![]()

I last reviewed Blackstone (BX) in this October 25, 2025 post at which time it had released its Q3 and YTD2025 results on October 23. In that post I disclose the October 24 purchase of 100 shares @ ~$155 in a ‘Core’ account. This increased my BX exposure to 1737 shares in a ‘Core’ account and 302 shares in a ‘Side’ account.

BX was my 10th largest holding when I completed my 2025 Mid-Year Portfolio Review and my 8th largest holding when I completed my 2025 Year-End Investment Holdings Review.

By the end of 2025, my total BX exposure had risen to 1750 shares in a ‘Core’ account and 304 shares in a ‘Side’ account; the increase from my October 25th post is the result of the automatic reinvestment of quarterly distributions. The share price at the time of that year end review was ~$154.14 versus ~$142.42 on January 30 when this post is being composed.

On January 29, BX released its Q4 and FY2025 results thus prompting me to revisit this existing holding.

Business Overview

BX is one of the world’s leading alternative asset managers. In recent years, it has rapidly grown its fee-earning assets under management (AUM). Its assets are relatively well balanced among private equity, real estate, hedge funds, and credit.

BX’s website and Part 1 of the FY2024 Form 10-K provide information to learn about the company. In addition, the ‘Our Businesses‘ section of BX’s website has a menu of the areas in which BX invests.

In this September 2025 presentation, BX’s President and Chief Operating Officer explores the forces driving growth and opportunities shaping the future of private equity, real estate, credit, infrastructure and more.

Financials

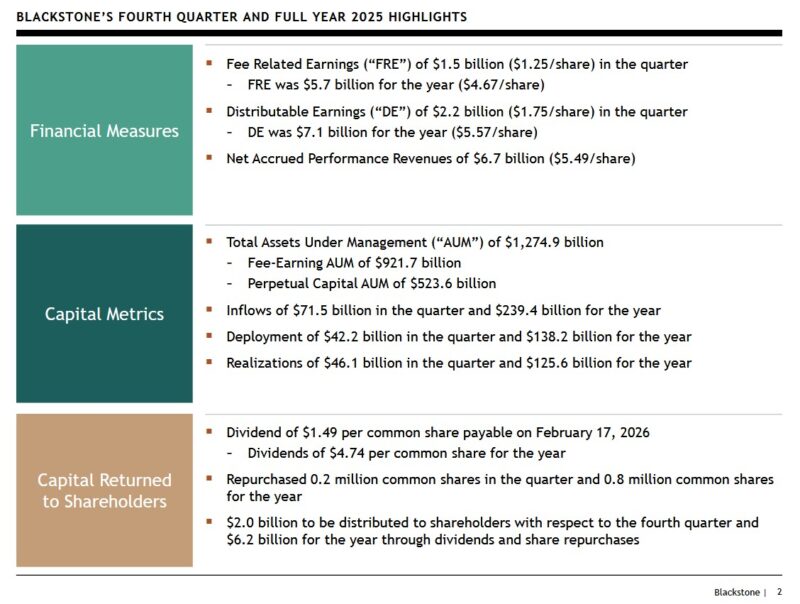

Q4 and FY2025 Results

Material related to BX’s Q4 and FY2025 earnings is accessible in the Press Release and Earnings Presentation and in the accompanying Supplemental Financial Data.

I encourage you to listen to BX’s President and Chief Operating Officer discuss Q4 2025 results here and here.

BX reported record results, highlighting strong earnings growth, fundraising strength, and positioning around AI, infrastructure, and private credit. On the Q4 earnings call management emphasized BX’s leadership in private wealth, citing recent analyst research indicating that BX has an estimated ~50% share of private-wealth revenue among major alternative firms.

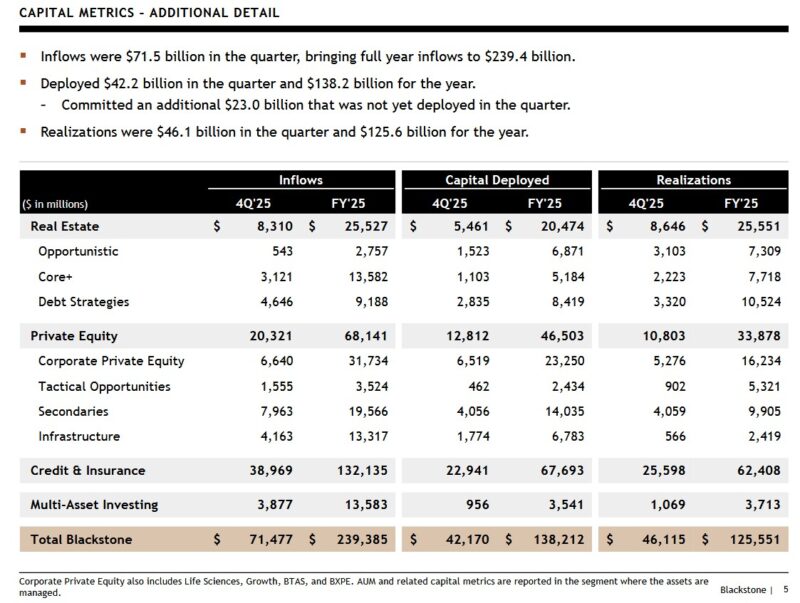

On the fundraising front, BX reported its highest inflows in over three years ($71.5B) in Q4 2025. This momentum typically takes 6 – 12 months to fully reflect in BX’s earnings report.

Proprietary data from more than 270 companies and nearly 13,000 real estate assets helped BX ‘see through the fog’ of macro uncertainty and lean into areas like digital infrastructure (data centers, power, electrification), private credit, life sciences, and regions such as India and Japan.

BX invested ~$138B in 2025, the highest in four years, including eight privatizations and an $18B med‑tech deal (Hologic).

The ongoing AI and power build‑out in semiconductors, data centers, and the grid is a major secular engine of US growth and a core opportunity set for BX’s strategies.

The deal and capital‑markets cycle is accelerating, with higher IPO and M&A activity and larger deal sizes.

Q4 global IPO issuance was up sharply YoY. BX highlighted the $7.2B Medline IPO as the largest sponsor‑backed IPO ever and a showcase of its private‑equity model.

Q4 2025 was one of the strongest quarters for realizations in years, with over $1B in gross performance revenues, helped by asset sales (e.g., energy, Las Vegas real estate, life sciences royalties) and year‑end crystallizations in Blackstone Multi-Asset Investing (BXMA) and credit vehicles.

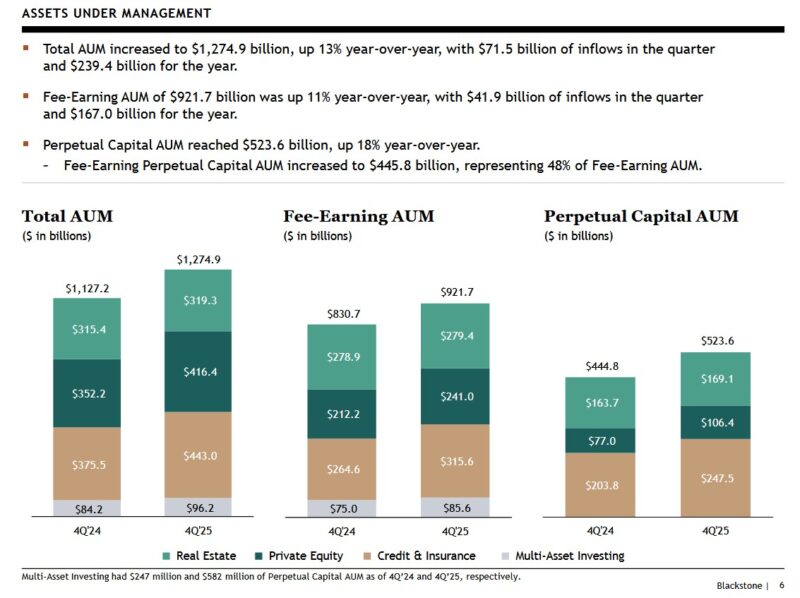

Institutional AUM represents over half of BX’s AUM and inflows. This is experiencing strong demand across infrastructure, multi‑asset (BXMA), secondaries, corporate private equity (including a larger Asia flagship and energy transition PE), and opportunistic credit.

BX’s credit platform reached ~$520B of AUM, with over $140B of 2025 inflows. Non‑investment‑grade private and real estate credit delivered double‑digit returns and long‑term outperformance versus public markets.

Investment‑grade private credit AUM grew to ~$130B, benefiting from very tight public investment grade spreads and heavy demand from insurers and other institutions for higher‑spread private deals tied to AI‑related infrastructure.

Insurance AUM grew 18% to ~$271B without BX taking insurance liabilities, and private‑wealth AUM rose 16% to over $300B, with strong sales into BX’s various product offerings.

Management believes US private real estate bottomed roughly two years ago and is slowly recovering, though values remain well below pre‑rate‑hike peaks.

BX has invested or committed over $50B in real estate since the trough, focusing on sectors like logistics, multifamily, grocery‑anchored retail, and data centers, and noted improving fundamentals such as lower construction starts and stronger leasing.

FY2026 Outlook

FY2026 Outlook

BX does not provide specific details in its outlook. On the earnings call, however, management states that it has growing client commitments and nearly $200B of dry powder. As BX deploys this dry powder, it activates new management fees.

Its ‘capital‑light, brand‑heavy’ model bodes well in what management views to be a more ‘business friendly’ business environment. Cooling inflation and central bank pivots are driving a rebound in deal activity. Lower rates make it easier for BX to sell older investments at a profit, which triggers ‘Realized Performance Revenues’.

Risk Assessment

BX’s senior unsecured domestic long-term debt ratings are at the top of the upper-medium-grade investment-grade tier. There is no change from prior reviews.

- S&P Global assigns an A+ long-term unsecured debt credit rating with a stable outlook; and

- Fitch assigns an A+ long-term unsecured debt credit rating with a stable outlook;

These ratings define BX as having a STRONG capacity to meet its financial commitments. It is, however, somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

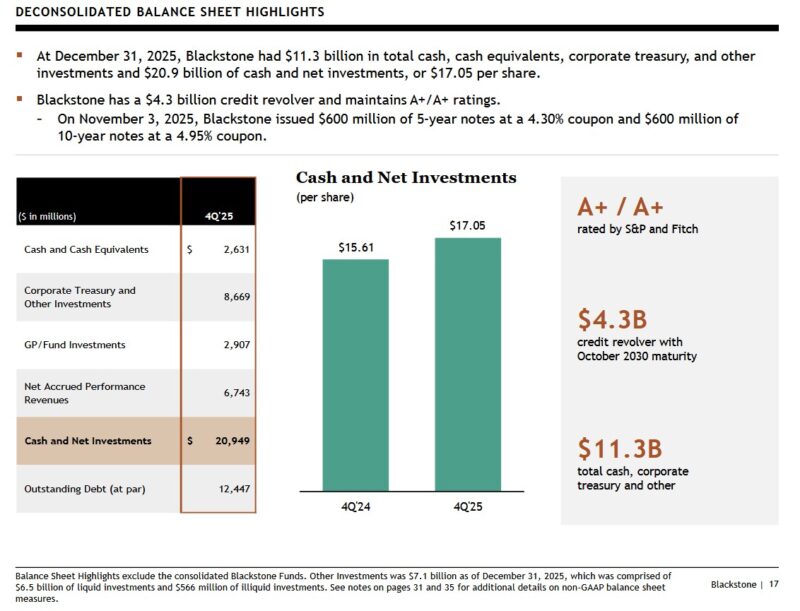

These are BX’s deconsolidated Balance Sheet highlights for Q4 2024 and Q4 2025.

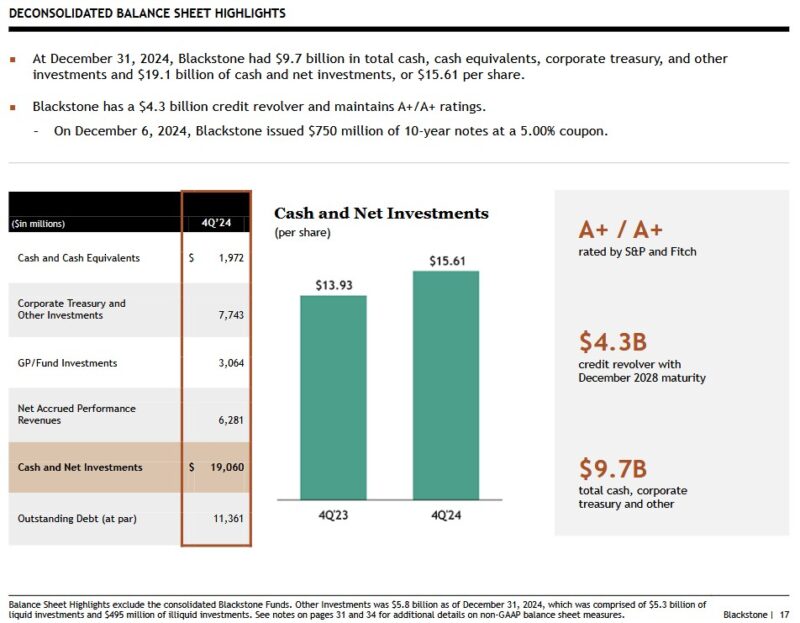

For comparison, I provide deconsolidated Balance Sheet highlights at FYE2023 and FYE2024.

Dividends and Share Repurchases

Dividend and Dividend Yield

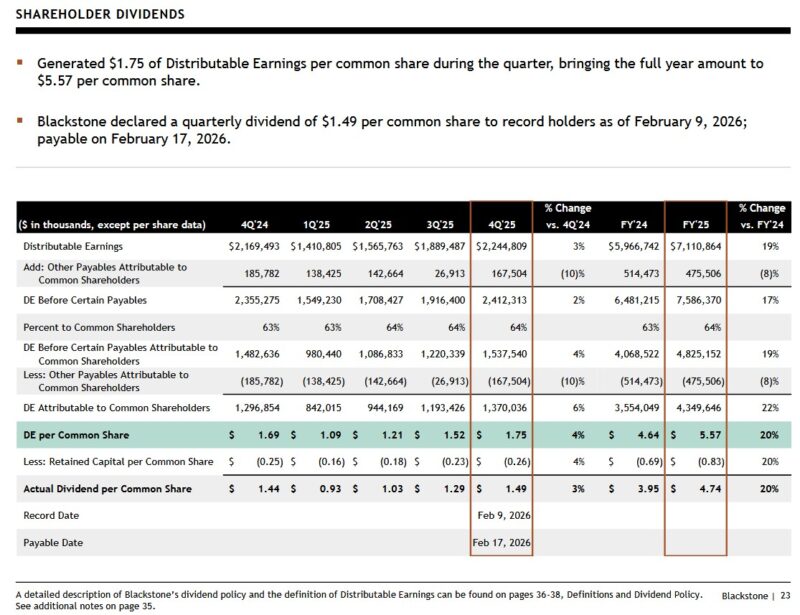

BX declared a quarterly dividend of $1.49/share to record holders as of February 9, 2026 payable on February 17, 2026.

BX’s quarterly distributions typically include a return of capital component. For example, the distribution of $1.29/share paid on November 10, 2025 consisted of a $0.705 qualified dividend and a $0.585 return of capital. Both are treated differently from a tax perspective if shares are held in taxable accounts. The 15% dividend withholding tax Canadian residents incur on dividend income is only applicable to the qualified dividend component of the quarterly distribution.

BX’s quarterly distributions are unconventional and fluctuate depending on DE. The distribution policy states:

‘We intend to pay to holders of common stock a quarterly dividend representing approximately 85% of The Blackstone Group Inc.’s share of Distributable Earnings, subject to adjustment by amounts determined by our board of directors to be necessary or appropriate to provide for the conduct of our business, to make appropriate investments in our business and funds, to comply with applicable law, any of our debt instruments or other agreements, or to provide for future cash requirements such as tax-related payments, clawback obligations and dividends to shareholders for any ensuing quarter. The dividend amount could also be adjusted upward in any one quarter.’

I do not calculate BX’s forward dividend yield because the quarterly dividend is unpredictable.

I look at an investment’s total potential long-term return perspective (capital gains and dividend income). Inconsistency in BX’s quarterly dividend, therefore, is irrelevant for my purposes.

Share Repurchases

BX focuses heavily on optimizing its capital allocation. The extent to which it repurchases shares depends on whether there is a meaningful deterioration in BX’s share price relative to the true underlying value.

Valuation

I typically look at:

- diluted EPS – P/E;

- adjusted diluted EPS – adjusted P/E;

- Free Cash Flow (FCF) – P/FCF;

- Return on Invested Capital (ROIC); and

- WACC (Weighted Average Cost of Capital)

metrics to gauge the valuation of most companies I analyze. These metrics apply to ‘traditional’ companies but are often meaningless or even misleading for alternative asset managers.

ROIC usually measures the company’s own balance sheet. In the case of BX, its balance sheet is tiny compared to the assets it actually controls.

BX doesn’t care if its corporate WACC is a specific percentage. Its focus is on achieving rates of return that beat benchmarks. If BX can exceed the benchmarks, it generates Carried Interest (performance fees). The cost of debt is secondary to the performance of the underlying assets in its various portfolios.

BX has ~$1.275T of AUM but most of this belongs to Limited Partners (pension funds, etc.). It raises large pools of capital from clients for deployment thus resulting in multiple multi-billion-dollar acquisitions annually. Because it continually makes sizable acquisitions or divestitures, earnings estimates can quickly become outdated.

Some of the assets are meant to be perpetual holdings. In other cases, BX uses its expertise to improve the performance of the companies in which it invests with the intent of monetizing these assets as part of its capital recycling programs. It is not, therefore, unusual to see wide swings in YoY GAAP results.

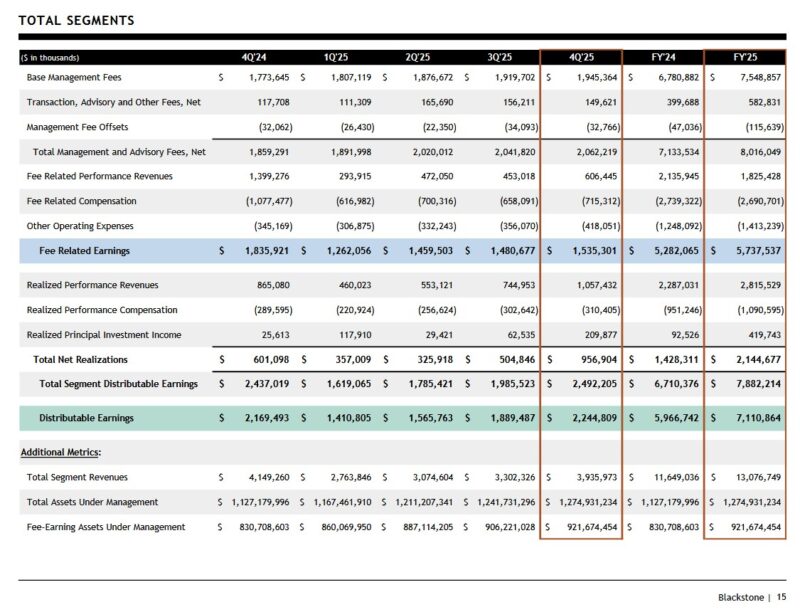

I expect fluctuations in quarterly FRE and DE. My interest, however, lies in the long-term trend of these two metrics. I, therefore, like to compare annual FRE and DE over several years. In my July 19, 2024 post, I reflect BX’s FRE and DE for FY2017 through Q2 2024.

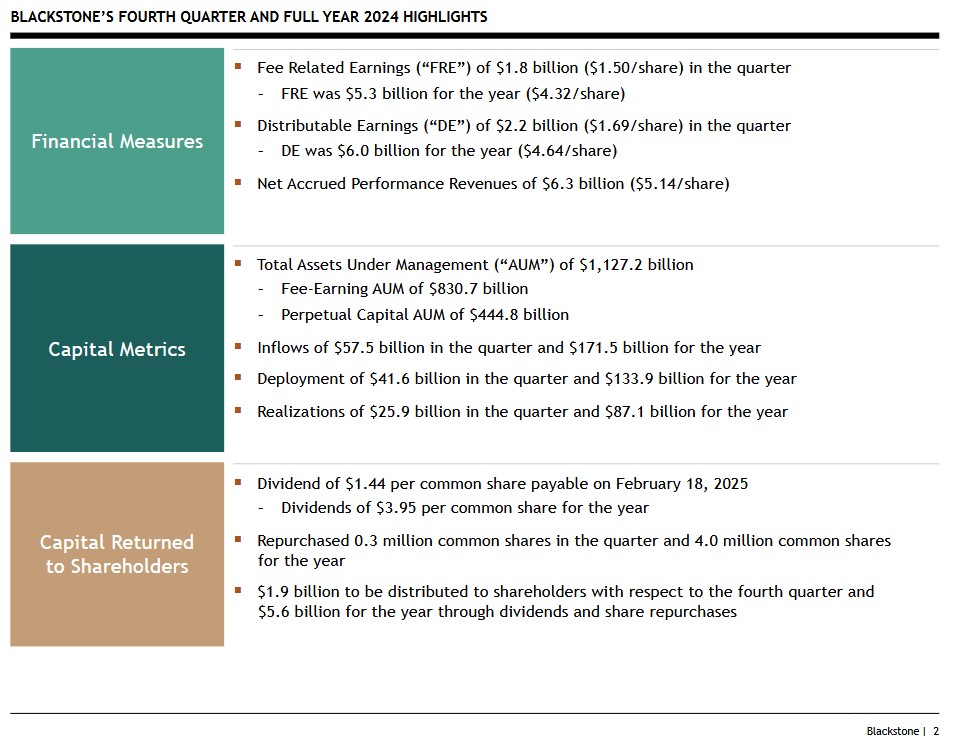

The following are BX’s metrics for FY2024 with the Q4 and FY2025 FRE and DE being reflected earlier in this post.

When we compare BX’s DE and FRE for FYE 2017 – FY2025, we see a noticeable increase over the years.

In addition to FRE and DE metrics I look at BX’s AUM. At December 31, 2016, BX had $366.6B of AUM. It now has ~$1.275T! As AUM grows, it stands to reason that DE and FRE have a reasonably strong probability of growing over the very long-term.

Naturally, DE and FRE will fluctuate depending on market/economic conditions. If conditions are not conducive to the immediate sale of certain assets, BX may elect to continue to manage the AUM until such time as conditions improve.

Finally, asset management is a talent-driven business. The ‘assets’ are people and intellectual property. These do not appear in the ‘Invested Capital’ denominator of the ROIC formula.

NOTE: The Q4 and FY2025 Press Release and Presentation includes 3 pages at the end that explain the definitions of the various relevant metrics the company uses to determine its performance.

Final Thoughts

A BX investment involves a unique set of risks that differ significantly from investing in a typical ‘blue chip’ stock or a standard index fund. BX makes its money by managing other people’s money in private equity, real estate, and credit and its performance is highly sensitive to the broader economy.

When investing in BX, an investor is not just ‘betting’ on the assets but is also betting on the management company.

As the private equity industry matures, there is constant pressure to lower management fees.

If institutional investors (like pension funds) feel over-exposed to private markets, BX may find it harder to raise new ‘dry powder’. Recent record inflows suggest this is not an issue.

BX’s business model is subject to interest rate sensitivity. It uses leverage to buy companies and real estate. If interest rates remain higher than expected or spike, the cost of maintaining these debts erodes profitability. Higher rates also typically lead to lower valuations for real estate and private companies. This can reduce the ‘carried interest’ (performance fees) BX earns when it sells assets.

BX is one of the largest owners of commercial real estate in the world. It has pivoted heavily toward ‘new economy’ real estate (data centers, warehouses, and student housing). Nevertheless, it still faces risks from the broader downturn in traditional office spaces and shifting retail trends.

There is also ongoing political debate and potential legislation regarding institutional ownership of single-family homes, which could impact BX’s residential portfolios.