![]() I recently covered Cintas (CTAS) in this my September 24, 2025 post. The reason for revisiting CTAS so soon is to disclose that on November 3, 2025 I acquired an additional 100 shares @ ~$181.455 in a ‘Side’ account in the FFJ Portfolio. My total exposure is now 700 shares.

I recently covered Cintas (CTAS) in this my September 24, 2025 post. The reason for revisiting CTAS so soon is to disclose that on November 3, 2025 I acquired an additional 100 shares @ ~$181.455 in a ‘Side’ account in the FFJ Portfolio. My total exposure is now 700 shares.

On October 28, CTAS released news about:

- a quarterly cash dividend of $0.45/share of common stock payable on December 15, 2025 to shareholders of record at the close of business on November 14, 2025; and

- an additional share buyback program under which CTAS may repurchase up to $1.0B of CTAS at market prices. This program is in addition to a current program with $0.7B of CTAS common stock remaining.

If the Board deems CTAS’s valuation to be sufficiently attractive, the company could potentially enter into an accelerated share repurchase (ASR) arrangement. An ASR is a specialized stock buyback mechanism in which a company quickly repurchases a significant block of its own shares with the help of an investment bank. The company makes an upfront cash payment to the bank and enters into a forward contract, which allows the immediate retirement of shares and a rapid impact on metrics such as earnings per share (EPS).

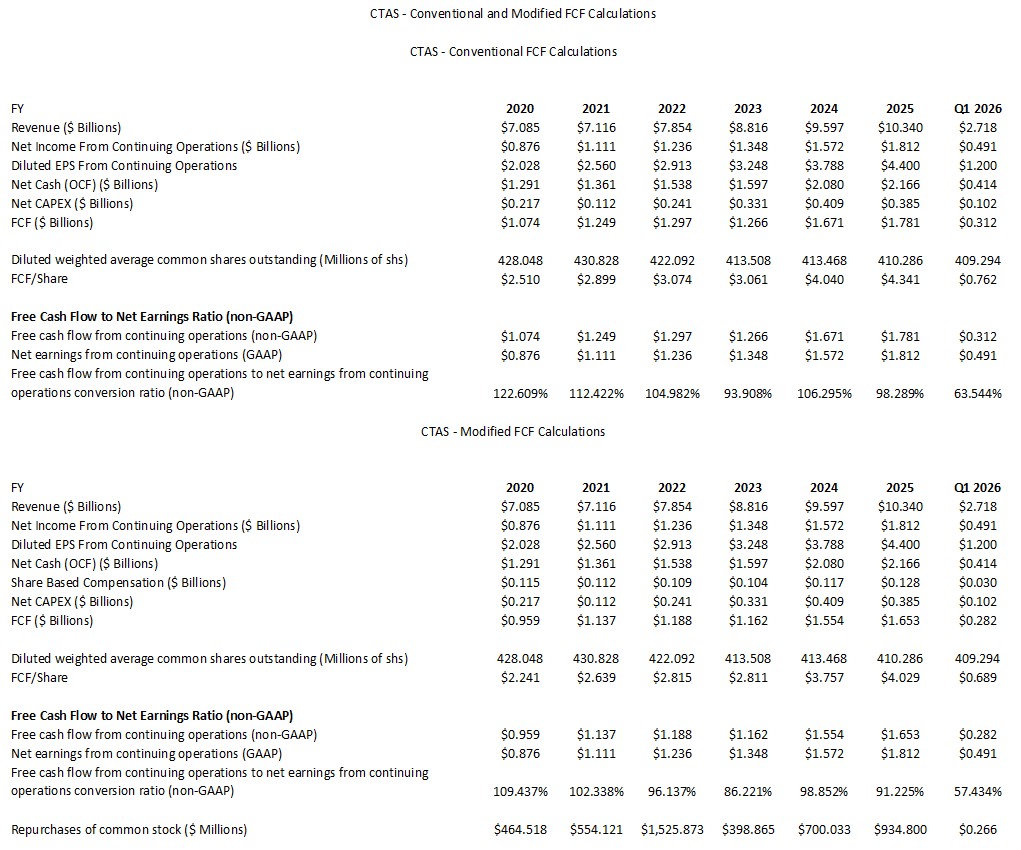

Conventional And Modified Free Cash Flow (FCF) Calculations (FY2020 – FY2025 and YTD2026)

In my prior post I provide the following table and provide it again for ease of reference.

NOTE: My valuation estimates could change significantly if CTAS enters into a meaningful ASR.

Valuation

Using my recent $181.455 purchase price and management’s current $4.74 – $4.86 adjusted diluted EPS outlook, the forward adjusted diluted PE is ~37.3 – ~38.3.

NOTE: CTAS’s diluted EPS and adjusted diluted EPS are likely to continue to be relatively similar.

Its valuation using the current broker guidance is:

- FY2026 – 19 brokers – mean of $4.84 and low/high of $4.78 – $4.90. Using the mean, the forward adjusted diluted PE is ~37.5.

- FY2027 – 19 brokers – mean of $5.36 and low/high of $5.15 – $5.55. Using the mean, the forward adjusted diluted PE is ~33.9.

- FY2028 – 10 brokers – mean of $5.92 and low/high of $5.53 – $6.20. Using the mean, the forward adjusted diluted PE is ~30.7.

I continue to estimate that the FY2026 FCF conversion ratio will be ~98% (calculated under the conventional method) and ~94% (calculated under the modified method). Using a $4.80 mid-point of management’s FY2026 guidance, CTAS’s FY2026 FCF is likely to be ~$4.70 (conventional) and ~$4.51 (modified). From these figures and my ~$181.455 purchase price, I estimate CTAS’s forward P/FCF is ~38.6 and ~40.2 (calculated using the conventional and modified FCF values).

This could significantly change depending upon the extent to which CTAS repurchases shares.

In my prior post I reflect the following:

Its valuation using the current broker guidance is:

- FY2026 – 20 brokers – mean of $4.85 and low/high of $4.76 – $4.92. Using the mean, the forward adjusted diluted PE is ~41.4.

- FY2027 – 19 brokers – mean of $5.35 and low/high of $5.13 – $5.51. Using the mean, the forward adjusted diluted PE is ~37.5.

- FY2028 – 10 brokers – mean of $5.89 and low/high of $5.51 – $6.19. Using the mean, the forward adjusted diluted PE is ~34.1.

Looking at the FCF/EPS metrics in prior years, I continue to estimate that the FY2026 FCF conversion ratio will be ~98% (calculated under the conventional method) and ~94% (calculated under the modified method). Using a $4.80 mid-point of management’s FY2026 guidance, CTAS’s FY2026 FCF is likely to be ~$4.70 (conventional) and ~$4.51 (modified). From these figures, we can estimate that CTAS’s P/FCF is ~42.7 and ~44.5 (calculated using the conventional and modified FCF values).

Final Thoughts

CTAS is the largest industry participant in a highly fragmented industry. It grows organically and through acquisitions; a major acquisition could quickly increase route density.

In FY2016 and FY2025, CTAS generated ~$4.8B and ~$10.34B of revenue. The current FY2026 revenue outlook is $11.06B – $11.18B. It seems realistic that CTAS could generate ~$14B of revenue by FY2035. If it can continue to generate ~15% – ~17% Net Income From Continuing Operations as a percentage of Revenue (16.4% and 17.5% in FY2024 and FY2025), it could generate ~$2.1B – ~$2.38B in FY2035.

CTAS was rebuffed AGAIN by one of its largest US competitors (Unifirst Corporation (UNF)) in early 2025. An acquisition could have added ~$2.4B to CTAS’s top line.

While UNF has not been receptive to CTAS’s overtures, Vestis (VSTS) (spun off from Aramark in October 2023) could be a potential acquisition target. It has generated ~$2B of revenue in the first 9 months of FY2025. Its financial results (EPS and FCF), however, are terrible and its balance sheet is bloated with non-investment grade debt. If CTAS were to acquire VSTS, it could possibly eliminate a sizable percentage of VSTS’s fixed costs and potentially quickly increase route density.

Alsco is another major competitor. It is, however, a privately held, fifth-generation, family-operated business that was founded in 1889. This competitor, in my opinion, might be less than receptive to selling to CTAS.

I wish you much success on your journey to financial freedom!

Disclosure: I am long CTAS.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.