When I last reviewed Intercontinental Exchange (ICE) in this August 3, 2024 post, I concluded that shares were no longer undervalued. At the time of that post, ICE had just released its Q2 and YTD2024 results on August 1, 2024.

When I last reviewed Intercontinental Exchange (ICE) in this August 3, 2024 post, I concluded that shares were no longer undervalued. At the time of that post, ICE had just released its Q2 and YTD2024 results on August 1, 2024.

I now revisit this existing holding given the release of Q3 and YTD2025 results on October 30, 2025.

Business Overview

Part 1 of ICE’s FY2024 Form 10-K has a comprehensive overview of the company and various risk factors.

ICE’s revenue used to be heavily reliant on volatile trading revenue. This made ICE’s quarterly results susceptible to wild variances. Through a series of acquisitions, ICE has diversified its business into new lines of business that generate more reliable annual recurring revenue (ARR). ICE, however, still receives a significant amount of its revenue from its largely transactional ‘Exchanges’ business segment.

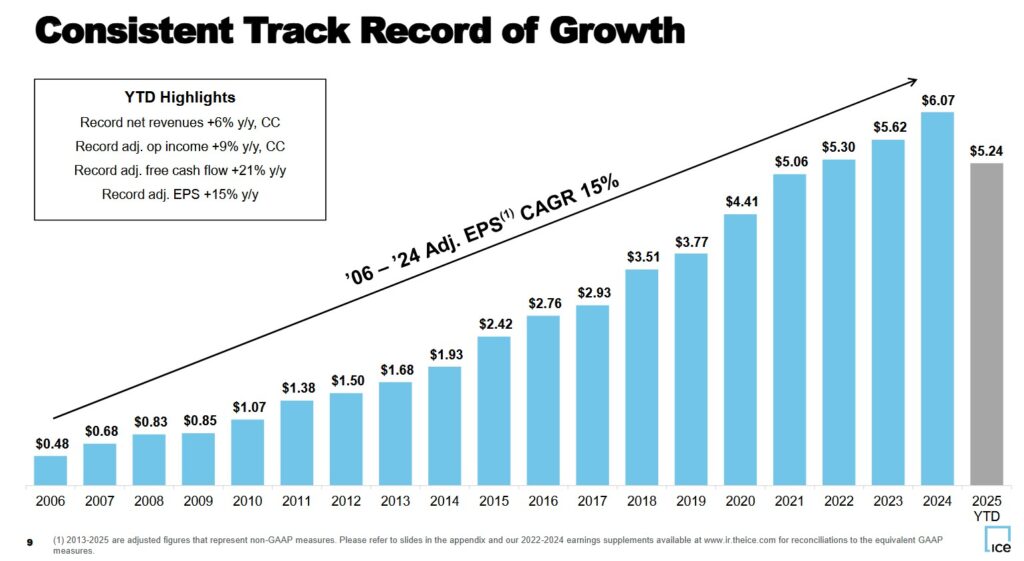

We see from the following graph that ICE has a consistent track record of growth.

Financial Review

Q3 and YTD2025 Results

Material related to ICE’s Q3 and YTD2025 earnings release is accessible here.

We need to be cognizant of the inherent volatility in ICE’s quarterly trading revenue. In FY2024 and the first 3 quarters of FY2025, trading volume has been elevated. Even if trading revenue ‘normalizes’, we should not interpret this as weakness in the Exchanges segment of its business.

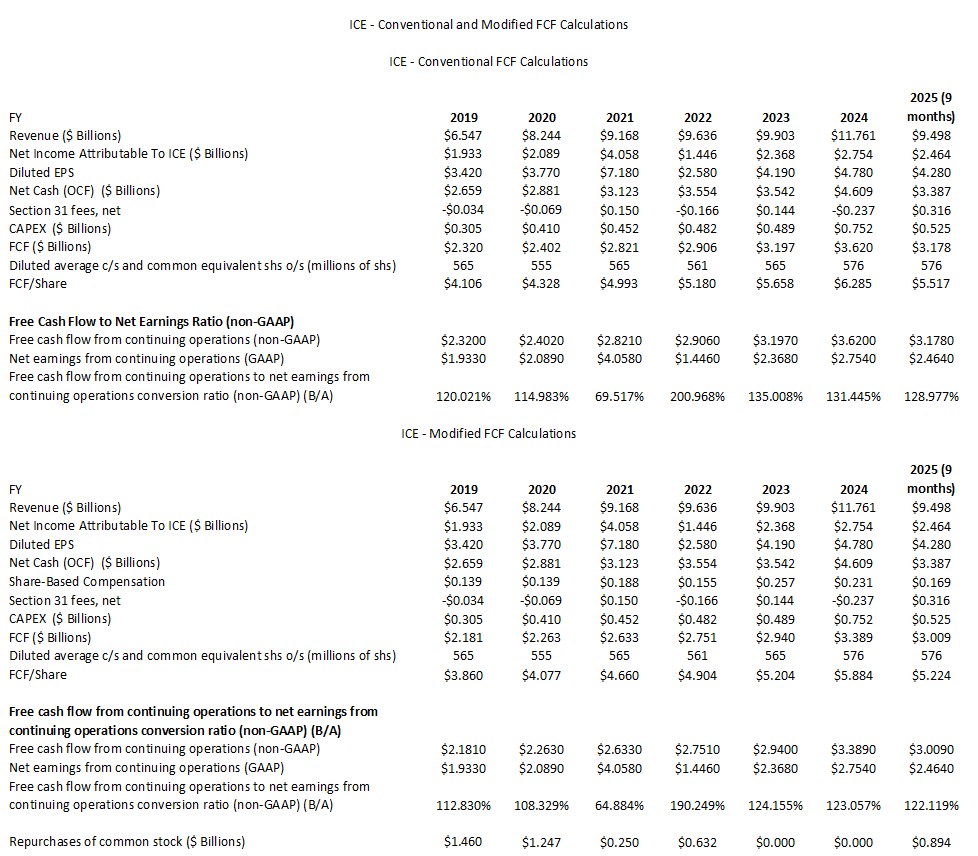

Conventional And Modified Free Cash Flow (FCF) Calculations (FY2019 – FY2025 (9 Months))

FCF is a non-GAAP measure, and therefore, its calculation is inconsistent. Many investors deduct CAPEX from OCF to arrive at FCF. In my How Stock Based Compensation Distorts Free Cash Flow post, I explain why I now also deduct stock based compensation (SBC) that is found in the Consolidated Statements of Cash Flows to determine FCF.

The conventional method only deducts CAPEX from OCF while the more conservative modified method also deducts SBC.

As with CME Group (see my October 25, 2025 post), we must deduct Section 31 fees. These fees are also known as SEC or transaction fees. They are small regulatory charges imposed on the sale of exchange-listed securities based on Section 31 of the Securities Exchange Act of 1934. The fee is 1% of one eight-hundredth of the dollar value of the equities sold.

When calculating free cash flow, these fees are deducted because:

-

They represent a real cash outflow directly tied to a company’s trading activities, such as when a brokerage or trading firm executes stock sales.

-

Self-regulatory organizations (SROs) technically pay these fees to the SEC. They are passed on to broker-dealers and ultimately to their customers or the company itself if it is executing trades as part of its operations.

-

Free cash flow aims to reflect all operating and transactional cash obligations that reduce available cash to equity holders, including recurring, transaction-specific outflows like Section 31 fees. Not deducting them would overstate a company’s true free cash flow, misrepresenting its financial capacity for dividends, reinvestment, or debt paydown.

The CAPEX figures below include capital expenditures and capitalized software development costs.

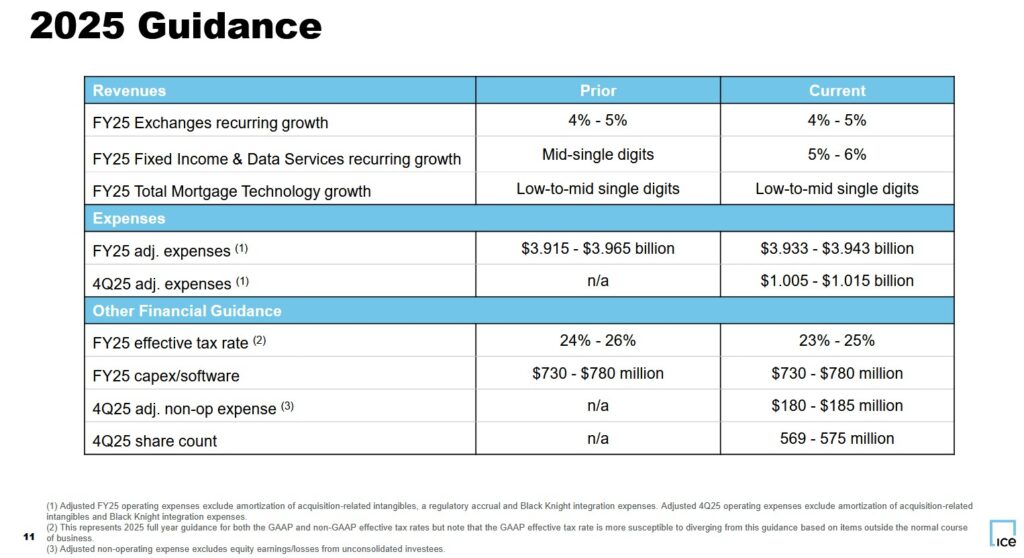

FY2025 Guidance

The following reflects ICE’s FY2025 guidance.

Risk Assessment

Adjusted leverage at the end of Q3 2025 is ~2.9x pro forma EBITDA. This is a reduction from 4.3x upon the completion of the Black Knight acquisition in Q3 2023, and 4.1x and 3.3x at FYE2023 and FYE2024.

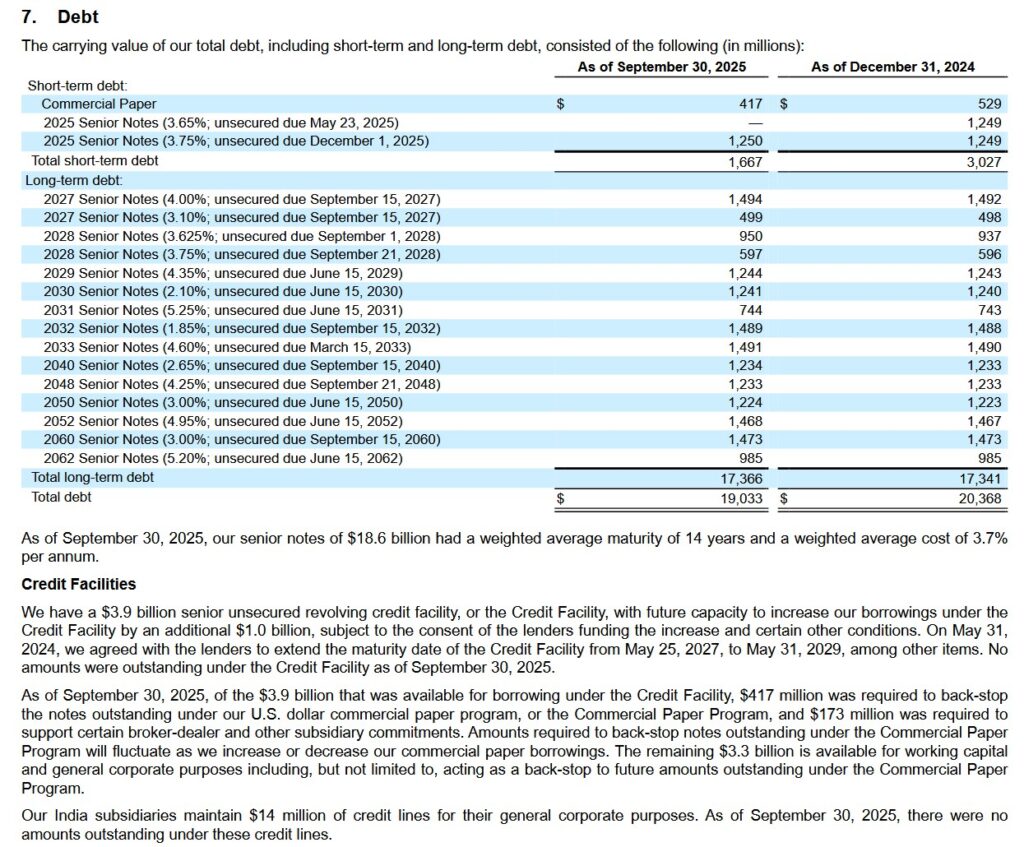

The following table reflects the fair value of ICE’s debt as of September 30, 2025 and December 31, 2024.

ICE’s current senior unsecured long-term debt credit ratings and outlook remain unchanged from my prior review.

- Moody’s: A3 (stable and affirmed on August 21, 2025)

- S&P Global: A- (stable and last reviewed on February 26, 2025)

Both ratings are at the bottom of the upper-medium grade investment-grade category. These ratings define ICE as having a strong capacity to meet its financial commitments. It is, however, somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

ICE’s ratings are acceptable for my purposes.

Dividend and Dividend Yield

ICE does not maintain a dividend history on its website. Its dividend history is accessible here.

On December 31, ICE will distribute its 4th consecutive $0.48/share quarterly dividend. In early February 2026, I expect ICE to declare a $0.03/share increase in the quarterly dividend.

As always, dividend metrics should have little bearing on our investment decisions. The focus should be on total potential shareholder return.

In December 2021, ICE’s Board approved an aggregate of $3.15B for future repurchases of common stock with no fixed expiration date that became effective on January 1, 2022.

In connection with the Black Knight acquisition, ICE terminated its Rule 10b5-1 trading plan and suspended share repurchases on May 4, 2022. ICE’s target was to reduce its adjusted leverage to 3.25X by 2025 and 3X as its normalized leverage level. Until such time as the 3.25x level was attained, ICE suspended share repurchases; it repurchased no shares in FY2023 and FY2024.

In December 2024, the remaining available balance of $2.52B was re-authorized by the Board.

During the 9 and 3 months ended September 30, 2025, ICE repurchased a total of 5.1 million and 2.2 million, respectively, shares of outstanding common stock at a cost of $0.894B and $0.398B, respectively,

As of September 30, 2025, the remaining balance of Board approved funds for future repurchases was $1.6B.

Valuation

On October 31, 2025, I acquired an additional 100 shares @ $145.245 in a ‘Core’ account in the FFJ Portfolio.

ICE does not provide adjusted diluted EPS guidance. Using my recent purchase price and current broker estimates the forward adjusted diluted PE levels are:

- FY2025 – 17 brokers – mean of $6.90 and low/high of $6.75 – $7.11. Using the mean estimate: ~21.05.

- FY2026 – 17 brokers – mean of $7.53 and low/high of $6.92 – $7.96. Using the mean estimate: ~19.3.

- FY2027 – 12 brokers – mean of $8.36 and low/high of $7.30 – $8.81. Using the mean estimate: ~17.4.

ICE has generated $5.517 and $5.224 of YTD2025 FCF/share. This is based on ~576 million diluted outstanding shares.

If ICE generates a comparable level of FCF in Q4 as in each of the first 3 quarters, we can expect another ~$1.84 and ~$1.74 thereby increasing the FY2025 FCF to ~$7.36 and ~$7 calculated on a conventional and modified basis. Divide my $145.245 purchase price by these FCF estimates and we get P/FCF of ~19.7 and ~20.8 (conventional and modified FCF calculation methods).

These FY2025 FCF estimates are ~107% (~$7.36/$6.90) and ~101% (~$7/$6.90) of the FY2025 mean adjusted diluted broker estimates. This appears reasonable considering FCF/share typically exceeds GAAP EPS by a wide margin.

With a wide variance in ICE’s FY2025 share count guidance (569 – 575 million), we could see better valuations than those calculated above. Much will depend on the extent to which ICE repurchases shares in Q4.

Final Thoughts

Now that ICE has attained a normalized leverage level, I anticipate it will start to deploy more capital toward share repurchases. I, therefore, want ICE’s shares to remain under pressure.

On October 31, 2025 I acquired an additional 100 shares in a ‘Core’ account in the FFJ Portfolio @ ~$145.245/share. I now hold 300 shares in a ‘Core’ account and 200 shares in a ‘Side’ account the FFJ Portfolio and more shares in a retirement account.

In my 2025 Mid-Year Portfolio Review, ICE was my 25th largest holding. At the time of that review, shares were trading at ~$183.45.

As noted at the outset of this post, through a series of acquisitions, ICE has diversified its revenue streams that now include mortgage technology and fixed-income data. ICE’s revenue used to be volatile but through a series of strategic acquisitions, ~50% of its revenue is now recurring.

ICE’s New York Stock Exchange is benefiting from a surge of retail interest in equity markets and higher option volume. Competition among equity exchanges and trading platforms, however, has driven net revenue per share lower.

The company’s equity trading is likely to continue to face stiff headwinds as new competitors encroach on the NYSE. In an effort to address this increasing competition, ICE is increasingly turning to data, listing, and connectivity fees to supplement its transaction fees at the NYSE. Nevertheless, ICE faces competition in this area as well. Fortunately, ICE’s futures business remains strong, with its energy complex growing at an accelerated rate; ICE benefits from pricing power and favorable energy market trends.

Following the acquisition of Black Knight in 2023, ICE is now the largest provider of mortgage technology in the US. By combining Ellie Mae with Black Knight (ICE acquired these 2 businesses for ~$22B), ICE now has a comprehensive mortgage data and service suite and a commanding position in the mortgage software market.

The digitization of mortgage workflow is in the early stages and while the acquisitions make strategic sense, the entire US mortgage industry is currently facing pressure from high mortgage rates and their impact on mortgage origination volume. In all likelihood, ICE’s mortgage technology segment will likely continue to face pressure until such time as rates fall and refinance volume recovers.

These headwinds are likely the reason why the share price has retraced from the ~$189.35 52 week high set in early August 2025.

I consider a fair value to be in the mid $160s. Should ICE’s share price increase to ~$165, this represents a ~13.6% capital appreciation. ICE’s dividend is irrelevant in my investment decision making process.

I wish you much success on your journey to financial freedom!

Note: Thanks for reading this article. Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long ICE.

Disclaimer: I do not know your circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decisions without conducting your research and due diligence. You should also consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.