In my July 26, 2025 CME Group Inc. (CME) post, I state that CME’s Board authorized up to $3B in opportunistic share buybacks. On October 10, 2025, CME and S&P Global (SPGI) announced the completion of the sale of their 50/50 OSTTRA joint venture to KKR for ~$3.1B. Given these two events, I envision CME will begin to address my concern about the steadily increasing average diluted shares outstanding.

In my July 26, 2025 CME Group Inc. (CME) post, I state that CME’s Board authorized up to $3B in opportunistic share buybacks. On October 10, 2025, CME and S&P Global (SPGI) announced the completion of the sale of their 50/50 OSTTRA joint venture to KKR for ~$3.1B. Given these two events, I envision CME will begin to address my concern about the steadily increasing average diluted shares outstanding.

With the October 22, 2025 release of Q3 and YTD2025 results, this is an opportune time to review this existing holding.

Business Overview

CME operates a derivatives marketplace which offers a range of futures and options products for risk management. It is where market participants turn to manage risk across the most diverse set of benchmark products.

The company’s website and Part 1 of the FY2024 Form 10-K are great source of information to learn more about the company.

Financials

Q3 and YTD2025 Results

The Q3 and YTD2025 earnings release is accessible through the SEC Filing section of the company’s website.

On the Q3 2025 earnings call, management stated:

The third quarter average daily volume of 25.3 million contracts represented the second highest third quarter average daily volume in our history, following the record quarter a year ago. Customers continue to turn to our markets to manage their risk exposures as demonstrated by year-end open interest of 126 million contracts, the highest open interest at end of September in the last 5 years and continuing to grow in October.

We also set records in large open interest holders in interest rates, equity indices, and cryptocurrencies in September despite a general pullback in volatility across asset classes during the quarter.

Our crypto complex traded a record 340,000 contracts per day in the third quarter and was up over 225% relative to a year ago. This growth was aided by the early success of Solana and XRP futures, which we launched earlier this year. Other new products with record volume in the third quarter include credit futures, 1 ounce gold futures and agricultural weekly options.

Additionally, we announced our intention to offer 24/7 trading of cryptocurrency futures and options beginning early next year.

FanDuel Alliance

In August 2025, CME and and FanDuel, America’s premier online gaming company, part of Flutter Entertainment (FLUT), announced an alliance that will launch new products and expand access to financial markets for millions of FanDuel customers in the United States.

Together, the companies will develop new fully funded, event-based contracts with defined risk. Customers will be able to express their views multiple times a day on a wide range of markets with simple “yes” or “no” positions for as little as $1.

Expected to launch later this year, the products will include benchmarks such as the S&P 500 and Nasdaq-100, prices of oil and gas, gold, cryptocurrencies, and key economic indicators such as GDP and CPI.

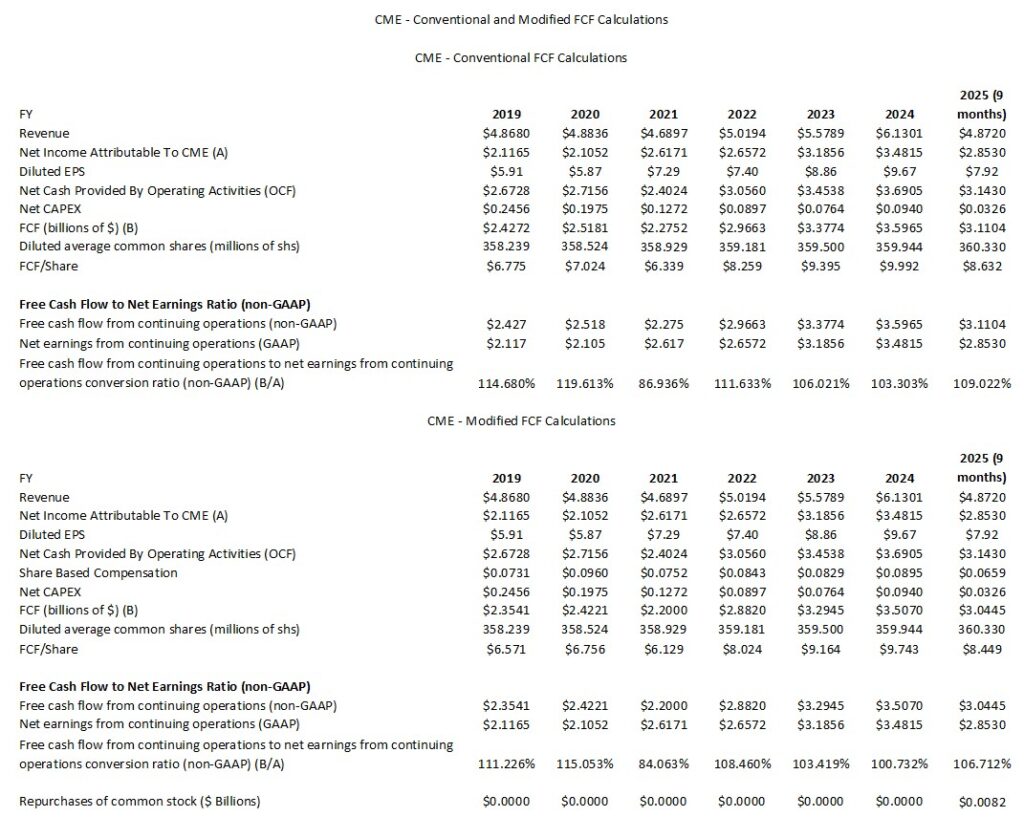

Conventional And Modified Free Cash Flow (FCF) Calculations (FY2019 – FY2024 and YTD2025 (9 months))

FCF is a non-GAAP measure, and therefore, its calculation is inconsistent. Many investors deduct CAPEX from OCF to arrive at FCF. In my How Stock Based Compensation Distorts Free Cash Flow post, I explain why I now also deduct stock based compensation (SBC) that is found in the Consolidated Statements of Cash Flows to determine FCF.

The conventional method only deducts CAPEX from OCF while the more conservative modified method also deducts SBC.

FY2025 Guidance

CME does not issue earnings guidance. When it released FY2024 results in February 2025, however, management provided the following:

We expect total adjusted operating expenses, excluding license fees, but including cloud migration expenses to be ~$1.65B. Total capital expenditures are expected to be ~$90 million, and the adjusted effective tax rate should come in between 22.5% – 23.5%. In December, we announced transaction fee adjustments, which became effective February 1.

Assuming similar trading patterns as 2024, the fee adjustments would increase futures and options transaction revenue by ~ 1% – ~1.5%.

Market data fees were increased by 3.5% at the beginning of the year.

Additionally, we announced a 10 basis point noncash collateral surcharge effective in April for participants that do not post at least 30% of their margin requirement in cash. This change will ensure a minimum level of cash for risk management purposes. The financial impact of this requirement will be dependent on customer decisions and may result in an increased average rate on noncash collateral or an increase in cash posted at the clearinghouse.

As always, we focused on the total cost of trade for our clients and considered the impact of the fee changes when reviewing adjustments to the clearing and transaction fees this year. In aggregate, the fee changes in cash minimum could add 2% – 2.5% to pretax income, assuming similar volume and collateral levels.

On the Q3 2025 earnings call, management provided the following update:

We expect total adjusted operating expenses for the year, excluding license fees, to be approximately $1.625 billion. That’s $10 million below our prior guidance and a total of $25 million below our expectations to start the year.

Risk Assessment

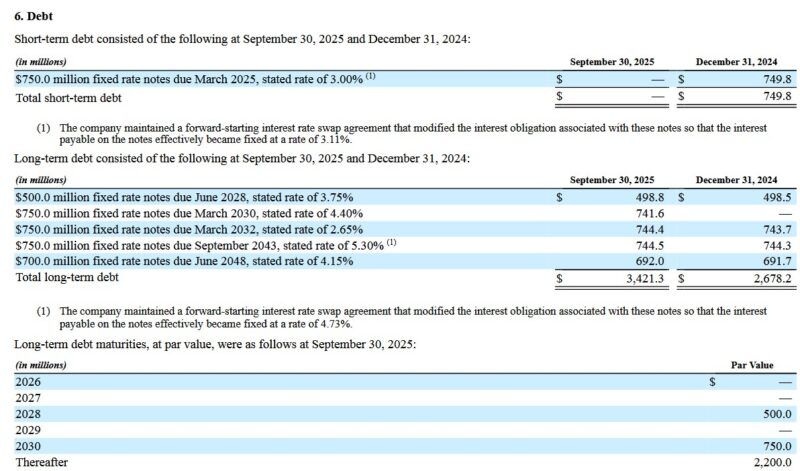

In March 2025, CME completed an offering of $750.0 million of its 4.4% fixed rate notes due March 2030 and also repaid the $750.0 million of 3% fixed rate notes due March 2025. CME now has no debt maturing until FY2028.

CME’s senior unsecured long-term debt ratings are the lowest tier of the high-grade category and are investment grade. These ratings define CME as having a VERY STRONG capacity to meet its financial commitments. It differs from the highest-rated obligors only to a small degree.

- Moody’s: Aa3 with a stable outlook (affirmed May 19, 2025)

- S&P Global: AA- with a stable outlook (affirmed July 18, 2025)

- Fitch: AA- with a stable outlook (affirmed February 6, 2025)

These strong ratings are acceptable for my risk tolerance.

Dividend and Dividend Yield

The following is reflected in CME’s FY2024 Form 10-K.

We intend to continue to pay a regular quarterly dividend to our shareholders, with a target of between 50% to 60% of the prior year’s cash earnings. The decision to pay a dividend and the amount of the dividend, however, remains within the discretion of our board of directors and may be affected by various factors, including our earnings, financial condition, capital requirements, levels of indebtedness and other considerations our board of directors deems relevant. We are also required to comply with restrictions contained in the general corporation laws of our state of incorporation, which could limit our ability to declare and pay dividends.

CME’s dividend history is accessible here.

NOTE: In conjunction with the December 5, 2024 declaration of the ‘special’ variable dividend, CME indicated that it intends to continue its variable dividend structure. Beginning in 2026, however, the declaration and payment of the annual variable dividend will align with the first quarter regular dividend paid in March 2026. The ‘special’ variable dividend used to be paid in mid-January.

In FY2014 and FY2024, the weighted average outstanding diluted shares outstanding (in millions of shares rounded) was 336.063 and 359.944. In the 9 months ending September 30, 2025, it was ~360.297.

When CME announced that its Board approved a share repurchase program in December 2024, I envisioned it would start addressing the concern I expressed at the outset of this post – the steady growth of diluted outstanding shares.

In the September 2025 CME Group Overview presentation, we see that opportunistic share repurchases is now a component of CME’s capital return to shareholders. This presentation is accessible under Investor Materials and Investor Presentation.

Valuation

I exclude any opportunistic share repurchases in my valuation estimates.

YTD2025, CME generated $7.92 of diluted EPS and $8.43 of adjusted diluted EPS.

CME’s current share price is $269.54. Using the current forward adjusted diluted EPS broker estimates, CME’s forward adjusted diluted PE levels are:

- FY2025 – 16 brokers – mean of $11.12 and low/high of $10.88 – $11.53. Using the mean estimate, the forward-adjusted diluted PE is ~24.2.

- FY2026 – 16 brokers – mean of $11.62 and low/high of $11.03 – $12.14. Using the mean estimate, the forward-adjusted diluted PE is ~23.2.

- FY2027 – 11 brokers – mean of $12.38 and low/high of $11.55 – $12.96. Using the mean estimate, the forward-adjusted diluted PE is ~21.8.

CME’s YTD2025 FCF/share is ~$8.632 and ~$8.449 using the conventional and modified calculated methods. I do not anticipate any share repurchases the remainder of the year. Additional SBC in Q4 is unlikely to materially change the number of outstanding shares. I, therefore, use ~360.4 million shares the gauge CME’s valuation; the YTD weighted average is ~360.33 million.

If CME generates a similar level of FCF in Q4 as in the prior 3 quarters, FY2025 FCF could be ~$11.5 and ~$11.27 (I have added ~33.3% of YTD FCF to estimate FY2025 FCF).

Divide the current $269.54 share price by these FCF estimates and CME’s P/FCF is ~23.4 and ~24. CME’s FCF conversion ratio is typically above 100%. It is, therefore, reasonable to expect CME’s valuation based on FCF to be superior to that based on adjusted diluted EPS.

NOTE: These valuations could improve depending on the extent to which CME repurchases shares.

In my July 26, 2025 post, I estimated CME’s valuation using July 25’s $279.55 closing share price.

Management does not provide earnings guidance, and therefore, I extrapolate YTD2025 results. In the first half of FY2025, CME generated diluted EPS and adjusted diluted EPS of $5.43 and $5.75. If the second half of the year is relatively similar to the first half, FY2025 diluted EPS and adjusted diluted EPS should be ~$10.86 and ~$11.50. Erring on the side of caution, I use the ~$11.18 mid-point thus suggesting the current adjusted diluted PE is ~25.

Using the current forward adjusted diluted EPS broker estimates, CME’s forward adjusted diluted PE levels are:

- FY2025 – 17 brokers – mean of $11.15 and low/high of $10.75 – $11.53. Using the mean estimate, the forward-adjusted diluted PE is ~25.1.

- FY2026 – 17 brokers – mean of $11.59 and low/high of $10.94 – $12.11. Using the mean estimate, the forward-adjusted diluted PE is ~24.1.

- FY2027 – 11 brokers – mean of $12.39 and low/high of $11.57 – $13.06. Using the mean estimate, the forward-adjusted diluted PE is ~22.6.

CME’s YTD2025 FCF/share is ~$5.946 and ~$5.830 using the conventional and modified calculated methods. I do not anticipate any share repurchases the remainder of the year. Fortunately, additional SBC in the second half of the year is unlikely to be meaningful. Given this, the weighted average diluted shares outstanding in FY2025 should be just marginally higher than the YTD weighted average. On this basis, I estimate CME’s FY2025 FCF will be ~$11.90 and ~$11.67. Divide the current $279.55 share price and CME’s P/FCF is likely close to ~23.5 and ~24. CME’s FCF conversion ratio is typically above 100% so it seems reasonable to expect CME’s valuation based on FCF to be slightly superior to that based on adjusted diluted EPS.

Final Thoughts

I currently hold 478 shares in in a ‘Core’ account and 413 shares in a ‘Side’ account within the FFJ Portfolio.

On June 29, 2020, I initiated a 300 share position @ $162.13. I subsequently acquired additional shares in May 2022 (30 @ $204.665), July 2022 (50 @ $195.315), and November 2022 (50 @ $173.575) in a ‘Core’ account in the FFJ Portfolio. The additional 48 shares were acquired through the automatic reinvestment of dividend income.

My last purchase was 400 shares @ $197.985 on June 10, 2024 in a ‘Side’ account. The additional 13 shares were acquired through the automatic reinvestment of dividend income.

When I completed my 2025 Mid-Year Portfolio Review, CME was my 11th largest holding.

Despite the comments in my Dividends Have Drawbacks post, I am a CME shareholder because I like the business and long-term prospects.

Now that opportunistic share repurchases are a component of CME’s capital return to shareholders I am considering adding to my exposure.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long CME.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.