If an investor were to judge Copart (CPRT) solely on its short-term share price behavior, it would be a less than desirable investment. The company’s share price, after all, is just shy of 30% lower than it was on November 21, 2024 (1 year ago).

If an investor were to judge Copart (CPRT) solely on its short-term share price behavior, it would be a less than desirable investment. The company’s share price, after all, is just shy of 30% lower than it was on November 21, 2024 (1 year ago).

As a CPRT shareholder, I am not the least bit concerned about this share price behavior. I approach my investments from the perspective of how it is likely to perform over the very long-term.

I last reviewed Copart (CPRT) in my September 8, 2025 post following the release of Q4 and FY2025 results. With the release of Q1 2026 results following the November 20 market close, this is an opportune time to revisit this existing holding.

Business Overview

CPRT, the largest online salvage vehicle auction operator in the US, was founded in 1982. Since 2003, however, all auctions are online. By holding all auctions online, CPRT is able to connect buyers and sellers around the world.

In my May 28, 2025 post, I provide a brief business overview. I, therefore, dispense with another overview in this post.

Section 1 of CPRT’s Form 10-K provides a good overview of the company (refer SEC Filings). It has ~300,000 paying registered members from virtually every non-sanctioned country. International members account for ~40% of all vehicles sold at US auctions, comprising almost half of auction proceeds. This is because international buyers generally purchase vehicles that are more valuable than those acquired by domestic buyers.

The top 10 individual vehicle buyers collectively purchase a low single-digit percentage of all the vehicles sold at US auctions.

Competition

The following is extracted from CPRT’s FY2025 Form 10-K:

We face significant competition from other remarketers of both salvage and non-salvage vehicles. Against these other vehicle remarketers, we face competition for long-term contractual commitments and various supply agreements with sellers, in addition to competition for the acquisition of vehicle storage facilities. We believe our principal competitors include vehicle auction and sales companies and vehicle dismantlers. These national, regional, and local competitors may have established relationships with vehicle sellers and buyers and may have financial resources that are greater than ours. The largest national or regional vehicle auctioneers in the U.S. include RB Global (RBA) (including its subsidiary Insurance Auto Auctions, Inc.), Carvana, Openlane, Manheim, Inc. and ACV Auctions Inc. The largest national dismantler in the U.S. is LKQ Corporation (‘LKQ’). LKQ, in addition to trade groups of dismantlers such as the American Recycling Association, United Recyclers Group LLC and other regional and local dismantlers, may purchase salvage vehicles directly from insurance companies, thereby bypassing vehicle remarketing companies like Copart entirely. In our International markets, our principal competitors are vehicle auction and sales companies, vehicle dismantlers, and privately-held independent remarketers.

The following are the ratings assigned to CPRT’s competitors. As equity investors, the credit risk is higher than that of debt holders. A shareholder in any of these companies is exposed to non-investment grade risk.

RBA, Carvana, and Openlane all have non-investment grade ratings assigned to their debt. LKQ is the only company with an investment grade rating BUT its domestic long-term unsecured debt rating is the lowest investment grade. Equity investors need to recognize that their risk is greater than that of unsecured creditors. If you are risk averse, avoid these 4 companies.

FYI – One of Carvana’s majority shareholders has a criminal record for fraud.

Financials

Q1 2026 Results

CPRT’s financial results are available through the SEC Filings on the company’s website. The Q1 2026 Form 10-Q, however, is unavailable as I compose this post but should be available shortly.

In Q1 2026, consolidated revenue grew just under 1% YoY to $1.16B, with service revenue increasing just under 1% and purchased vehicle sales increasing nearly 2%.

Fee revenue per unit, however, increased over 7% during the quarter. This was primarily driven by growth in average selling prices which have increased 8.5% from Q1 2025.

It is important to recognize that the 2024 Atlantic hurricane season was classified as ‘extremely active’ by forecasters. Storm numbers and overall energy were well above the long‑term average. The season produced about 18 named storms, 11 hurricanes, and 5 major hurricanes, all above typical seasonal norms.

While the 2025 Atlantic hurricane season was active overall, the US experienced one of its most uneventful hurricane seasons by direct impact. For the first time in a decade, no hurricanes made landfall. Only one named storm, Tropical Storm Chantal, made landfall on the South Carolina coast, causing flooding and power outages.

CPRT is driving higher value units through its marketplace and has developed a more profitable ‘direct buy’ channel to manage lower value units. These lower value units are units which CPRT would have previously purchased through its Copart Direct, Cash for Cars business unit. Now, it earns a referral fee to connect a junk buyer to the individual seller.

As a result of this change, the units are not part of CPRT’s inventory, and it does not incur costs associated with the processing and handling of the unit. Normalizing for this shift, US purchase units increased 6.2% for the prior year period compared to a decline of 19.2% on a reported basis.

As non-insurance units are contributing a greater percentage of CPRT’s overall unit volumes, there is a greater proportion of units which have substantially shorter cycle times being processed through the company’s facilities.

In Q1, the US cycle times decreased by 9% from the prior year period. This improvement in cycle time is decreasing inventory levels and increasing the overall processing capacity of CPRT’s existing facilities.

Despite a negligible change in total service revenues and vehicle sales relative to Q1 2025, CPRT’s Gross Profit as a percentage of sales in Q1 2026 was 46.5% versus 44.65% in Q1 2025. Its Operating Income as a percentage of sales in Q1 2026 was ~37.3% versus ~35.4% in Q1 2025.

At the end of Q1 2026 (October 31, 2025) CPRT’s cash, cash equivalents, and restricted cash and investment in held to maturity securities was just shy of $5.244B. Its TOTAL liabilities, however, were ~$0.962B of which ~$0.031B was deferred revenue. CPRT could essentially wipe out 100% of its liabilities and still have over $4B of cash. In addition, CPRT has a $1.25B unused revolving credit facility maturing on December 21, 2026.

In Q1, CPRT’s Net cash provided by operating activities was ~$0.535B. Net CAPEX in the same quarter was ~$0.1B.

Stock-based compensation continues to be negligible.

Q1 2026 Earnings Call Transcript

The following is CPRT’s CEO commentary from the Q1 2026 earnings call.

Global demand leads to more bidders, more competition and higher price and better price discovery. And again, since 2022, against the backdrop of global economic uncertainty, tariffs and so forth, the share of our U.S. vehicles and auction value that have been purchased by international buyers has continued to grow. In the first quarter of 2026, international buyers have purchased vehicles that are 38% higher in value than comparable U.S. buyers by comparison. We believe that these are long-term durable trends as population growth and mobility demand growth outside the United States, outside the U.K., Canada and so forth continues to outpace what we were experiencing firsthand in our origin markets.

We sometimes face the question as to whether a marketplace like ours can ever experience saturation. That is the unit volume can grow so much that it eclipses the buyer base’s ability to absorb it. I would argue that most historical marketplace analyses in other industries would say quite the opposite. Liquidity begets liquidity. And in fact, since 2022, our unique bidders per auction instance have grown steadily to today’s all-time highs as well.

Capital Allocation Strategy

CPRT doe not distribute a dividend. Reinvesting in the business is CPRT’s capital allocation priority with share repurchases ranking second.

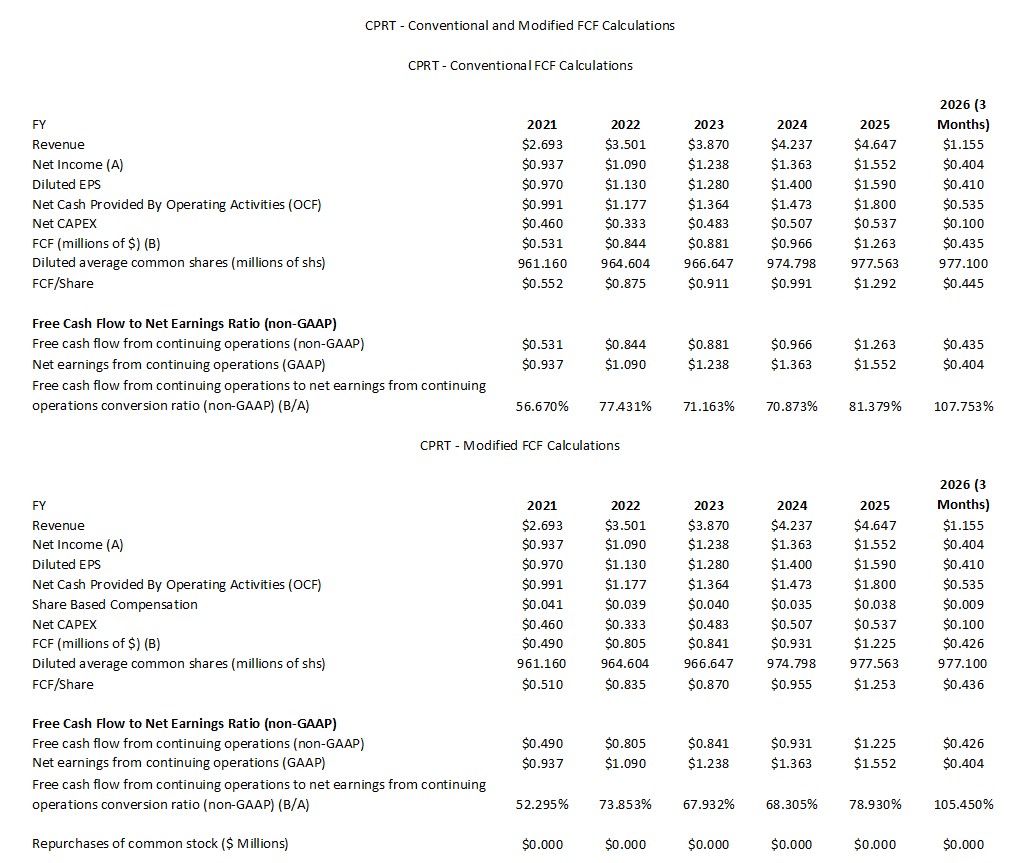

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX

In various prior posts, I deduct stock-based compensation (SBC) when determining a company’s net cash provided by operating activities. This is particularly important when a significant component of a company’s employee compensation is in the form of SBC.

CPRT issues shares to its employees but the annual SBC is negligible. This explains the reason for the moderate FCF variance using the conventional and modified calculation methods.

FY2025 Outlook

CPRT does not provide any outlook.

Risk Assessment

CPRT has no debt to rate.

Dividend and Dividend Yield

CPRT has not paid a cash dividend since becoming a public company in 1994.

Stock Splits

Since becoming a shareholder on January 18, 2022, CPRT has had two 2 for 1 stock splits (November 3, 2022 and August 21, 2023).

In FY2013 – FY2025, CPRT’s weighted average number of outstanding shares (in millions of shares rounded) was 1,038, 1,050, 1,051, 977, 948, 968, 962, 955, 961, 965, 967, 975, and 978.

On September 22, 2011, CPRT’s Board authorized a 320 million share increase in the stock repurchase program, bringing the total current authorization to 784 million shares.

The last time CPRT repurchased any shares was in FY2019 when it repurchased $364.997 million. CPRT has subsequently opted to reinvest in the company to fuel growth.

On the Q1 2026 earnings call, an analyst posed the following question:

The cash on the balance sheet is at record levels and I think the multiple on the shares right now are very close to the multiples that you last time bought stock back. Just given all of the noise in the ecosystem, what are the reasons for maybe not being active on the buyback front maybe over the next 6 to 12 months?

Management’s response was:

CPRT will continue to focus on deploying capital when we see areas that we believe will create meaningful long-term value for the business and for our shareholders. Our first priority remains driving as much expansion as possible for the business through investments (CAPEX or M&A).

We will treat cash as though it is dear to us as it is to anyone. We know it ultimately belongs to shareholders, and we have bought shares back in the past. That’s always been the mechanism by which we return cash to shareholders. There for sure, will come a day that we do that again. And exactly as to how, when and where, I think we always defer. We always suggest that that’s a conversation for another day.

Valuation

As I compose this post on November 22, the share price is ~$40.73.

Using the current broker estimates and the current share price, the forward-adjusted diluted PE levels are:

- FY2026 – 12 brokers – ~24.2 based on the mean of $1.68 and low/high of $1.40 – $1.80.

- FY2027 – 12 brokers – ~21.9 based on the mean of $1.86 and low/high of $1.68 – $2.09.

- FY2028 – 3 brokers – ~20.8 based on the mean of $1.96 and low/high of $1.76 – $2.15.

NOTE: These broker estimates are likely to be revised over the next several days.

I continue to estimate that CPRT will likely generate ~$1.30 of FCF in FY2026. If this materializes, the current P/FCF is ~31.3.

In my September 8, 2025 post, I reflect the following:

In FY2025, CPRT generated $1.59 in diluted EPS. As I compose this post on September 8, the share price is ~$47.88 giving us a PE of ~30.1.

Based on the annual diluted EPS growth in FY2021 – FY2025, I estimate CPRT’s FY2026 diluted EPS will be ~$1.72. This ~$0.13 increase from the FY2025 level is roughly the average annual diluted EPS increase in FY2021 – FY2025. Using my estimate and a ~$47.88 share price, the forward diluted PE is ~27.8.

Using the current broker estimates and share price, the forward-adjusted diluted PE levels are:

- FY2026 – 12 brokers – ~27.8 based on the mean of $1.72 and low/high of $1.65 – $1.80.

- FY2027 – 12 brokers – ~25.2 based on the mean of $1.90 and low/high of $1.80 – $2.09.

NOTE: These broker estimates are likely to be revised over the next several days.

In FY2025, CPRT generated $1.292 and $1.253 of FCF calculated using the conventional and modified methods (see Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX section in this post) resulting in a P/FCF of ~37 and ~38.2.

Looking at CPRT’s FCF trend over the past few years, it is not unreasonable to expect ~$1.30 of FCF in FY2026. At this level, the current P/FCF is ~36.8.

In my May 28, 2025 post, I reflect the following:

In the first 3 quarters of FY2025, CPRT generated $1.18 EPS versus $1.07 in the same period in FY2024.

Using the current broker estimates and my May 28 ~$52.13 purchase price, the forward-adjusted diluted PE levels are:

- FY2025 – 11 brokers – ~33.4 based on the mean of $1.56 and low/high of $1.52 – $1.64.

- FY2026 – 11 brokers – ~29.9 based on the mean of $1.75 and low/high of $1.65 – $1.91.

- FY2027 – 6 brokers – ~26.3 based on the mean of $1.98 and low/high of $1.80 – $2.23.

As noted earlier, I estimate CPRT will generate ~$1.20 and ~$1.16 of FCF in FY2025 calculated under the conventional and modified methods. Using my recent ~$52.13 purchase price, CPRT’s P/FCF is ~43.4 and ~45.

CPRT’s valuation appears rich until we consider its dominant industry position, fortress balance sheet, and growth opportunities. Many investors, however, may have no interest in CPRT because:

- the industry is unappealing;

- it issues no dividend; and/or

- it is not a technology company.

While CPRT is not a technology company, it has revolutionized the salvage industry by employing technology.

Final Thoughts

CPRT has significant liquidity. If shares remain undervalued, I envision CPRT’s Board and senior management will repurchase shares. This is why I hope shares remain undervalued.

The diluted weighted average common shares outstanding in Q1 was 977.1 million. Suppose CPRT deploys $1B to repurchase shares at an average price of $43. This amounts to 23,255,814 shares. Were this to occur, the diluted weighted average common shares outstanding could drop to ~953.8 million. This would have a meaningful impact on CPRT’s valuation.

A repurchase of this magnitude would send a signal to the investment community that management views shares as undervalued and could lead to a recovery in CPRT’s share price.

I consider CPRT to be fairly valued at ~$47. While tempting to acquire additional shares, I currently hold 3200 shares in ‘Core’ accounts and 940 shares in ‘Side’ accounts in the FFJ Portfolio. Young investors I am helping on their journey to financial freedom also have CPRT exposure. I am, therefore, satisfied with my current exposure.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long CPRT.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.