![]()

I initiated a Becton Dickinson (BDX) position on February 11, 2009 @ ~$70.55 in a retirement account. I gradually increased my exposure over the years while the company performed well.

In October 2022, I exited 100% of my BDX exposure in the retirement account as part of our Registered Retirement Savings Plan (RRSP) meltdown strategy.

I, however, built another BDX position in a ‘Core’ account in the FFJ Portfolio and currently hold 647 shares at an average cost of ~$227.77.

My rate of return on my BDX investment was decent for the first few years. The company’s performance, however, has been abysmal the past several years. When I composed my May 2, 2025 ‘Can Becton Dickinson Regain Investor Confidence?’ post, I remained cautiously optimistic that it would stop testing my patience.

In an effort to restore investor confidence, the company has undergone a radical transformation. I touch upon this in the Capital Allocation section of this post.

This an opportune time to revisit this existing holding now that the Q1 2026 results and FY2026 guidance are available.

Business Overview

Good sources of information to learn about BDX are its website and its FY2025 Annual Report/Form 10-K.

Financials

Q1 2026 Results

BDX’s most recent results are accessible here.

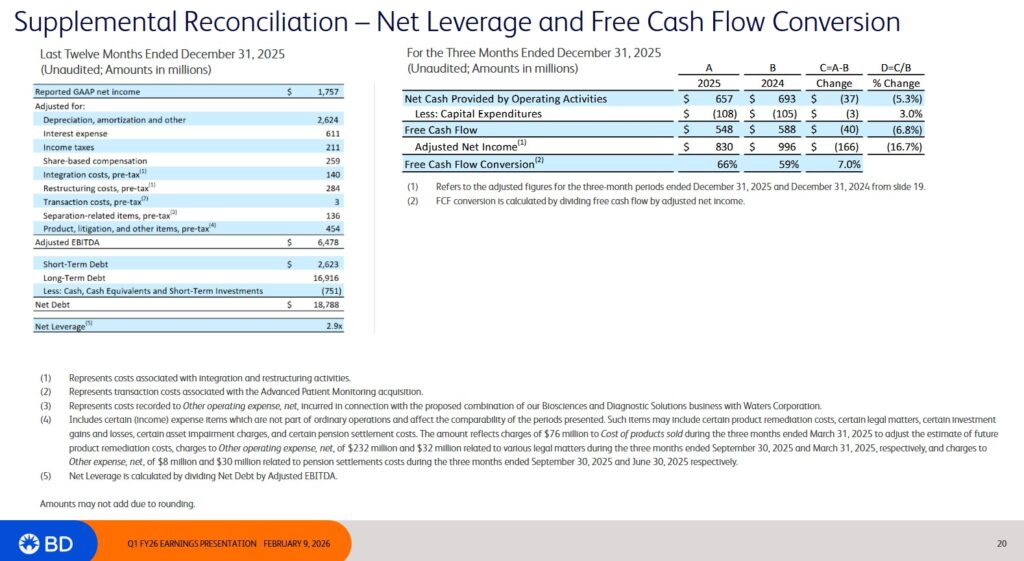

Net leverage (Net Debt/Adjusted EBITDA) at FYE2021, FYE2022, FYE2023, FYE2024, FYE2025, and Q1 2026 was 2.6x, 2.8x, 2.6x, 2.6x, 3.0x, 2.8x, and 2.9x.

On the Q1 2026 earnings call with analysts, management reiterated its commitment to a 2.5x long-term net leverage target. The $2B debt repayment from the $4B proceeds generated from exiting the Biosciences & Diagnostic Solutions business will go a long way in improving BDX’s net leverage ratio.

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX

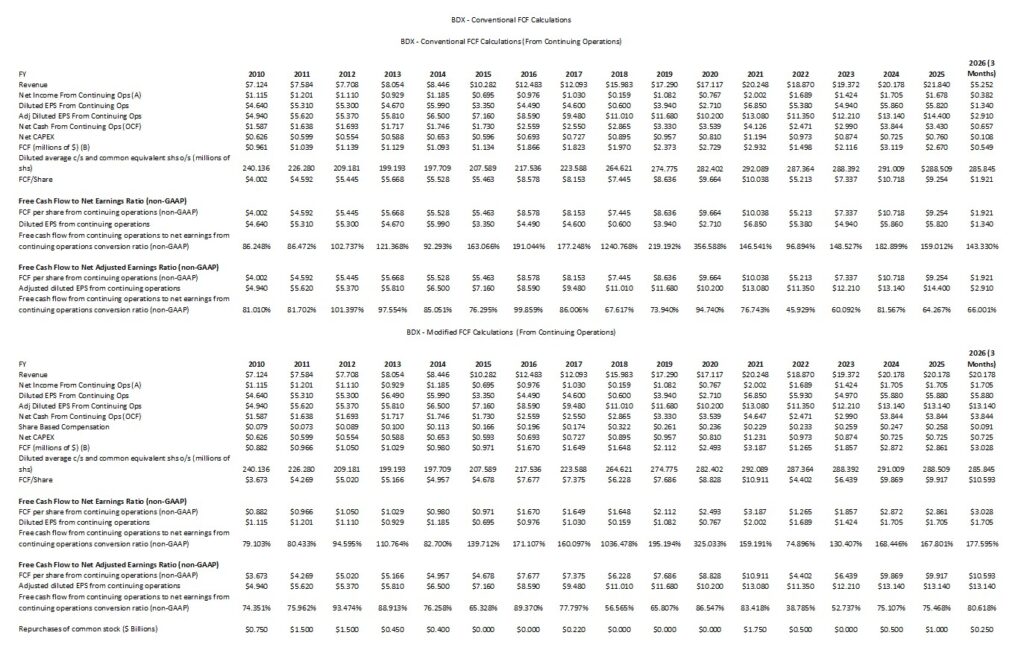

BDX merely deducts CAPEX from its net cash provided by continuing operating activities to determine its FCF. In several prior posts, I explain my rationale for deducting share based compensation (SBC) when determining FCF.

As reflected in BDX’s Q1 2026 earnings presentation, BDX uses adjusted net income to calculate its FCF conversion ratio. BDX’s adjusted diluted EPS, however, differs considerably from GAAP diluted EPS as far back as FY2013!

The following table calculates BDX’s FCF conversation ratio using GAAP and non-GAAP EPS. There is a significant variance in the FCF conversion ratio because BDX has had so many adjustments to its GAAP earnings over the past decade.

Capital Allocation

BD’s capital allocation from FY2018 – FY2025 is defined by a transition from deleveraging following the massive Carefusion (~$12.2B) and C.R. Bard (~$24B) acquisitions in FY2015 and FY2017 to portfolio simplification and disciplined shareholder returns.

The period is broken down into three distinct phases.

The Deleveraging Phase (2018–2020)

BDX’s primary capital allocation goal was debt reduction. Management prioritized using free cash flow to pay down debt and paused share repurchases. Despite the focus on debt reduction, BDX maintained its decades-long streak of annual dividend increases.

The ‘BDX 2025’ Strategy & Tuck-in M&A (2021–2024)

As leverage ratios improved, BDX shifted toward a strategy titled ‘Grow, Simplify, Empower’.

Instead of massive M&A transactions, BDX focused on smaller, high-growth ‘tuck-in’ acquisitions (over 20 deals by 2025, adding ~$1.3B in revenue). One such acquisition was the ~$4.2B acquisition of Edwards Lifesciences’ Critical Care unit in 2024 (rebranded as Advanced Patient Monitoring).

BDX also began to aggressively spin off slower-growth or non-core assets to focus on higher-margin MedTech. In April 2022, it spun off its Diabetes Care business as a standalone public company Embecta (EMBC).

In 2021, BDX resumed share repurchases as leverage approached its target of ~2.5x.

The ‘New BDX’ & Simplification Capstone (2025)

FY2025 marks a major pivot toward becoming a ‘pure-play’ MedTech leader.

On February 9, 2026, BDX completed the combination of its Biosciences & Diagnostic Solutions business with Waters Corporation (WAT) via a ‘Reverse Morris Trust’ structure at a value of ~$18.8B. A ‘Reverse Morris Trust’ is a tax-efficient way to spin off and merge a business unit.

Following this separation, BDX is now a ‘new BDX’.

The value BDX realized is through:

- A cash payment of $4B immediately prior to the February 9, 2026 closing.

- BDX shareholders will also receive ~0.135 shares of WAT common stock for every BDX share held. This results in BDX shareholders owning 39.2% of the newly combined WAT.

NOTE: I intend to sell my WAT shares upon receipt.

BDX has publicly committed to using the $4B cash payment to:

- repurchase $2B of its shares through an accelerated share repurchase program (ASR).

- repay $2B of debt.

This divestiture marks the final major milestone of the ‘BDX 2025′ strategy, leaving BDX as a ‘pure-play’ medical technology company focused on its Medical Essentials, Connected Care, and Interventional segments.

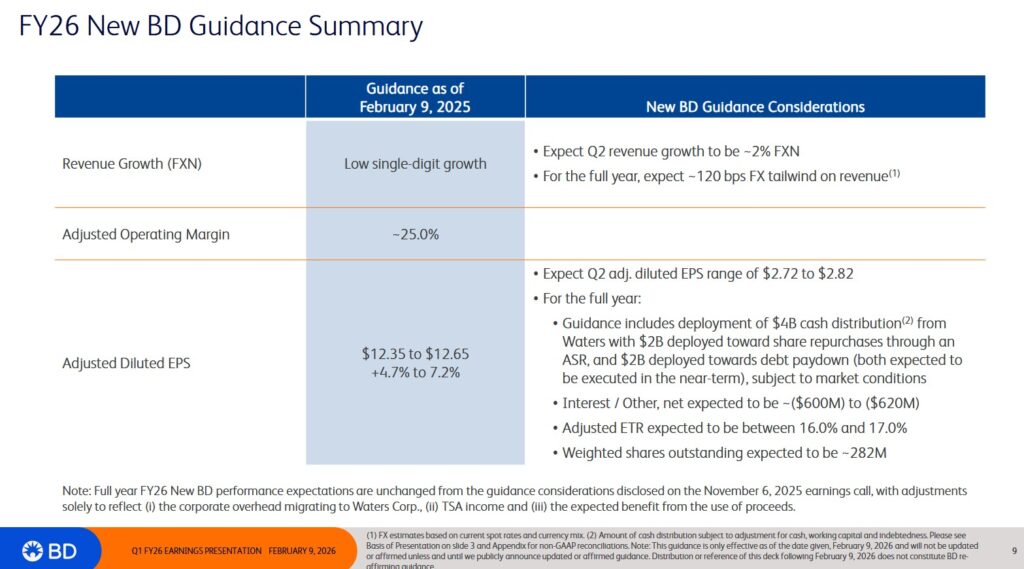

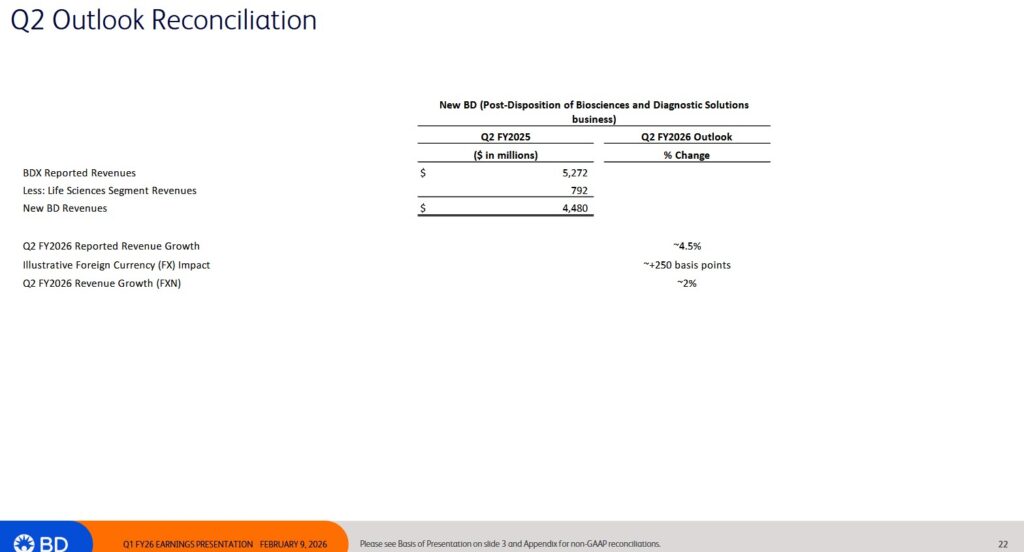

FY2026 Guidance

The following is BDX’s current and prior FY2026 guidance which includes deployment of the $4B cash distribution from the February 9, 2026 ‘WAT’ transaction.

Adjusted diluted EPS guidance reflects growth of ~6% at the $12.35 – $12.65 midpoint and includes an impact of 370 bps from tariffs.

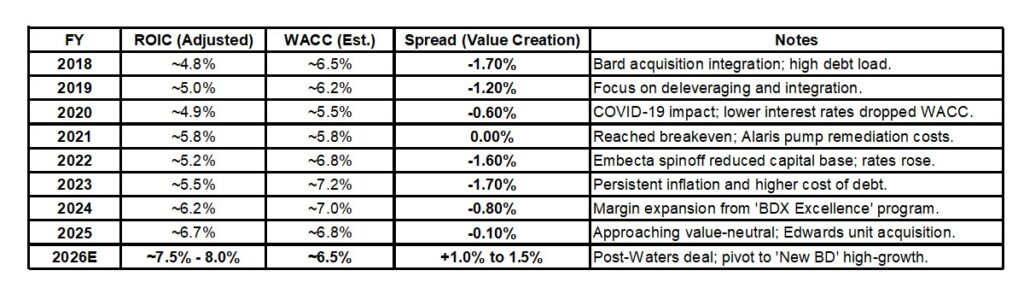

ROIC and WACC

Return on Invested Capital (ROIC) provides an indication of a company’s efficiency. In essence, is a company actually creating value or ‘burning’ cash for the sake of growth?

A company with a higher ROIC is mathematically worth more because it requires less reinvestment to achieve that growth.

A good indication of how well a company is performing is to compare ROIC to the Weighted Average Cost of Capital (WACC). WACC, however, is not a metric officially reported by BDX but it can be roughly estimated based on the company’s credit profile and market conditions.

The generally accepted high-level formula used by Wall Street is:

ROIC = NOPAT/Average Invested Capital

with the Net Operating Profit After Tax (NOPAT) formula being Operating Income (EBIT) x (1-tax rate)

This shows how much profit the core business makes while ignoring how much debt the company has.

The Average Invested Capital is the total money tied up in the business.

- The Operating Approach formula is

- The Financing Approach is

One shortcoming with ROIC is that it is a non-GAAP metric meaning the input data plugged into the ROIC formula is inconsistent.

The following is an approximation of BDX’s ROIC, WACC, and spread in FY2018 – YTD 2026.

In FY2018 – FY2021 the inclusion of significant goodwill and debt on BDX’s balance sheet from the C.R. Bard deal initially suppressed ROIC. During this time, BDX’s ROIC was often below its WACC, technically ‘destroying’ economic value as it integrated the business.

The spinoff of Embecta (Diabetes Care) in FY2022 was a targeted move to improve ROIC by removing a lower-growth, capital-intensive business. This initially caused a dip in absolute earnings but improved the long-term capital efficiency profile.

With the Biosciences and Diagnostics separation to WAT Corporation for $4B on February 9, 2026, at least $2B will go toward share buybacks which will reduce the equity base and should boost ROIC.

BDX’s WACC has fluctuated primarily due to interest rate environments. After the low-rate environment of 2020, the cost of debt rose significantly through 2023. BDX intends to apply $2B from the $4B received in February 2026 toward debt reduction. This should improve its WACC.

It now appears that BDX is in a position to start generating a consistent positive spread where its ROIC will exceed its WACC.

Risk Assessment

BDX’s net leverage ratio (Net Debt/Adjusted EBITDA) at FYE2021, FYE2022, FYE2023, and FYE2024 was 2.6x, 2.8x, 2.6x, and 3.0x. BDX’s target is under 3.0x. At the end of Q2 2025 is was 2.9x. The commitment is to deleverage to ~2.5x.

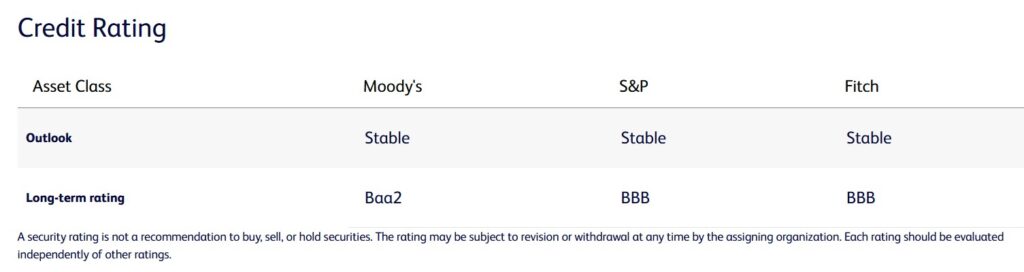

There are no changes to BDX’s domestic senior unsecured debt ratings from the time of my most recent prior posts.

All 3 ratings are the middle tier within the lower medium grade category. They define BDX as having an ADEQUATE capacity to meet its financial commitments. Adverse economic conditions or changing circumstances, however, are more likely to lead to a weakened capacity for BDX to meet its financial commitments.

These ratings are satisfactory for my purposes.

Dividend and Dividend Yield

BDX’s dividend history is accessible here.

BDX is somewhat trapped because with 54 consecutive years of dividend increases, its shareholder base EXPECTS dividend increases. If BDX were to re-prioritize its capital allocation and to lower the importance of dividend increases, the shareholder base will most likely revolt. Any dividend cut/freeze would most likely lead to a drop in BDX’s share price.

BDX is essentially trapped in having to continually increase its annual dividend.

As per prior posts, a company’s dividend metrics are of little importance in my investment decision making process. My interest lies in the total potential investment return and whether the return is commensurate with the risk I am assuming.

BDX’s share repurchases over the years have been ‘all over the map’ as reflected in the table found within the Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX section of this post.

In addition to the issuance of shares as part of its various SBC programs, BDX has made several acquisitions (eg. Carefusion, C.R. Bard, Parata Systems, Edwards LifeSciences’ Critical Care) over the years. These acquisitions have been funded through the use of debt and the issuance of new shares. A history of BDX’s recent mergers and acquisitions is accessible here.

The years in which BDX repurchased no shares (or few shares) is because the priority was to reduce debt taken on for acquisition purposes.

The diluted average common shares outstanding (millions of shares) in FY2010 was 240.136. In FY2024, this had ballooned to 291.009 but in Q1 2026 this had been reduced to 285.845.

Guidance for the weighted average diluted shares outstanding in FY2026 is 282 (millions of shares). Using 285.845 at the beginning of the year and the 282 average for the year, the year end diluted shares outstanding should be

The difference between 285.845 and is 7.69. BDX intends use $2B of the $4B proceeds from the WAT transaction to repurchase shares. Divide $2B by 7.69 million shares and the purchase price is ~$260. We need to recognize, however, that BDX issues shares under under employee and other plans so I suspect management has used a lower share purchase price to arrive at its 282 weighted average diluted shares outstanding projection.

BDX expects to repurchase shares through an accelerated share repurchase program that is expected to be executed in Q2 2026. Given this, I WANT BDX’s share price to remain under pressure until such time as the ASR has been completed. If BDX can repurchase $2B shares at an average price of $210 (the current price is $207.39 as I compose this post), it can repurchase ~9.5 million shares or ~1.81 million shares more than 7.69 million.

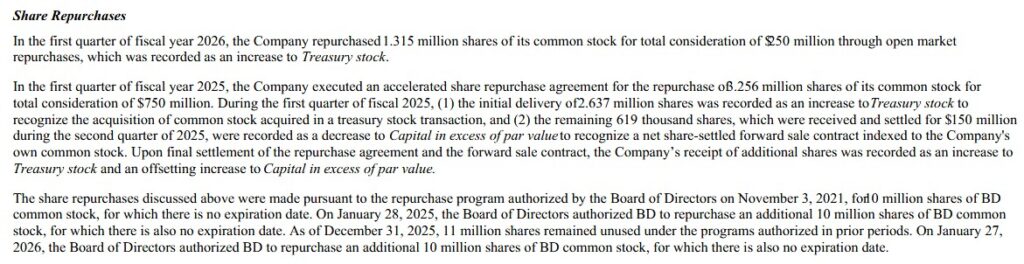

The following information about BDX’s share repurchases is extracted from the Q1 2026 Form 10-Q. BDX has sufficient Board authorization to repurchase the number of shares I estimate can be repurchased with $2B.

Valuation

In my February 7, 2025 post, I touch upon the significant variances between BDX’s GAAP and non-GAAP earnings for the past decade. The variances are primarily attributed to purchase accounting adjustments, restructuring costs, and integration costs. There may have been variances prior to BDX embarking on the path of major acquisitions (the first major acquisition post Financial Crisis was the 2015 acquisition of Carefusion) but nothing like in FY2015 – FY2024. In the past decade, BDX has reported significant earnings adjustments. At some point in time, investors begin to wonder whether these adjustments should really be considered ‘adjustments’ or whether there are really part of normal business operations.

Management’s FY2026 outlook is for $12.35 – $12.65 in adjusted diluted EPS. Using the February 9, 2026 $207.39 closing share price, the forward adjusted diluted PE range is ~16.4 – ~16.8.

Keeping in mind management’s FY2026 estimate, it is readily apparent that not all brokers have adjusted their estimates. I think even the low end of the current broker estimates are too high. Given that the WAT transaction closed on February 9 and not all brokers have adjusted their forward adjusted diluted EPS estimates, I recommend you do not rely on these current estimates.

- FY2026 – 14 brokers – mean of $14.42 and low/high of $12.80 – $14.97.

- FY2027 – 14 brokers – mean of $14.57 and low/high of $12.96 – $15.90.

- FY2028 – 7 brokers – mean of $15.54 and low/high of $14.03 – $16.87.

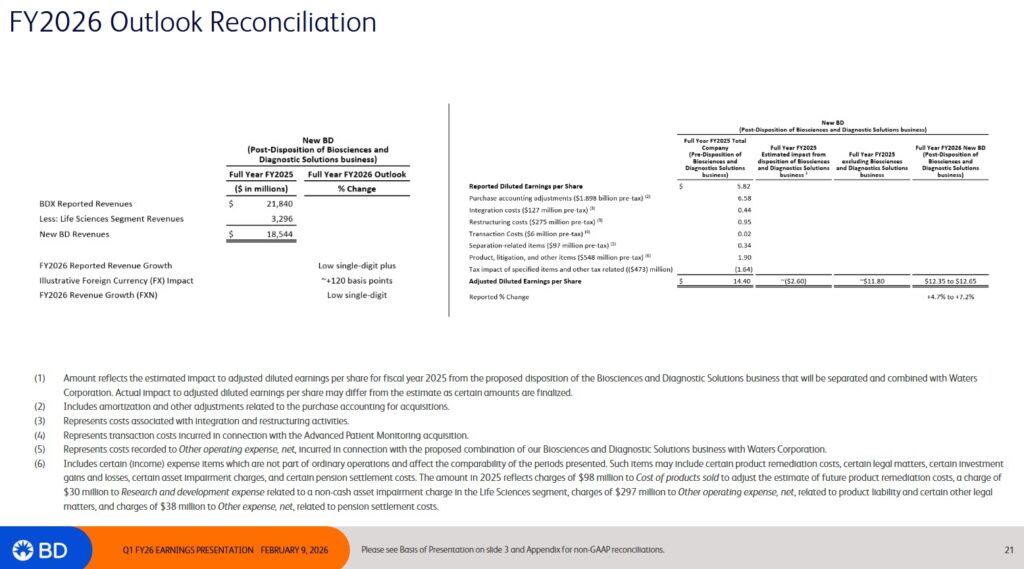

NOTE: In the February 5, 2025 BD Announces Intent to Separate Biosciences and Diagnostic Solutions Business presentation, we see that this business segment’s FY2024 revenue was ~$3.4B. A variety of earnings adjustments will accompany this transaction that will ‘muddy’ BDX’s financial results in FY2026. I am not, therefore, attempting to estimate the ‘New BDX’ valuation.

I will assess BDX’s valuation once the FY2026 results and FY2027 guidance become available. At the moment, there are just too many unknowns for me to determine what is BDX’s valuation.

Final Thoughts

BDX was my:

- 27th largest holding when I completed my 2023 Year End Review;

- 24th largest holding when I completed my 2024 Mid Year Review;

- 25th largest holding when I completed my 2024 Year End Review;

- 29th largest holding when I completed my 2025 Mid Year Review; and

- 28th largest holding when I completed my 2025 Year End Review.

BDX has certainly tested my patience over the last several years. Now that it has completed its transformation into a ‘pure-play’ medical technology company focused on its Medical Essentials, Connected Care, and Interventional segments can it finally close the ROIC-WACC gap?

BDX has much to do to regain my confidence but I am not about to give up on it now that management says the company has completed its transformation. Having said this, there are far too many unknowns at this point for me to determine BDX’s valuation (eg. how many shares will be repurchased, what debt will be repaid, etc.). BDX has destroyed shareholder value for several years and management needs to demonstrate that BDX’s ROIC can finally exceed its WACC.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long BDX.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.