In my June 27, 2025 Why I Added Accenture To The FFJ Portfolio post, I disclose a new Accenture (ACN) position. Following my initial purchase, I have increased my exposure in keeping with the Final Thoughts expressed in my prior post.

ACN is a new holding and my current exposure is only 200 shares. It will not, therefore, come close to being a top 30 holding when I complete my 2025 Mid-Year End Review in early July. I do, however, like the company’s long-term outlook and short-term headwinds do not concern me. If ACN’s valuation improves, I hope to be in a position to increase my exposure.

ACN’s share price is slightly lower than when I initiated a position. There is, however, no material change in the brokers’ adjusted diluted EPS estimates nor any material change in the company’s operations thus prompting me to acquire:

- 100 shares @ $281.5887 on July 11; and

- 200 shares @ $278.5323 on July 28

My exposure now stands at 500 shares in a ‘Core’ account in the the FFJ Portfolio.

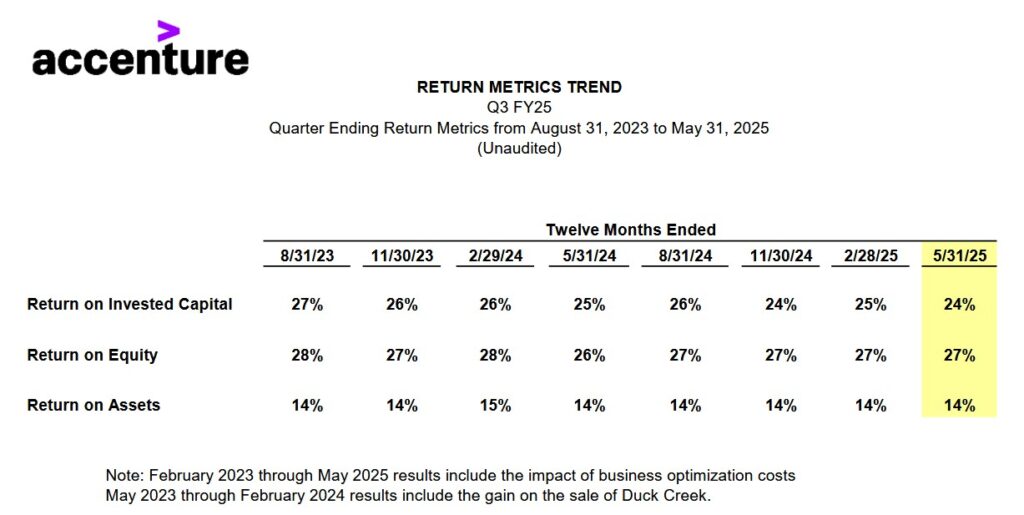

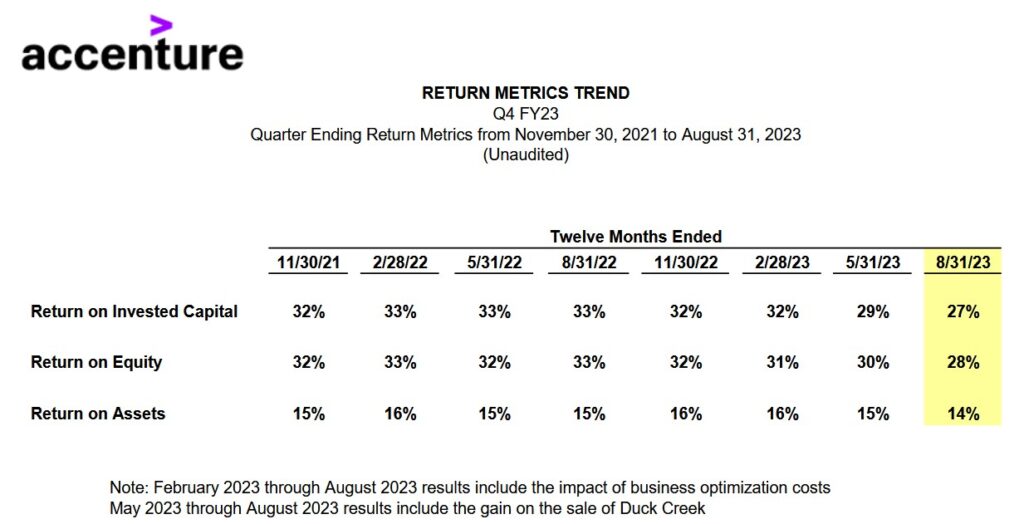

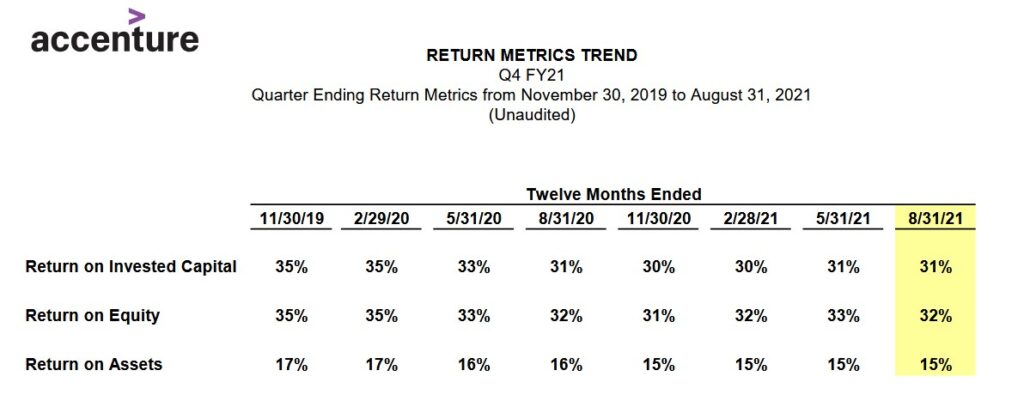

After giving this investment more consideration, I could not justify why I would not increase my exposure in a company with the following recent ROIC, ROE, and ROA track record. ACN provides these metrics quarterly in its supporting materials.

Final Thoughts

Management expects to return at least $8.3B through dividends and share repurchases in FY2025. In the first 3 quarters of FY2025 it has returned ~$6.924B. I don’t care much for dividend income on which I incur a tax liability. My interest lies in the magnitude in which ACN reduces its weighted average diluted outstanding shares (678.757 million in FY2015 to 630.457 million in Q3 2025).

The company consistently generates significant free cash flow (FCF). My expectation is that ACN’s weighted average diluted shares outstanding can conservatively be reduced by 2 – 4 million annually for the foreseeable future. Using a 3 million mid-point, it is feasible that ACN’s weighted average diluted shares outstanding could be ~600 million in another 10 years. I also anticipate that its earnings and FCF will be considerably higher in another 10 years. With shares currently trading close to fair value, it strikes me as foolish not to increase my exposure.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long ACN.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation. I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.