![]() In my September 24, 2025 post, I disclose the purchase of an additional 100 shares @ $200.79 bringing my total exposure to 600 shares in a ‘Side’ account in the FFJ Portfolio. When I wrote that post, CTAS had just released its Q1 2026 results. Subsequently, an improvement in valuation prompted me to acquire an additional 100 shares in the same account @ ~$181.455/share. I disclose this purchase in my November 3, 2025 post.

In my September 24, 2025 post, I disclose the purchase of an additional 100 shares @ $200.79 bringing my total exposure to 600 shares in a ‘Side’ account in the FFJ Portfolio. When I wrote that post, CTAS had just released its Q1 2026 results. Subsequently, an improvement in valuation prompted me to acquire an additional 100 shares in the same account @ ~$181.455/share. I disclose this purchase in my November 3, 2025 post.

In my December 8, 2025 post, I raise the question of whether CTAS could take another run at trying to acquire Unifirst (UNF) – its largest US competitor. In that post I touch upon pressure being placed on UNF’s Board by large independent shareholders regarding UNF’s need to improve governance and initiate a review of strategic alternatives.

UNF’s 2026 Annual Meeting of Shareholders was held on December 15, 2025. The preliminary vote count from UNF’s proxy solicitor indicates that UNF’s nominees were re-elected to the UNF Board of Directors at the Company’s Annual Meeting of Shareholders. This comes as no surprise as the founder’s family controls over 70% of the vote with only an economic interest of ~19.6%.

Following the preliminary vote count, UNF’s Board issued the following statement:

The Board and management team appreciate the active dialogue we have had with our shareholders and look forward to further constructive engagement to advance our common goal of enhancing value. We remain open-minded and will continue to take actions and make decisions that we believe are in the best interest of all UniFirst shareholders.

It remains to be seen whether UNF’s Board is prepared to renegotiate with CTAS if an offer is presented.

In the interim, I revisit CTAS now that we have the Q2 and YTD2026 results that were issued on December 18.

Business Overview

Part 1 Item 1 in the FY2025 Form 10-K and the company’s website provide a good overview of the company.

Financial Results

Q2 and YTD2026 Results

The December 18, 2025 earnings release reflecting Q2 and YTD2026 results is accessible through CTAS’s website (a link to the company’s EDGAR Filings on the SEC website).

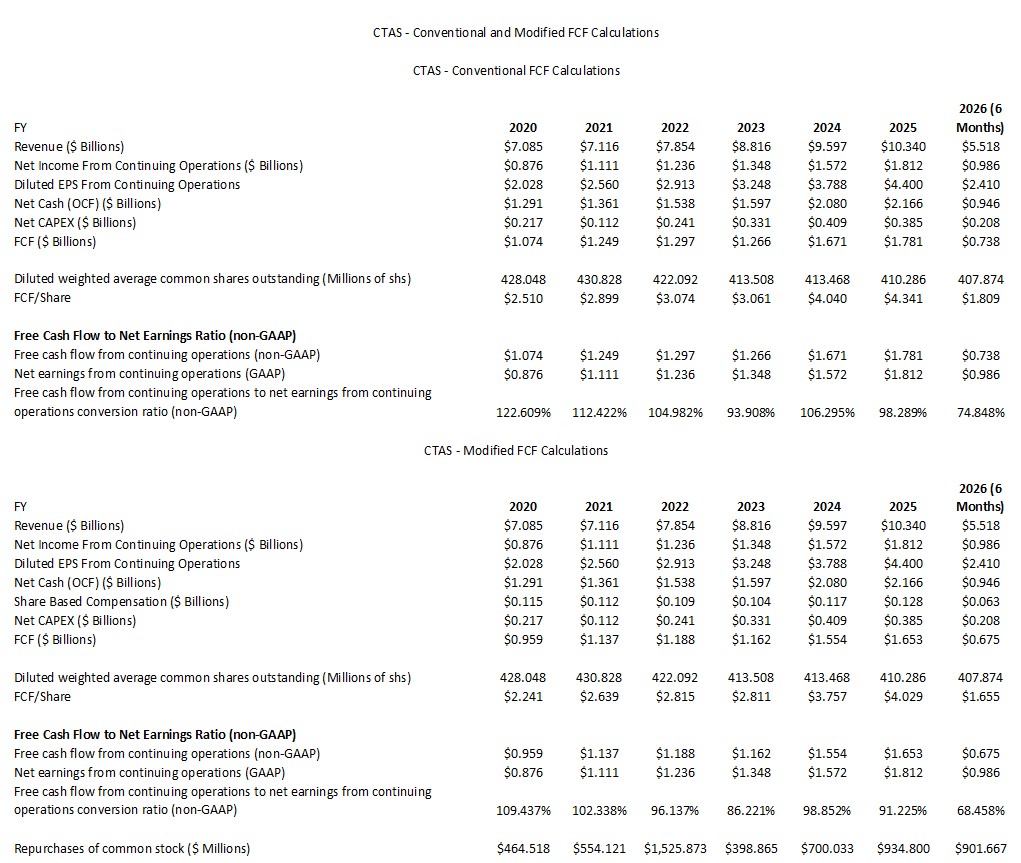

Conventional And Modified Free Cash Flow (FCF) Calculations (FY2020 – FY2025 and YTD2026)

FCF is a non-GAAP measure, and therefore, its method of calculation is open to debate. Most companies subtract capital expenditures (CAPEX) from Net Cash Provided by Operating Activities found in the Consolidated Statement of Cash Flows.

The ‘conventional’ calculations do not deduct share-based compensation (SBC) while the ‘modified’ calculations deduct SBC. In several posts, I touch upon why I deduct SBC when analyzing a company’s FCF.

FY2026 Outlook

Current Outlook with the release of Q2 2026 results

- FY2025 and FY2026 have the same number of workdays for the year and by quarter;

- The exclusion of any future acquisitions;

- A constant foreign currency exchange rate;

- FY2026 net interest of ~$0.104B compared to $95.5 million in FY2025, primarily as a result of refinancing senior notes at a higher interest rate in Q4 2025, as well as higher variable rate interest expense from commercial paper as a result of buyback activity during FY2026. Expected net interest may change as a result of future share buybacks or acquisition activity.

- A ~20% effective tax rate which is the same as FY2025.

Prior Outlook with the release of Q1 2026 results

- FY2025 and FY2026 have the same number of workdays for the year and by quarter;

- The exclusion of any future acquisitions;

- A constant foreign currency exchange rate;

- FY2026 net interest of ~$0.097B compared to $95.0 million in FY2025, primarily as a result of refinancing senior notes at a higher interest rate, partially offset by lower variable rate interest. Expected net interest may change as a result of future share buybacks or acquisition activity.

- A ~20% effective tax rate which is the same as FY2025.

Prior Outlook with the release of Q4 2025 results

- FY2025 and FY2026 have the same number of workdays for the year and by quarter;

- The exclusion of any future acquisitions;

- A constant foreign currency exchange rate;

- FY2026 net interest of ~$0.098B.

- A ~20% effective tax rate which is the same as FY2025.

Risk Assessment

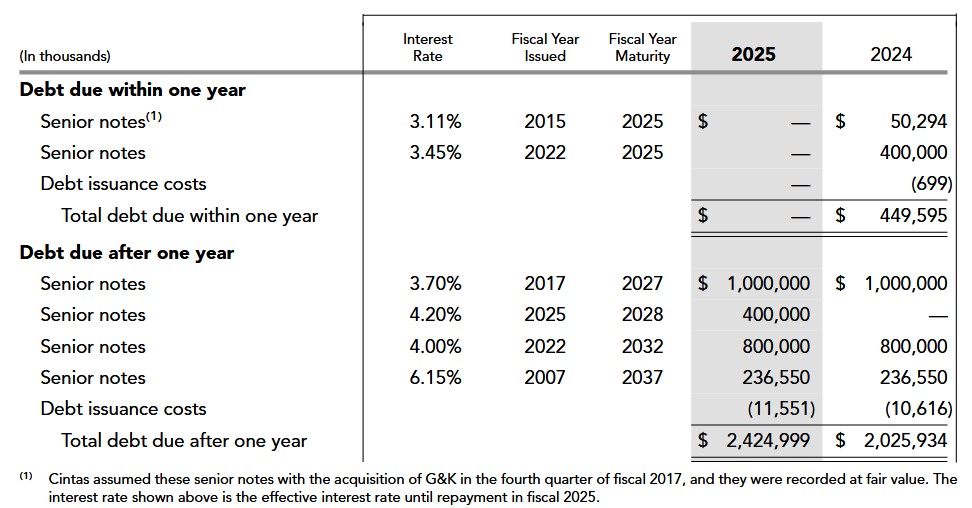

The following reflects CTAS’s outstanding debt at FYE2025.

The amount owing at the end of Q2 2026 is ~$2.977B of which ~$0.551B is due within 1 year and ~$2.427B is debt due after 1 year. The ~$0.551B is commercial paper issued in Q2. Proceeds aided in the repurchase of outstanding CTAS shares.

CTAS’s credit agreement supports its commercial paper program; the revolving credit facility is in the amount of $2B. The credit agreement includes an accordion feature that provides the company with the ability to request increases to the borrowing commitments under the revolving credit facility of up to $0.5B in the aggregate, subject to customary conditions.

The maturity date of the revolving credit facility is March 23, 2027.

CTAS uses interest rate locks to manage its overall interest expense; interest rate locks effectively change the interest rate of specific debt issuances. These interest rate locks are entered into to protect against unfavorable movements in the benchmark treasury rate related to forecasted debt issuances. These interest rate locks represent cash flow hedges employed to hedge against movements in the treasury rates at the time the company issued its senior notes.

CTAS’s domestic senior unsecured long-term debt ratings are:

- Moody’s: A3 with a stable outlook (last reviewed on May 7, 2025)

- S&P Global: A- with a stable outlook (last reviewed on March 10, 2025)

Both ratings are the bottom tier of the upper medium-grade investment-grade category. These ratings define CTAS as having a strong capacity to meet its financial commitments. It is, however, somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

Dividends and Share Repurchases

Dividend and Dividend Yield

CTAS’s dividend history is accessible here.

Little of CTAS’s total long-term shareholder return is likely to come from the quarterly dividend. I, therefore, recommend assigning little weight to the dividend aspect of this investment.

Share Repurchases and Stock Splits

On October 28, 2025, CTAS announced a new $1B stock buyback authorization.

The table provided earlier in this post reflects the dollar value of shares repurchased and the diluted weighted average common shares outstanding in FY2020 – FY2025 and Q2 2026.

CTAS’s FY2026 diluted EPS guidance excludes any future potential share buybacks. It is, however, opportunistically repurchasing shares. In Q2 and as of December 17, CTAS was active in the buyback program with repurchases totaling $622.5 million. This marks the third largest share repurchase made in a quarter.

CTAS’s stock split history is:

- September 11, 2024: 4:1

- November 18, 1997: 2:1

- April 2, 1992: 2:1

- April 2, 1991: 1.5:1

- April 2, 1987: 2:1

Valuation

The current share price is ~$187.60. Using management’s current $4.81 – $4.88 adjusted diluted EPS outlook, the forward adjusted diluted PE is ~38.4 – ~39.

NOTE: CTAS’s diluted EPS and adjusted diluted EPS are likely to continue to be relatively similar.

Its valuation using the current broker guidance is:

- FY2026 – 21 brokers – mean of $4.87 and low/high of $4.80 – $4.94. Using the mean, the forward adjusted diluted PE is ~38.5.

- FY2027 – 21 brokers – mean of $5.40 and low/high of $5.24 – $5.57. Using the mean, the forward adjusted diluted PE is ~34.7.

- FY2028 – 13 brokers – mean of $5.95 and low/high of $5.62 – $6.25. Using the mean, the forward adjusted diluted PE is ~31.5.

I continue to estimate that the FY2026 FCF conversion ratio will be ~98% (calculated under the conventional method) and ~94% (calculated under the modified method). Using a ~$4.85 mid-point of management’s FY2026 guidance, CTAS’s FY2026 FCF is likely to be ~$4.75 (conventional) and ~$4.56 (modified). From these figures and the current ~$187.60 share price, I estimate CTAS’s forward P/FCF is ~39.5 and ~41.1 (calculated using the conventional and modified FCF values).

This could significantly change depending upon the extent to which CTAS repurchases shares.

For comparison, the following is my valuation commentary from November 3, 2025 post.

Using my recent $181.455 purchase price and management’s current $4.74 – $4.86 adjusted diluted EPS outlook, the forward adjusted diluted PE is ~37.3 – ~38.3.

NOTE: CTAS’s diluted EPS and adjusted diluted EPS are likely to continue to be relatively similar.

Its valuation using the current broker guidance is:

- FY2026 – 19 brokers – mean of $4.84 and low/high of $4.78 – $4.90. Using the mean, the forward adjusted diluted PE is ~37.5.

- FY2027 – 19 brokers – mean of $5.36 and low/high of $5.15 – $5.55. Using the mean, the forward adjusted diluted PE is ~33.9.

- FY2028 – 10 brokers – mean of $5.92 and low/high of $5.53 – $6.20. Using the mean, the forward adjusted diluted PE is ~30.7.

I continue to estimate that the FY2026 FCF conversion ratio will be ~98% (calculated under the conventional method) and ~94% (calculated under the modified method). Using a $4.80 mid-point of management’s FY2026 guidance, CTAS’s FY2026 FCF is likely to be ~$4.70 (conventional) and ~$4.51 (modified). From these figures and my ~$181.455 purchase price, I estimate CTAS’s forward P/FCF is ~38.6 and ~40.2 (calculated using the conventional and modified FCF values).

This could significantly change depending upon the extent to which CTAS repurchases shares.

Final Thoughts

I currently hold 701 CTAS shares in a ‘Side’ account in the FFJ Portfolio at an average cost of ~$186.49. One share was purchased on December 15 through the automatic reinvestment of the dividend income.

I consider shares to be fairly valued and view this as an opportunity to acquire additional shares; CTAS’s valuation rarely drops into fairly valued territory.

I would like to increase my exposure in the account that currently holds 701 shares. This account, however, has insufficient liquidity to make a meaningful purchase. Over the next few days I will determine through which account I can purchase additional shares. I will also recommend that a couple of young investors I am helping on their journey to financial freedom consider CTAS as a potential investment.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long CTAS.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.