![]()

When I reviewed Lockheed Martin (LMT) in this January 29, 2025 post, the most current financial information was for FY2024. On January 27, 2025, LMT’s shares closed at ~$503.70. Following the release of Q4 and FY2024 results and FY2025 outlook on January 28, 2025, the share price plunged ~$46. My conclusion was that LMT’s share price weakness was a buying opportunity. I, therefore, acquired an additional 50 shares @ $457.75 in one of the ‘Core’ accounts in the FFJ Portfolio on January 28 bringing my LMT exposure to 620 shares.

When I completed my 2025 Year-End Investment Holdings Review, I held 632 shares making it my 9th largest position. At the time of that review, LMT’s share price was $483.67.

With shares trading at ~$630 as I compose this post on January 30, LMT’s ranking has undoubtedly improved.

LMT’s share price experienced volatility in early January 2026 thus prompting me to publish my Lockheed Martin – The Importance Of Having A Long-Term Mindset post on January 8.

On January 29, 2026, LMT released its Q4 and FY2025 results and FY2026 outlook. This is, therefore, an opportune time to revisit this existing holding.

Business Overview

LMT is a global security and aerospace company that operates in 4 business segments: Aeronautics, Missiles and Fire Control (MFC), Rotary and Mission Systems (RMS) and Space. Its main areas of focus are in defense, space, intelligence, homeland security and information technology, including cybersecurity.

It is engaged in the research, design, development, manufacture, integration and sustainment of advanced technology systems, products and services.

Principal customers are agencies of the U.S. Government. It, however, also serves international customers with products and services that have defense, civil and commercial applications.

A good way to learn about a company is to review the company’s website and Part 1 Item 1 – Business and Item 1A – Risk Factors in the FY2025 Form 10-K that is accessible through the SEC Filings section of the company’s website.

Financials

Q4 and FY2025 Results

Refer to the material available in the Quarterly Results section of LMT’s website.

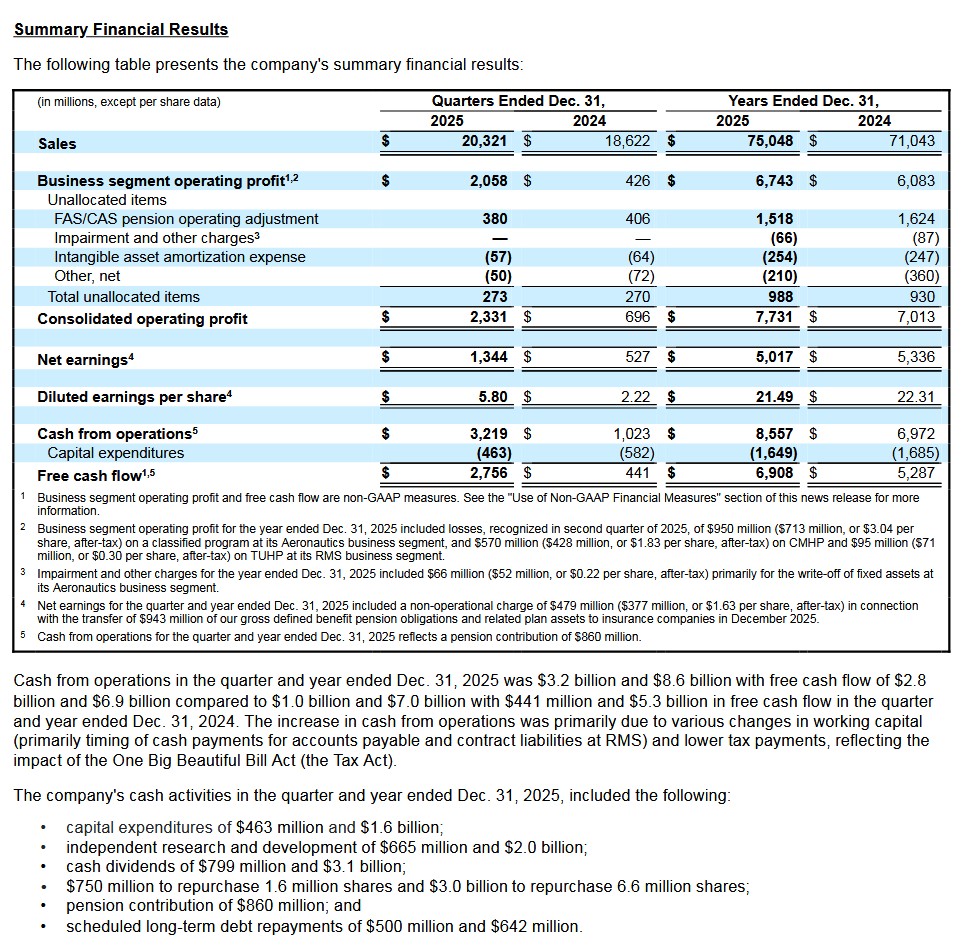

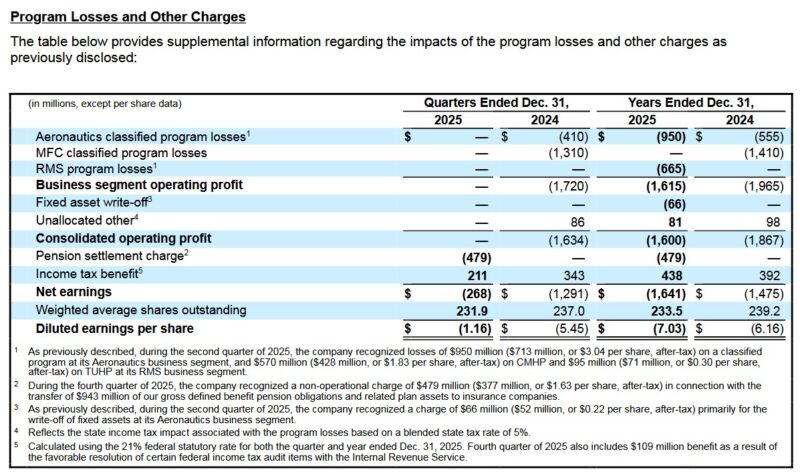

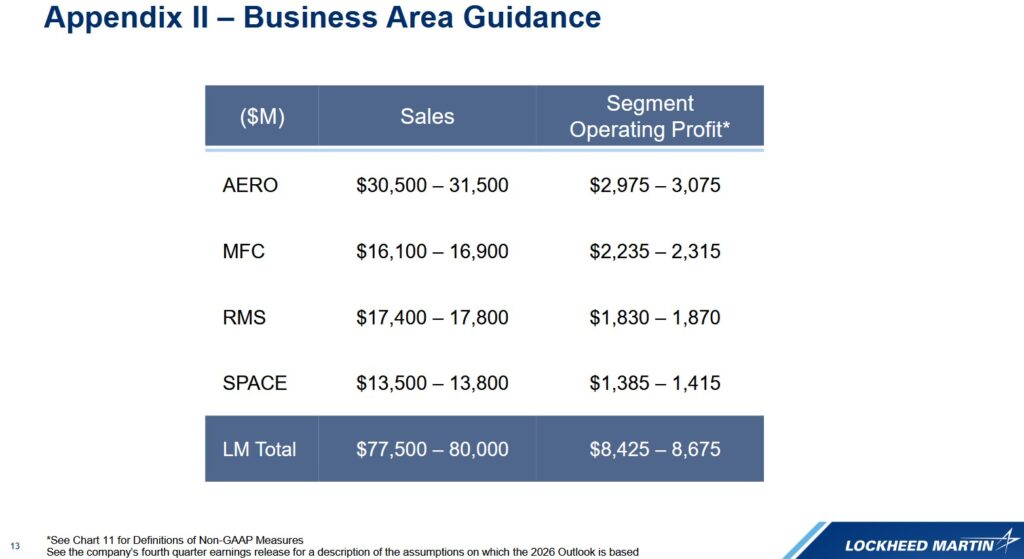

The following images reflect the highlights for LMT as a whole. The Q4 2025 Earnings Presentation, however, provides Sales and Operating Profit results for each of LMT’s 4 business segments.

Earnings Impacts of Classified Program Losses and Other Items

LMT’s recent program losses stem from a combination of ‘classified’ development hurdles, production delays on the F-35, and the inherent risks of fixed-price contracts.

The single largest contributor to recent losses involves several highly sensitive, classified development programs. These are often fixed-price incentive contracts, and therefore, LMT must absorb costs that exceed the agreed-upon ceiling.

Aeronautics Division: In 2024 and 2025, LMT recognized ~$1.5B in losses on a single classified aeronautics program (often associated with the ‘Skunk Works’ division). These were ‘reach-forward’ losses, meaning LMT updated its estimates to account for higher-than-expected engineering and integration costs needed to meet future milestones.

Skunk Works, officially known as Advanced Development Programs, is LMT’s legendary, top-secret innovation hub. It is famous for taking on ‘impossible’ missions under extreme deadlines and extreme secrecy. It is essentially the specialized laboratory where the ‘next big thing’ is invented.

Missiles and Fire Control (MFC): In Q4 2024, LMT took a ~$1.4B loss on a classified program within its missiles segment. This was driven by the realization that the US government would likely exercise all contract options, forcing LMT to complete work at costs significantly higher than the original contract price.

To avoid future program losses, LMT is executing a strategy that shifts away from high-risk contract types. It has pivoted to prioritize predictability over aggressive bidding, focusing on four main pillars:

1. Moving Away from High-Risk Contracts

The primary cause of LMT’s recent losses was ‘fixed-price’ development contracts where the company was responsible for all cost overruns. LMT is now increasing the use of long-term framework agreements that provide stable, multi-year production instead of year-to-year uncertainty.

For highly experimental R&D (like new Skunk Works projects), LMT is pushing for ‘cost-plus’ contracts where the US government covers the expenses of technical hurdles, rather than forcing LMT to gamble on a fixed price.

2. The “1LMX” Digital Transformation

LMT is currently in the middle of a massive internal overhaul called 1LMX which is a multi-year effort to replace dozens of siloed legacy systems. By integrating the supply chain, engineering, and finance into one AI-assisted system, LMT will be able to better identify cost spikes before they lead to a multi-billion dollar ‘reach-forward’ loss. It is also aligning all business segments to the same accounting and management practices to ensure transparency, specifically to avoid the ‘surprises’ that hit the Missiles and Fire Control (MFC) segment in 2024.

3. ‘Digital Twins’ and AI Engineering

To avoid the software delays that have plagued the F-35’s TR-3 upgrade, LMT is moving toward a ‘Model-Based Enterprise’.

Before a single piece of metal is cut, engineers build a ‘Digital Twin’ of the aircraft or missile enabling them to run millions of simulated tests to find design flaws that would normally only appear during expensive physical flight tests. In addition, on production lines for the F-35 and PAC-3, AI sensors now monitor every bolt and weld in real-time, drastically reducing the ‘rework’ costs that contribute to program losses.

4. Aggressive Focus on Munitions Ramping

Recognizing that complex aircraft programs are risky, LMT is shifting its growth focus toward high-volume munitions like the High Mobility Artillery Rocket System (HIMARS) launcher, PAC-3, and Terminal High Altitude Area Defense (THAAD).

These are ‘mature’ programs with lower technical risk. LMT is quadrupling production capacity for these items, which provides a buffer of reliable profit to offset the R&D risks undertaken by divisions such as Skunk Works.

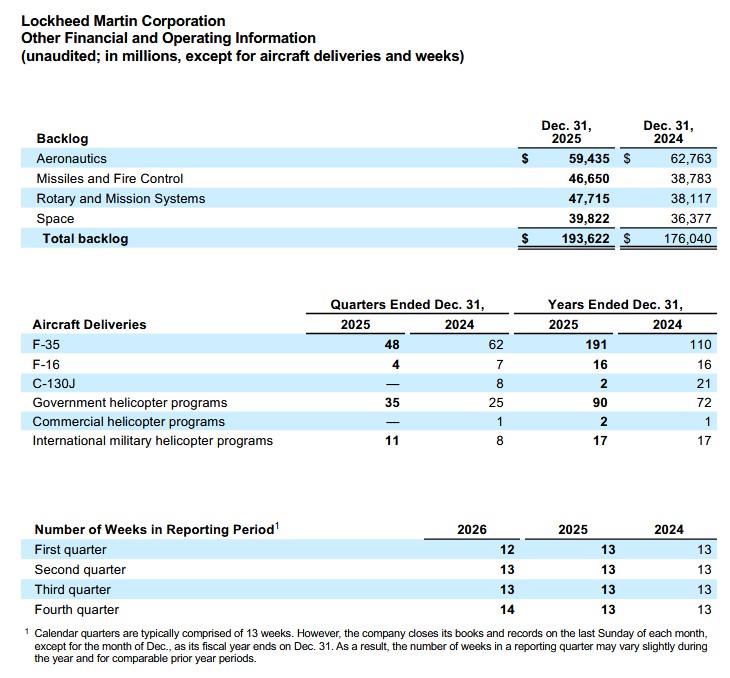

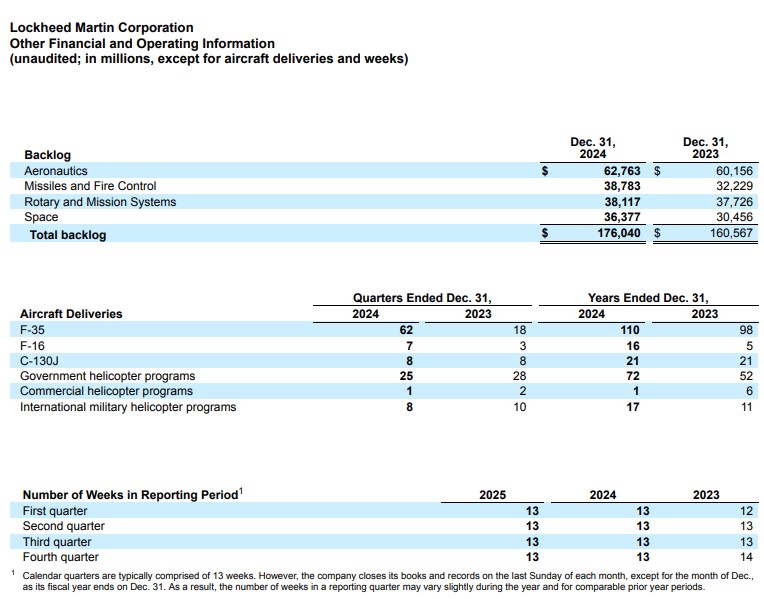

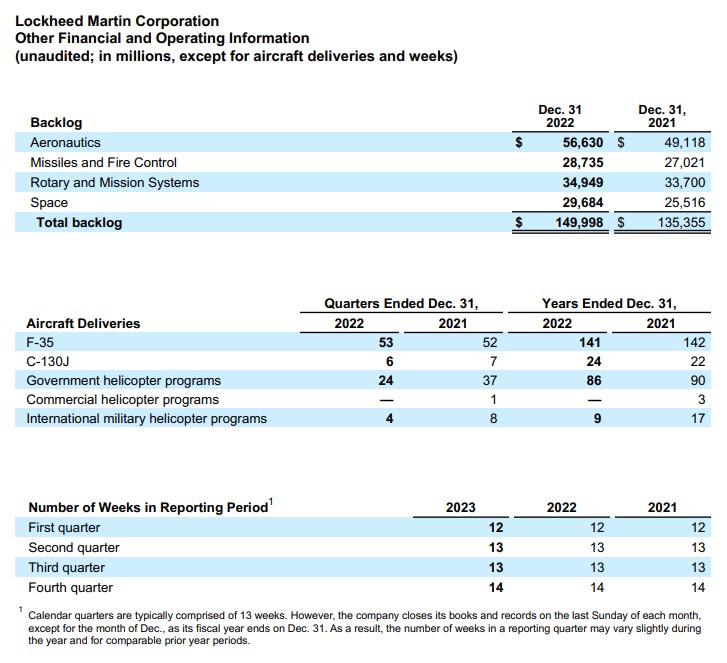

Order Backlog

The following reflect the deliveries and backlog for FY2021 – FY2025.

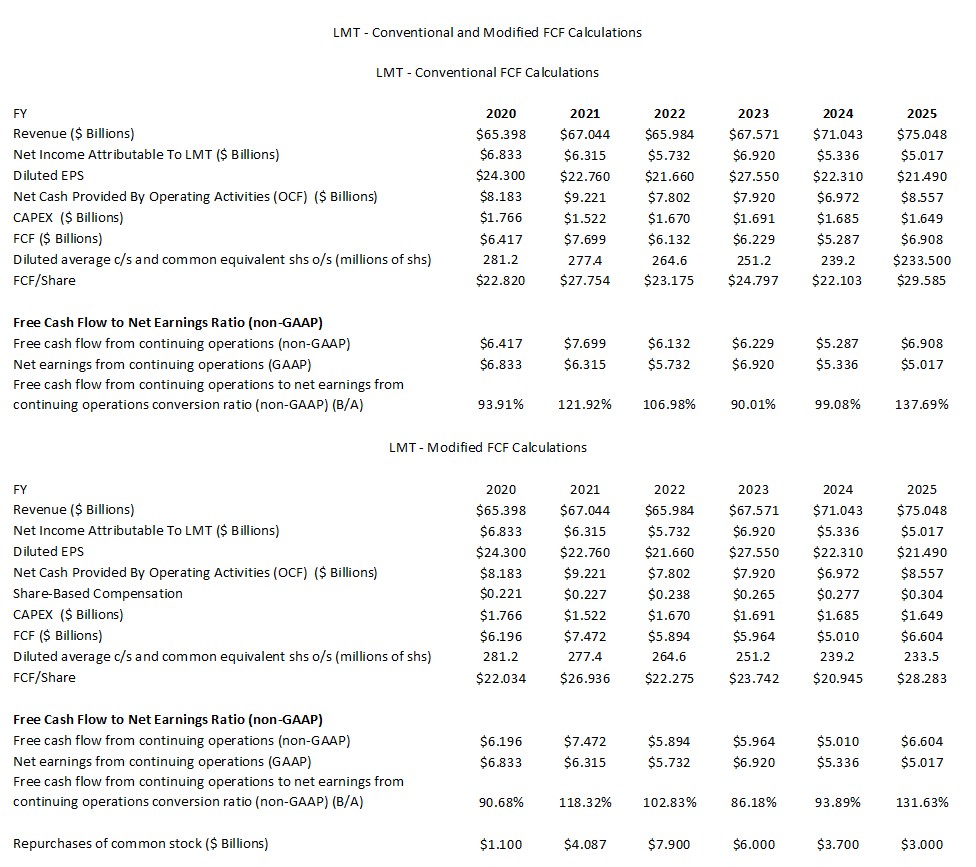

Conventional And Modified Free Cash Flow (FCF) Calculations (FY2020 – FY2025)

In several previous posts I touch upon why I am now taking a conservative approach when looking at a company’s FCF.

FCF is a non-GAAP measure, and therefore, the manner in which we compute it is subject to debate. Most companies subtract capital expenditures (CAPEX) from Net Cash Provided by Operating Activities found in the Consolidated Statement of Cash Flows. As explained in several prior recent posts, I think we need to look at FCF using the conventional method AND a modified method; the modified method also deducts share-based compensation (SBC).

Return On Invested Capital (ROIC)

ROIC is calculated as (

High quality companies often generate a high ROIC. If a company generates a high ROIC, it needs to invest less to achieve a certain growth rate thus reducing the need for external capital.

When a company consistently generates a high ROIC over the long term and it is growing its revenue, it can reinvest a portion of its profits under favorable conditions thereby leading to a compounding effect. I would much rather invest in a growing company that can reinvest to create greater shareholder value than to invest in a company that has limited growth opportunities and thus chooses to distribute a growing dividend.

LMT typically maintains a high and stable ROIC that significantly exceeds its WACC. This ‘spread’ is a key indicator of its ability to create economic value from large-scale defense contracts.

LMT experienced a sharp decline in ROIC starting in 2024. This was primarily driven by:

- Classified Program Losses: In late 2024 and 2025, LMT recognized multi-billion dollar ‘reach-forward’ losses on fixed-price classified programs. Because the ROIC calculation uses Net Operating Profit After Tax (NOPAT), these massive charges directly reduced the numerator of the ratio.

- Inventory & Capital Base: Increased production ramp-ups for the F-35 and missile programs (JASSM/LRASM) expanded the company’s ‘Invested Capital’ base, further putting downward pressure on the ROIC percentage.

LMT’s WACC hit a historic low of ~4.9% in 2021 when interest rates were near zero. As of early 2026, however, its WACC has climbed toward 8.2%.

- LMT maintains a high credit rating, but new debt issuances (such as those in late 2025 to manage liquidity and share repurchases) have carried higher coupon rates.

- Higher risk-free rates (Treasury yields) have increased the return expected by shareholders thus pushing the equity component of WACC higher.

Below is the Return on Invested Capital (ROIC) and the estimated Weighted Average Cost of Capital (WACC).

| Fiscal Year | ROIC (%) | WACC (%) | Economic Spread |

| 2025 | 18.30% | 8.20% | 10.10% |

| 2024 | 23.50% | 7.90% | 15.60% |

| 2023 | 31.40% | 7.10% | 24.30% |

| 2022 | 26.80% | 6.50% | 20.30% |

| 2021 | 32.60% | 4.90% | 27.70% |

| 2020 | 44.30% | 5.40% | 38.90% |

The widening gap between 2020 (~44% ROIC) and 2025 (~18% ROIC) reflects LMT’s transition into more complex, ‘cost-share’ development programs. These lower the immediate ROIC but often secure 20 – 30 year revenue streams once they move into full-rate production.

NOTE: ROIC and WACC are non-GAAP metrics, and therefore, there is inconsistency in the calculation of these metrics. Calculations can vary slightly depending on whether we use GAAP or Non-GAAP operating income (NOPAT) and how ‘Invested Capital’ is defined (e.g. inclusion of goodwill).

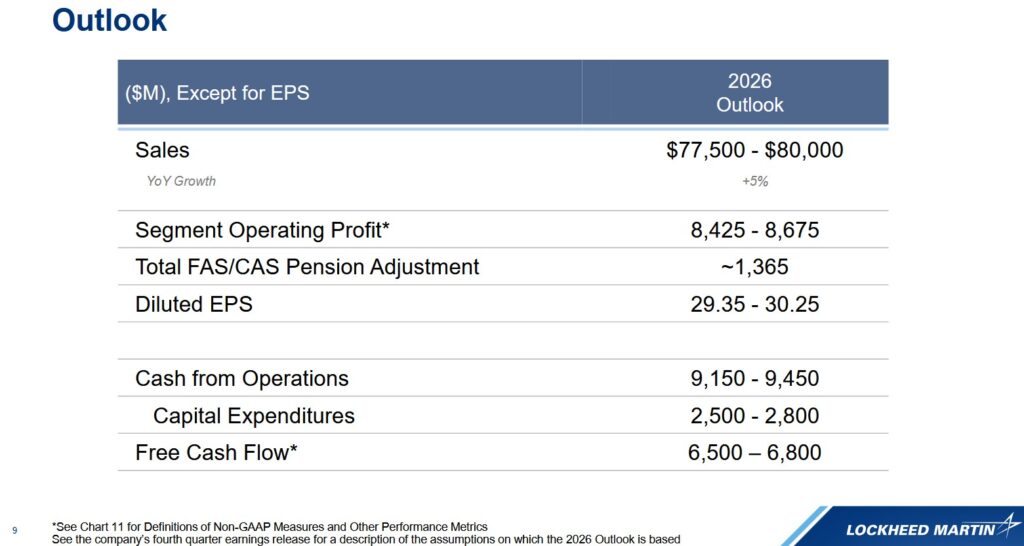

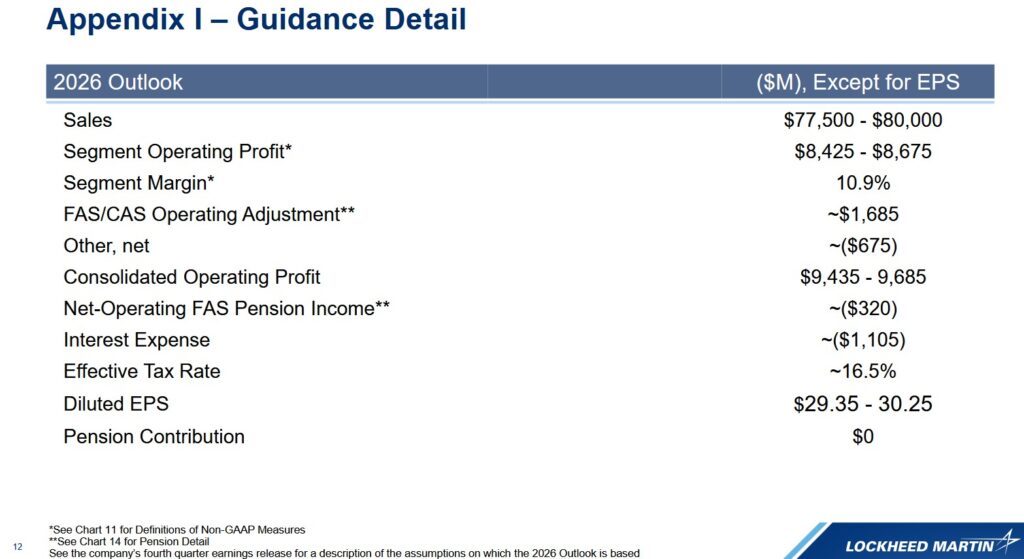

FY2026 Outlook

LMT’s current FY2026 outlook projects a 25% increase in operating profit. This is largely because it believes it has already ‘flushed out’ the worst of the reach-forward losses in the FY2024 – FY2025 period.

Risk Assessment

LMT’s current senior unsecured domestic currency debt ratings are:

- Moody’s: A2 with a stable outlook – last reviewed on August 14, 2023

- S&P Global: A- with a stable outlook – last reviewed on May 20, 2025

- Fitch: A with a stable outlook – last reviewed on May 22, 2025

The rating assigned by S&P Global is the lowest tier of the upper-medium investment grade level; the rating assigned by Moody’s and Fitch is one tier higher.

All 3 ratings define LMT as having a STRONG capacity to meet its financial commitments. LMT is, however, somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

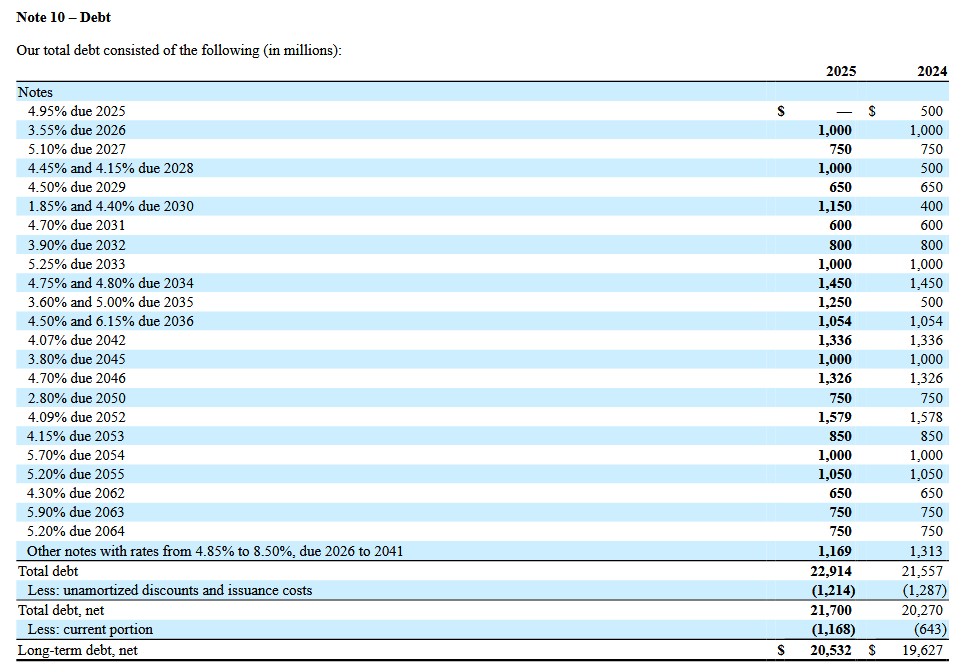

In addition to looking at a company’s credit ratings, I want to know the breakdown of a company’s debt. Details of LMT’s debt is in Note 10 of the FY2025 Form 10-K starting on page 77 of 167. The Form 10-K is accessible through the SEC Filings section of the company’s website.

Dividends

LMT has increased its dividend for 24 consecutive years; its dividend history is accessible here.

LMT is a prolific acquirer of its shares. The weighted average number of shares was ~340 million in FY2011 versus ~233.5 million in Q4 2025.

In FY2020 – FY2025, LMT repurchased $25.787B of its issued and outstanding shares.

Valuation

Management’s adjusted diluted EPS FY2026 outlook is $29.35 – $30.25. Using the current ~$630 share price, the forward adjusted diluted PE range is ~20.8 – ~21.5.

Current broker guidance will change over the next several days but for now, the forward adjusted diluted PE levels using current estimates are:

- FY2026 – 22 brokers – mean of $29.71 and low/high of $29.01 – $30.75. Using the current mean, the forward adjusted diluted PE was ~21.2.

- FY2027 – 19 brokers – mean of $31.67 and low/high of $29.24 – $34.59. Using the current mean, the forward adjusted diluted PE was ~19.9.

- FY2028 – 8 brokers – mean of $33.64 and low/high of $30.87 – $37.23. Using the current mean, the forward adjusted diluted PE was ~18.7.

The mid-point of LMT’s FY2025 FCF outlook is ~$6.65B. If LMT issues ~$0.32B in new shares under its various SBC programs and we deduct this amount from ~$6.65B, the modified FCF is lowered to ~$6.33B.

Suppose LMT repurchases $3B of shares in FY2026 as it did in FY20255. The average purchase price and the timing of the purchases will naturally impact the diluted weighted average number of outstanding shares. If it repurchases shares at an average price of $580 in 2026, this amounts to 5.172 million shares. LMT, however, will issue new shares (perhaps ~$0.32B) under its various SBC programs. At FYE2025, there were 229 million shares outstanding versus 234 million at FYE2024. It does not seem unreasonable to envision a FY2026 weighted average of ~226.5 million shares ((229 + (229 – 5))/2). Based on this, FCF/share under the conventional and modified methods of calculating FCF should be:

- ~$6.65B/226.5 million shares = ~$29.4

- ~$6.33B/226.5 million shares = ~$28

Divide $630 by these FCF/share estimates and we get P/FCF values of ~21.4 and ~22.5.

The following what I reflect in my January 29, 2025 post.

I thought LMT was overvalued at ~$511 when I wrote my July 24, 2024 post. The share price, however, marched higher to a ~$619 52-week high in October 2024. I don’t know what would have possessed anyone to acquire shares at that level but with a pullback to $457.75, I view LMT’s valuation as appealing thus prompting me to acquire 50 more shares.

In FY2024, LMT generated ~$22.31 and ~$27.99 of diluted EPS and adjusted diluted EPS. Based on my purchase price, the trailing PE is ~20.5 and ~16.35, respectively.

Management’s FY2025 adjusted diluted EPS guidance is $27 – $27.30. Using the $27.15 mid-point, the forward adjusted diluted PE is ~16.9.

Current broker guidance will change over the next several days. The forward adjusted diluted PE levels using current estimates, however, are:

- FY2025 – 22 brokers – mean of $27.74 and low/high of $26.75 – $29.20. Using the current mean, the forward adjusted diluted PE was ~16.5.

- FY2026 – 18 brokers – mean of $29.82 and low/high of $28.50 – $31.40. Using the current mean, the forward adjusted diluted PE was ~15.4.

- FY2027 – 10 brokers – mean of $31.55 and low/high of $28.77 – $34.27. Using the current mean, the forward adjusted diluted PE was ~14.5.

- FY2028 – 2 brokers – mean of $32.83 and low/high of $31.19 – $34.46. Using the current mean, the forward adjusted diluted PE was ~14.

Using LMT’s FY2024 $22.103 conventional and $20.945 modified FCF levels, the P/FCF is ~20.7 and ~21.9.

LMT’s FY2025 FCF outlook is ~$6.7B. If we deduct ~$0.27B in new shares issued under its various SBC programs, the modified FCF is lowered to ~$6.43B.

LMT intends to repurchase $3B of shares in FY2025. The average purchase price and the timing of the purchases will naturally impact the diluted weighted average number of outstanding shares. If it repurchases shares at an average price of $500 in 2025, this amounts to 5.4 million shares. LMT, however, will issue new shares under its various SBC programs. In Q4 2024, the weighted average was 237 million shares. It does not seem unreasonable to envision a FY2025 weighted average of 234 million shares. Based on this, FCF/share under the conventional and modified methods of calculating FCF should be:

- ~$6.7B/234 million shares = ~$29

- ~$6.43B/234 million shares = ~$27

Divide my $457.75 purchase price by these FCF/share estimates and we get P/FCF values of ~15.8 and ~17.

Final Thoughts

I like that LMT is moving away from ‘high-risk contracts’ and that it is seeking to eliminate/mitigate program losses. Not only will this appeal to LMT shareholders but I think employees may appreciate working on projects that stand to benefit the company. It must be extremely demoralizing to be working on projects knowing that they could very well result in losses.

Although I like LMT’s long-term outlook, I can not justify increasing my exposure at the current valuation.

The current geopolitical environment has created a level of irrational exuberance when it comes to companies in the aerospace and defense sector. I think acquiring LMT shares at the current valuation may make it difficult to achieve double digit total investment over the next few years.

LMT’s share price can be volatile, and therefore, a pullback to ~$590 (a price I deem attractive) or lower strikes me as being a possibility. Investors, however, may need to bide their time before LMT’s share price retraces to such a level.

At ~$590 and using management’s adjusted diluted EPS FY2026 outlook of $29.35 – $30.25, the adjusted diluted PE retraces to ~19.5 – ~20.1. Even in this range, LMT is not ‘on sale’.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long LMT.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation. I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.