Filings section of ISRG’s website.

With less than 3 weeks before the end of of ISRG’s second quarter, I dispense with reviewing Q1 results. Suffice it to say that ISRG’s financial position is very strong. Total cash, cash equivalents, and investments are in excess of ~$9.1B. Total liabilities on the other hand are ~$2.013B, of which ~$0.496B is deferred revenue (funds received in advance from customers).

Details about ISRG’s liquidity are found in the Form 10-Q but I provide the following table for ease of reference.

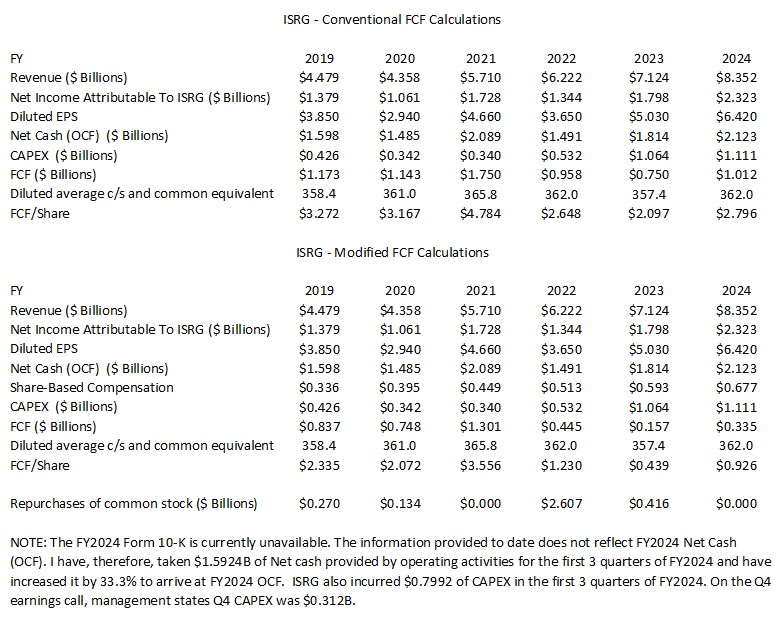

Conventional And Modified Free Cash Flow (FCF) Calculations (FY2019 – FY2024)

In my September 28, 2024 How Stock Based Compensation Distorts Free Cash Flow post, I touch upon how a company’s FCF can be distorted. In several subsequent posts, I take a conservative approach when looking at a company’s FCF.

FCF is a non-GAAP measure, and therefore, the manner in which it is computed is open to debate. Most companies subtract capital expenditures (CAPEX) from Net Cash Provided by Operating Activities found in the Consolidated Statement of Cash Flows. They do not, however, deduct share-based compensation (SBC). Given the magnitude of ISRG’s SBC, I think it is prudent to deduct it.

In Q1 2025, ISRG generated ~$0.5816B net cash from operations and the purchase of property, plant, and equipment amounted to ~$0.1166B giving us FCF of ~$0.465B when calculated under the conventional method. If we deduct ~$0.1852B of SBC, FCF drops to ~$0.2798B.

Significant CAPEX projects are now completed and are operational. This bodes well for an increase in ISRG’s FCF and FY2025 FCF calculated under the ‘modified’ method could very well exceed $1B (much higher than in FY2022 – FY2024).

FY2025 Outlook

On the Q4 2024 earnings call, management’s FY2025 procedures growth forecast was 13% – 16%. The forecast is now 15% – 17%.

The low end of the range assumes growth in China is impacted by trade, environmental and competitive dynamics.

Governments in key outside the US markets continue to constrain CAPEX budgets.

The high end of the range assumes China procedure growth improves relative to 2024, the CAPEX environment improves in key outside the US markets, and declines in bariatric procedures moderate. The high end of the range also assumes that procedures are not impacted by the current trade environment.

On the prior earnings call, the FY2025 pro forma gross profit margin forecast was 67% – 68% of revenue. This forecast reflected significant incremental depreciation as the company brings on new facilities, the impact of growth in newer products, and the impact of a stronger US dollar. With the impact of recently implemented and announced tariffs, ISRG’s cost of sales is expected to be negatively impacted by ~1.7% of revenue, plus or minus 30 bps. The pro forma gross margin forecast is now ~65% – 66.5% of revenue.

Management now expects pro forma operating expense growth of 10% – 14% which reflects increased depreciation from new facilities and investments to drive growth objectives.

The FY2025 non-cash stock compensation expense forecast is now $0.77B – $0.79B versus the prior forecast of ~$0.76B – ~$0.79B. In comparison, it was ~$0.513B, ~$0.593B, and $0.677B in FY2022 – FY2024 and ~$0.185B in Q1.

The FY2025 forecast for Other income, comprised mostly of interest income, remains at ~$0.37B – $0.4B.

The CAPEX estimate is now ~$0.65B – $0.75B which is primarily for planned facility construction activity. The prior estimate was ~$0.65B – ~$0.8B.

ISRG’s pro forma income tax rate was 21.4% in FY2024 and the estimate for 2025 remains at ~22% – ~23% of pretax income.

Risk Assessment

No rating agency rates ISRG because it has no debt.

Dividends

ISRG does not distribute a dividend.

Share Repurchases

In FY2019, there were 358.4 million outstanding diluted shares. By Q1 2025, this had increased to 364.6 million. During this period, the aggregate share based compensation reflected on the consolidated statements of cash flows amounts to ~$3.15B. Without share repurchases of ~$3.43B in FY2019 – Q1 2025, the number of outstanding diluted shares would be well above the current level.

One means by way a company can allocate its capital is to repurchase shares. This works wonders when shares are undervalued; ISRG repurchased ~$2.61B in FY2022 and ~$0.416B in FY2023. Fortunately, ISRG repurchased no shares in FY2024 and in Q1 2025 when shares were grossly overvalued.

Although I am not in favor of an increase in outstanding shares, ISRG is wise to have reinvested in the business and to have limited share repurchases when shares were significantly overvalued.

As of March 31, 2025, the remaining amount of share repurchases authorized by ISRG’s Board under the Repurchase Program was ~$1.1B. It will be interesting to see if ISRG repurchased shares in Q2!

Valuation

ISRG’s valuation is rich from earnings and cash flow perspectives.

As a growing business (Total Revenue of ~$2.385B in FY2015 versus ~$8.352B in FY2024 and ~$2.2534B in Q1 2025) with no reliance on debt to fuel this growth, it is not surprising many investors view ISRG is an attractive investment. ISRG’s valuation, therefore, is never at ‘bargain basement’ levels.

Trying to value ISRG using GAAP and non-GAAP earnings or conventional and modified FCF leads to valuation levels in the stratosphere. Investors, therefore, need to assess the probability of ISRG being able to grow into the lofty valuations.

At the time of my January 24 post, the forward-adjusted diluted PE estimates using the current ~$370 share price were:

- FY2024 – 26 brokers – ~59 based on a mean of $6.29 and low/high of $5.96 – $6.76.

- FY2025 – 21 brokers – ~50 based on a mean of $7.36 and low/high of $6.76 – $8.34.

- FY2026 – 14 brokers – ~43 based on a mean of $8.63 and low/high of $7.84 – $10.12.

When I wrote my April 20, 2024 post, ISRG shares traded at ~$366. Based on the estimates at the time of my post, the forward-adjusted diluted PE estimates were:

- FY2024 – 26 brokers – ~58.4 based on a mean of $6.27 and low/high of $5.96 – $6.58.

- FY2025 – 26 brokers – ~50 based on a mean of $7.34 and low/high of $6.87 – $7.76.

- FY2026 – 18 brokers – ~42.6 based on a mean of $8.60 and low/high of $7.85 – $9.29.

At the time of my July 23, 2024 post, the share price was ~$461. ISRG’s forward-adjusted diluted PE levels using the currently available information were:

- FY2024 – 26 brokers – ~70.3 based on a mean of $6.56 and low/high of $6.21 – $6.75.

- FY2025 – 27 brokers – ~60.7 based on a mean of $7.60 and low/high of $7.16 – $8.01.

- FY2026 – 21 brokers – ~52.0 based on a mean of $8.86 and low/high of $8.28 – $9.56.

Using the October 18, 2024 ~$521 closing share price and the current broker estimates, ISRG’s forward-adjusted diluted PE levels were:

- FY2024 – 26 brokers – ~76.4 based on a mean of $6.82 and low/high of $6.42 – $7.11.

- FY2025 – 27 brokers – ~66.9 based on a mean of $7.79 and low/high of $7.24 – $8.25.

- FY2026 – 23 brokers – ~57.3 based on a mean of $9.09 and low/high of $8.28 – $9.75.

Using ISRG’s January 24, 2025 closing share price of ~$584, ISRG’s forward-adjusted diluted PE levels were:

- FY2025 – 27 brokers – ~73.4 based on a mean of $7.96 and low/high of $7.69 – $8.45.

- FY2026 – 26 brokers – ~62.7 based on a mean of $9.32 and low/high of $8.05 – $10.00.

- FY2027 – 15 brokers – ~53.5 based on a mean of $10.91 and low/high of $10.01 – $11.68.

- FY2028 – 3 brokers – ~49 based on a mean of $11.93 and low/high of $11.39 – $12.80.

I have just acquired shares on June 9, 2025 at ~$519.22. Using the current broker adjusted diluted EPS estimates, ISRG’s forward-adjusted diluted PE levels are:

- FY2025 – 27 brokers – ~66.2 based on a mean of $7.84 and low/high of $7.59 – $8.23.

- FY2026 – 26 brokers – ~57.3 based on a mean of $9.06 and low/high of $8.49 – $9.80.

- FY2027 – 20 brokers – ~48.8 based on a mean of $10.63 and low/high of $9.46- $11.87.

- FY2028 – 7 brokers – ~43.1 based on a mean of $12.05 and low/high of $11.12 – $13.96.

Although I look at brokers’ earnings estimates, all estimates beyond the current fiscal year have no bearing on my investment decision making process. My reasoning for excluding estimates beyond the current fiscal year is that I have no idea how anybody, especially in the current environment, can determine how a company will perform over the next few years. The variance in the brokers’ earnings estimates clearly indicates there is no consensus on how ISRG is likely to perform going forward.

Final Thoughts

ISRG was our 7th largest holding when I completed my 2024 Year End Review. I anticipate ISRG will still be a top 10 holding when I perform my 2025 mid-year review.

Acquiring attractively valued shares is critical if we want to achieve decent total investment returns. A very high quality company such as ISRG, however, rarely has an attractive valuation. This does not mean that we should exclude them as potential investments. It means we must be confident a richly valued high quality company can ‘grow’ into its elevated valuation. A reasonable time frame in which to ‘grow’ into an elevated valuation might be under 5 years. Beyond this time frame and it might be prudent to be patient.

The only time ISRG’s valuation has been reasonable in recent years was in the second half of 2021 and late 2022. While I know my recent purchase @ ~$519.22 is perhaps ~$80 – ~$100 above fair value, I am reasonable certain ISRG will grow into its valuation within the next few years.

In my January 8, 2025 The Position Sizing Conundrum post, I touch upon making a meaningful investment when we have a high conviction in an attractively value high quality company. As noted at the outset of this post, I currently only own 500 ISRG shares. This is not sufficiently meaningful given my thoughts on the company’s long-term outlook. I, however, have a limited amount of ‘dry powder’. Depending on my liquidity and ISRG’s valuation in the future, I hope to gradually increase my ISRG exposure.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long ISRG.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation. I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.