At the time of my February 6, 2025 post, Blackstone (BX) had just released its Q4 and FY2024 results. The company’s outlook for FY2025 suggested it would be a year of robust results.

Looking at BX’s Press Releases, we see that it has been extremely active. Recently, BX announced that funds managed by BX and TPG have entered into a definitive agreement to acquire Hologic, Inc. in a transaction valued at up to $79/share, representing an enterprise value of up to $18.3B.

The nature of BX’s business is that it acquires companies and makes strategic investments to improve their value for subsequent spin-off/resale at a later date.

The last few quarters have been challenging from an ‘exit’ perspective but the tide has turned. BX’s leadership indicates there is a robust Initial Public Offering (IPO) pipeline being driven by improving market conditions and pent-up demand; it is currently one of the busiest IPO period since 2021.

In July 2025, for example, BX spun off a portion of its Cirsa (founded in Spain in 1985) stake via one of the largest IPOs in 2025 in Spain. This is a company BX acquired in 2018 for a ~€2.1 billion enterprise value. The original BX investment was backed by ~€1.5B in debt. Two years later, an additional loan of €400 million was taken to distribute a special dividend to BX.

Subsequent to the acquisition, Cirsa has invested around €1.2 billion in more than 130 acquisitions that include majority stakes in Apuesta Total in Peru (July 2024) and Casino Portugal (September 2024).

By going public, Cirsa’s plans are to accelerate its growth and to reduce its net debt.

From a BX perspective, the IPO brought its fund more than 2.5 times its invested equity. By retaining a stake in Cirsa, BX will benefit from Cirsa’s plans for further acquisitions over the next 3 years. There are ~100 takeover candidates located mainly in Spain and Latin America.

In addition, after a successful four-year holding period which saw Hotwire Communications expand its operations significantly, BX sold its stake to Brookfield Infrastructure Partners for ~$7B. This Q3 2025 exit marks BX’s full divestiture of the fiber internet provider after acquiring it in 2021.

In September 2025, BX completed the sale of a portion of its interest in a GP stakes portfolio held within its secondaries platform to generate liquidity. This sale was the largest single realization from the secondaries platform in Q3 and was part of the firm’s strategy to return capital to investors.

Business Overview

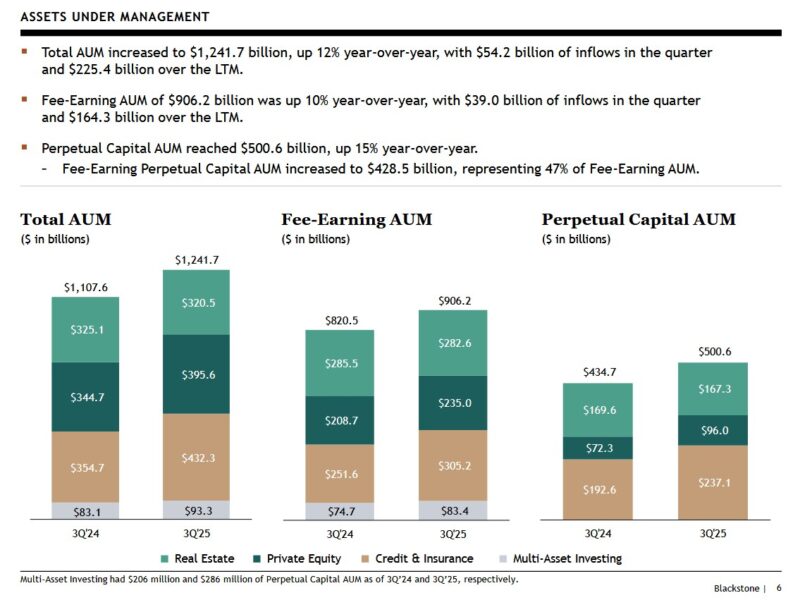

BX is one of the world’s leading managers of alternative assets. In recent years, it has rapidly grown its fee-earning assets under management (AUM). Its assets are relatively well balanced among private equity, real estate, hedge funds, and credit.

BX’s website and Part 1 of the FY2024 Form 10-K provide information to learn about the company. In addition, the ‘Our Businesses‘ section of BX’s website has a menu of the areas in which BX invests.

In this September 2025 presentation, BX’s President and Chief Operating Officer explores the forces driving growth and opportunities shaping the future of private equity, real estate, credit, infrastructure and more.

Private Credit Market – Misunderstandings and Misinformation

Recently, there has been significant focus on the implications of certain credit defaults in the market. On the Q3 2025 earnings call, BX’s CEO (Stephen Schwarzman) addresses this subject matter.

These events have been erroneously linked to the traditional private credit market as a result of misunderstandings and misinformation.

Importantly, the defaults and focus resulted from bank-led and bank syndicated credits, not private credit. Moreover, these situations are widely believed to involve the fraudulent pledging of the same collateral to multiple parties.

The traditional private credit model is characterized by direct origination in the context of a long-term hold strategy, with due diligence performed by sophisticated institutional managers and rigorously negotiated documentation.

For Blackstone, our $150B+ direct lending platform is comprised of over 95% senior secured debt, with low loan-to-value ratios of less than 50% on average, meaning there is significant borrower capital subordinate to our positions in nearly all cases from companies backed by financial sponsors or public companies.

And in the private investment-grade area, we’ve concentrated our activities in multitrillion-dollar markets where Blackstone is often a leading player, including data centers, energy infrastructure and real estate, with our loans secured by underlying assets of excellent quality.

While some asset managers may have ‘cockroaches’ in their portfolios, the asset management industry is highly fragmented and saturated. Some asset managers of lesser pedigree than BX may have serious problems with some of their investments. Furthermore, some asset managers are not in the business of ‘building’ the businesses they acquire. Their objective is to extract as much as possible from the acquired companies.

In ‘Plunder – Private Equity’s Plan to Pillage America’ by Brendan Ballou, there are several examples where private equity has decimated some companies while avoiding debt and liability for their actions. Some acquired companies have been forced to take on huge debts and pay extractive fees. In several instances, the companies purchased by private equity firms are left bankrupt or shells of their former selves.

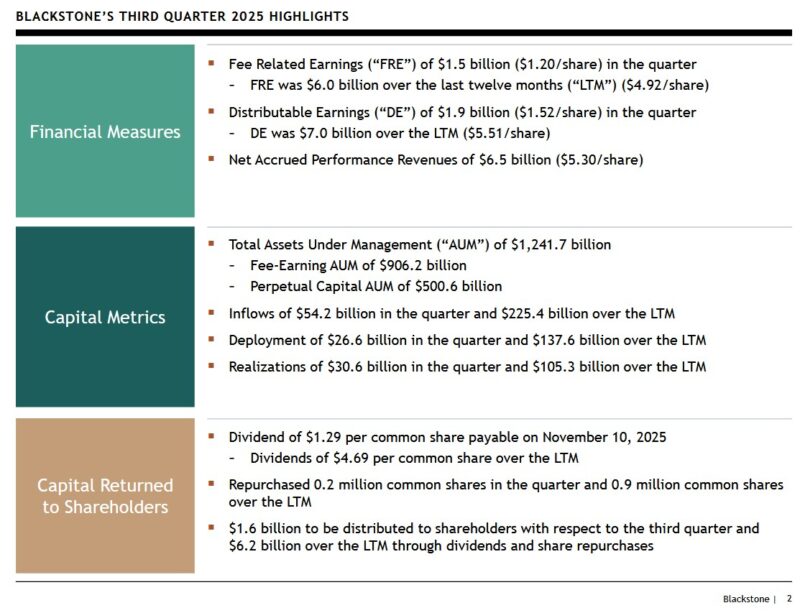

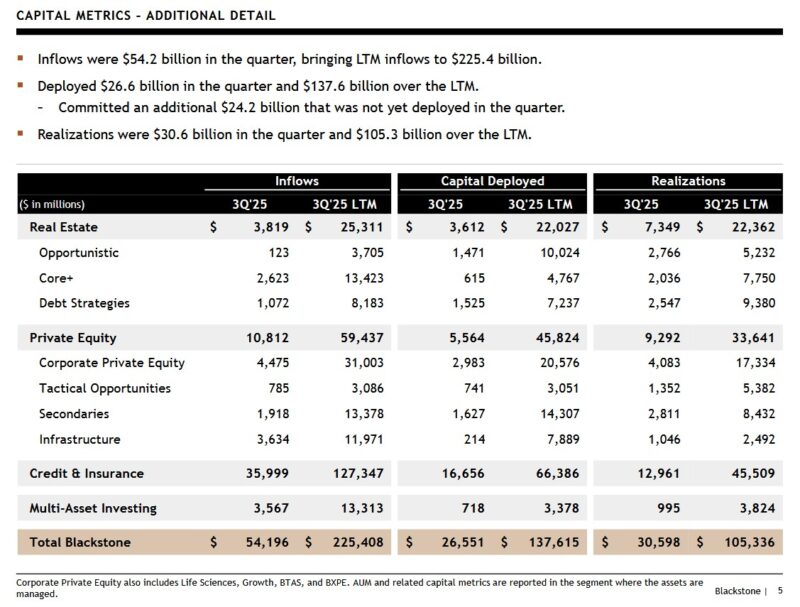

BX has its tentacles around so many companies that not every investment will be highly successful. If BX, however, did not have an enviable long-term track record it would not have reported Inflows of $54.2B in Q3 and $225.4B over the LTM.

Financials

Q3 and YTD2025 Results

I encourage you to listen to BX’s President and Chief Operating Officer discuss Q3 2025 results here and here.

The most recent results are accessible in the Press Release and Earnings Presentation and in the accompanying Supplemental Financial Data.

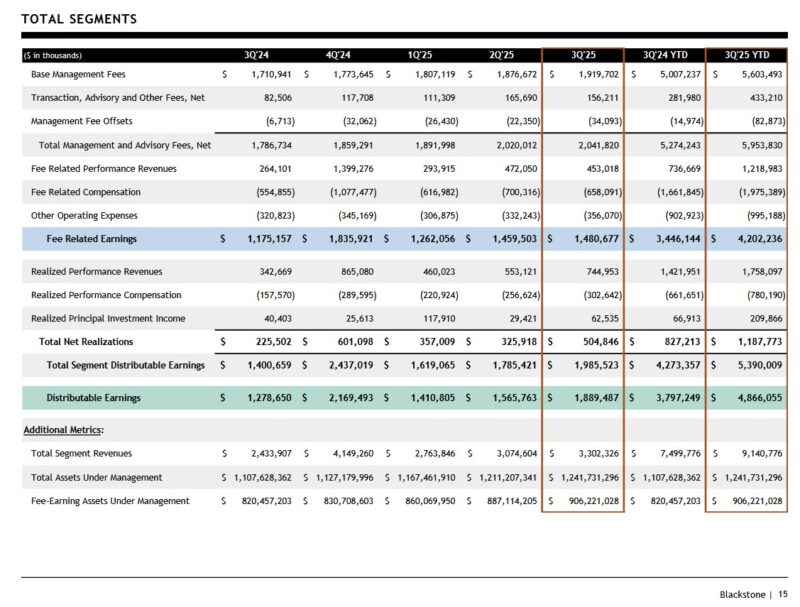

On the Q3 2025 earnings call, Michael Chae (CFO) states that Q3 2025 was one of the three best quarters of FRE in BX’s history.

FY2025 Outlook

BX does not provide specific details in its outlook. Michael Chae, however, provided the following on the Q3 2025 earnings call.

While we expect FRE margin in the fourth quarter to be sequentially lower due to seasonal expense factors, for the full year 2025, we are tracking favorably against the initial view of margins we provided in January.

Looking forward, in terms of fund dispositions, we have a robust pipeline of processes underway amid the improving transaction backdrop, and we believe we’re moving toward acceleration in 2026, the concentrated in private equity with expanding contribution from real estate over time. And the firm’s underlying realization potential is significant. The net accrued performance revenue on our balance sheet, our store value, stood at $6.5 billion at quarter end or $5.30 per share, while performance revenue eligible AUM in the ground has reached a record $611 billion.

Risk Assessment

BX’s senior unsecured domestic long-term debt ratings are at the top of the upper-medium-grade investment-grade tier. There is no change from prior reviews.

- S&P Global assigns an A+ long-term unsecured debt credit rating with a stable outlook; and

- Fitch assigns an A+ long-term unsecured debt credit rating with a stable outlook;

These ratings define BX as having a STRONG capacity to meet its financial commitments. It is, however, somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

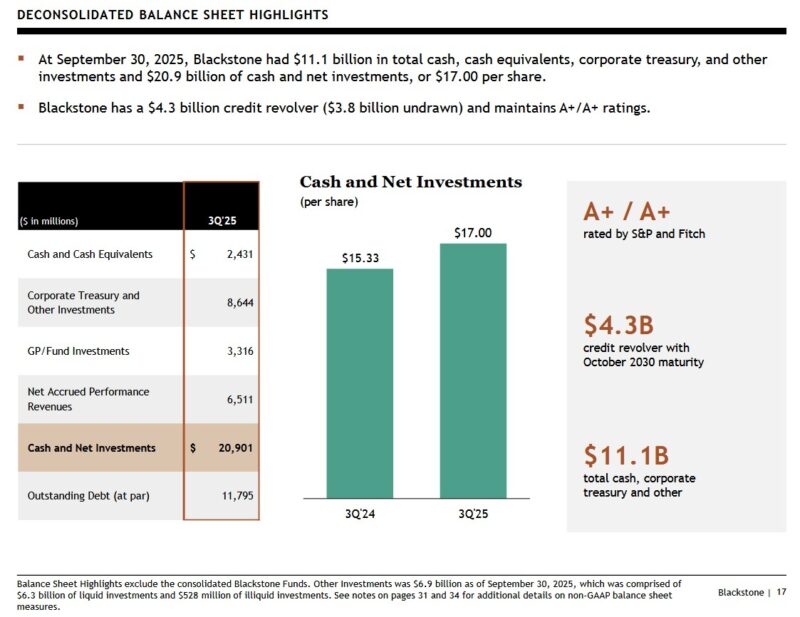

These are BX’s deconsolidated Balance Sheet highlights for Q3 2024 and Q3 2025.

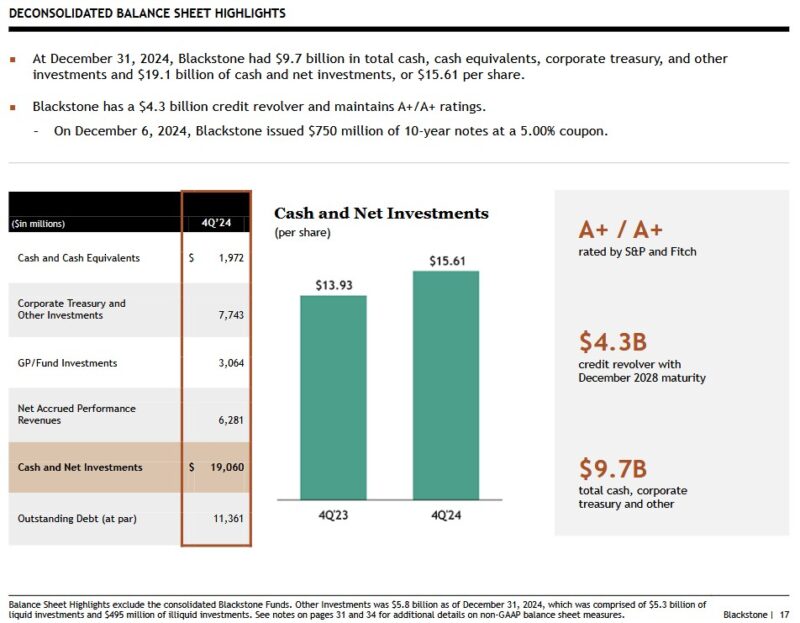

For comparison, I provide deconsolidated Balance Sheet highlights at FYE2023 and FYE2024.

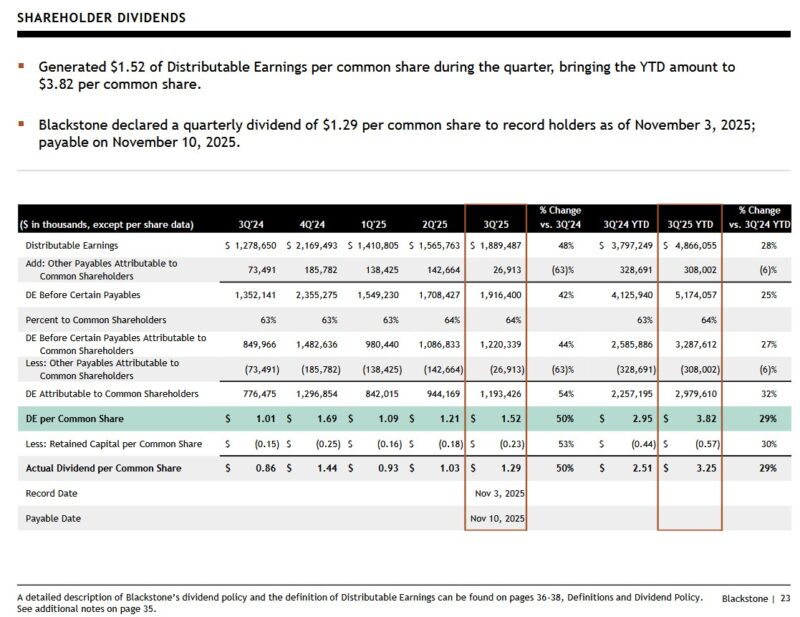

Dividends and Share Repurchases

Dividend and Dividend Yield

The next distribution of $1.29 is payable on November 10, 2025 on which I will incur a 15% dividend withholding tax. At a later date, BX will assign the component that is a qualified dividend and what is a return of capital.

Looking at the historical dividend distributions (see pdf documents), we see the allocation of prior distributions.

BX’s quarterly distributions are unconventional and fluctuate depending on DE. The distribution policy states:

‘We intend to pay to holders of common stock a quarterly dividend representing approximately 85% of The Blackstone Group Inc.’s share of Distributable Earnings, subject to adjustment by amounts determined by our board of directors to be necessary or appropriate to provide for the conduct of our business, to make appropriate investments in our business and funds, to comply with applicable law, any of our debt instruments or other agreements, or to provide for future cash requirements such as tax-related payments, clawback obligations and dividends to shareholders for any ensuing quarter. The dividend amount could also be adjusted upward in any one quarter.’

I do not calculate BX’s forward dividend yield because the quarterly dividend is unpredictable.

I look at an investment’s total potential long-term return perspective (capital gains and dividend income). Inconsistency in BX’s quarterly dividend, therefore, is irrelevant for my purposes.

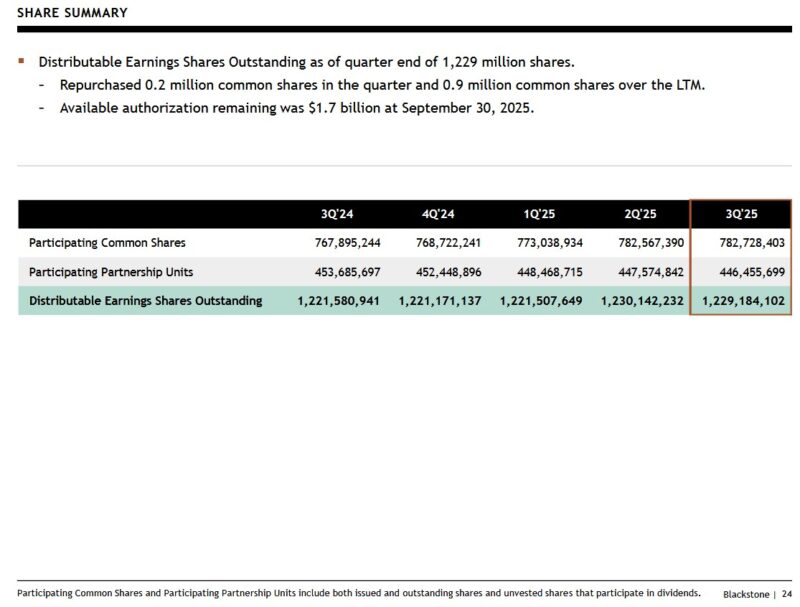

Share Repurchases

BX focuses heavily on optimizing its capital allocation. The extent to which it repurchases shares depends on whether there is a meaningful deterioration in BX’s share price relative to the true underlying value.

Valuation

I typically look at:

- diluted EPS – P/E;

- adjusted diluted EPS – adjusted P/E; and

- Free Cash Flow (FCF) – P/FCF

metrics to gauge the valuation of most companies I analyze. These metrics, however, are of little relevance when trying to assess BX’s performance and outlook.

BX uses DE and FRE to more accurately measure its performance. Definitions for these, and other terms, are within the FY2024 Form 10-K.

The very manner in which BX operates makes it virtually impossible to forecast these metrics. This explains why BX does not provide guidance.

BX is not easy to value because it raises large pools of capital from clients for deployment thus resulting in multiple multi-billion-dollar acquisitions annually. Because it continually makes sizable acquisitions or divestitures, earnings estimates can quickly become outdated.

Some of the assets are meant to be perpetual holdings. In other cases, BX uses its expertise to improve the performance of the companies in which it invests with the intent of monetizing these assets as part of its capital recycling programs. It is not, therefore, unusual to see wide swings in YoY GAAP results.

I expect fluctuations in quarterly FRE and DE. My interest, however, lies in the long-term trend of these two metrics. I, therefore, like to compare annual FRE and DE over several years.

When we compare BX’s DE and FRE for FYE 2017 and the most recent last 12 months, we see a noticeable increase over the years. At December 31, 2016, for example, BX had $366.6B of AUM. It now has ~$1.2417T! As AUM grows, it stands to reason that DE and FRE should also grow over the very long-term.

Naturally, DE and FRE will fluctuate depending on market/economic conditions. If conditions are not conducive to the immediate sale of certain assets, BX may elect to continue to manage the AUM until such time as conditions improve.

Final Thoughts

When I completed my 2025 Mid-Year Portfolio Review, BX was my 10th largest holding.

Subsequent to my my February 6, 2025 post, I published my April 3, 2025 post in which I disclose the purchase of 300 BX shares in a ‘Side’ account in the FFJ Portfolio @ ~$135.0146/share. In my October 17, 2025 post, I disclose the purchase of 100 shares @ $156.48 in a ‘Core’ account in the FFJ Portfolio.

On October 24, I acquired another 100 shares @ ~$155 in a ‘Core’ account bringing my total BX exposure to 1737 shares in a ‘Core’ account and 302 shares in a ‘Side’ account.

I automatically reinvest all net quarterly distributions (after the 15% withholding tax).

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long BX.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.