In my October 16 Select Your Asset Manager Investment Wisely post, I state that there are some great firms in the highly fragmented asset management industry. One such industry participant is BlackRock (BLK) which I consider to be an asset manager investment for the long term.

At the end of Q3 2024, it had ~$11.5T of assets under management (AUM) after having grown ~$2.4T over the last 12 months. In this same time frame, clients entrusted BLK with $456B of net inflows, including a record $221B in Q3 2024.

On March 9, 2023, I initiated a BLK position in a ‘Core’ account within the FFJ Portfolio at ~$664/share. I added to my exposure in April and May 2023 @ ~$656 and ~$635 and again in April 2024 @ ~$770.

When I completed my 2024 Mid Year FFJ Portfolio Review, BLK was my 21st largest holding. It is now a top 20 holding.

In hindsight, I should have loaded up on BLK shares in early 2023. Instead, I now find myself holding only 160 BLK shares in the FFJ Portfolio.

Now that I have ample liquidity, I revisit BLK to determine if I should increase my exposure.

Overview

BLK is positioning itself as a single place for global clients to invest across public and private markets.

A comprehensive overview of BLK is provided in Part 1 Item 1 in BLK’s FY2023 Form 10-K which is accessible through the SEC Filings section of the company’s website. I also strongly recommend reviewing the company’s website.

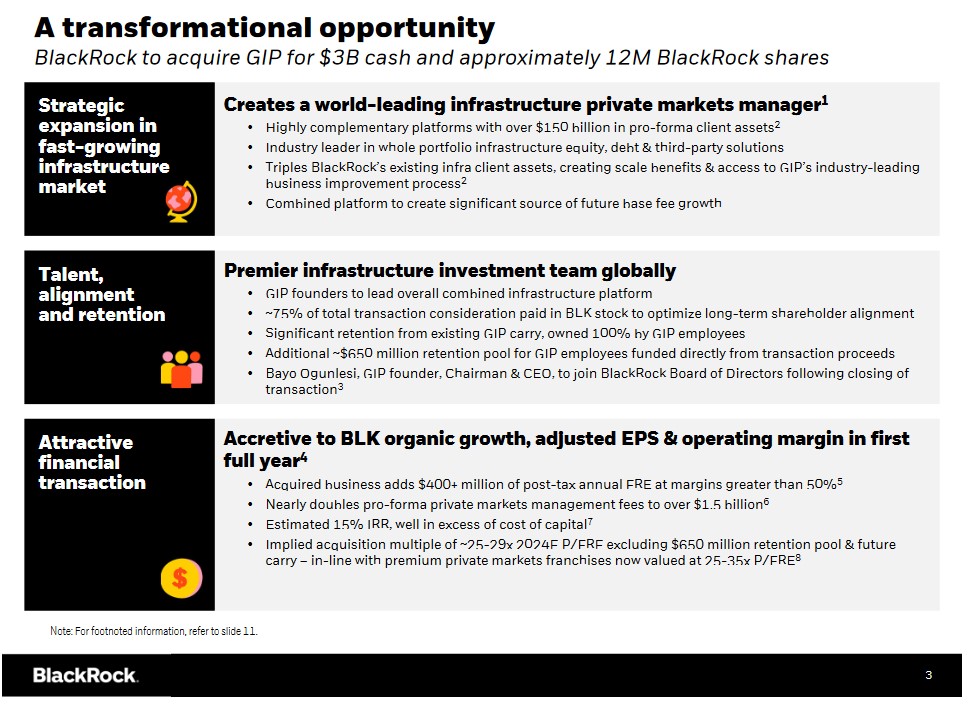

Global Infrastructure Partners (GIP) Acquisition

On January 12, BLK disclosed its intent to acquire GIP, a leading independent infrastructure fund manager for total consideration of $3B of cash and ~12 million BLK shares. Details are accessible here.

This acquisition adds ~$116B of private market assets to BLK’s business.

The successful completion of this acquisition was announced on October 1, 2024.

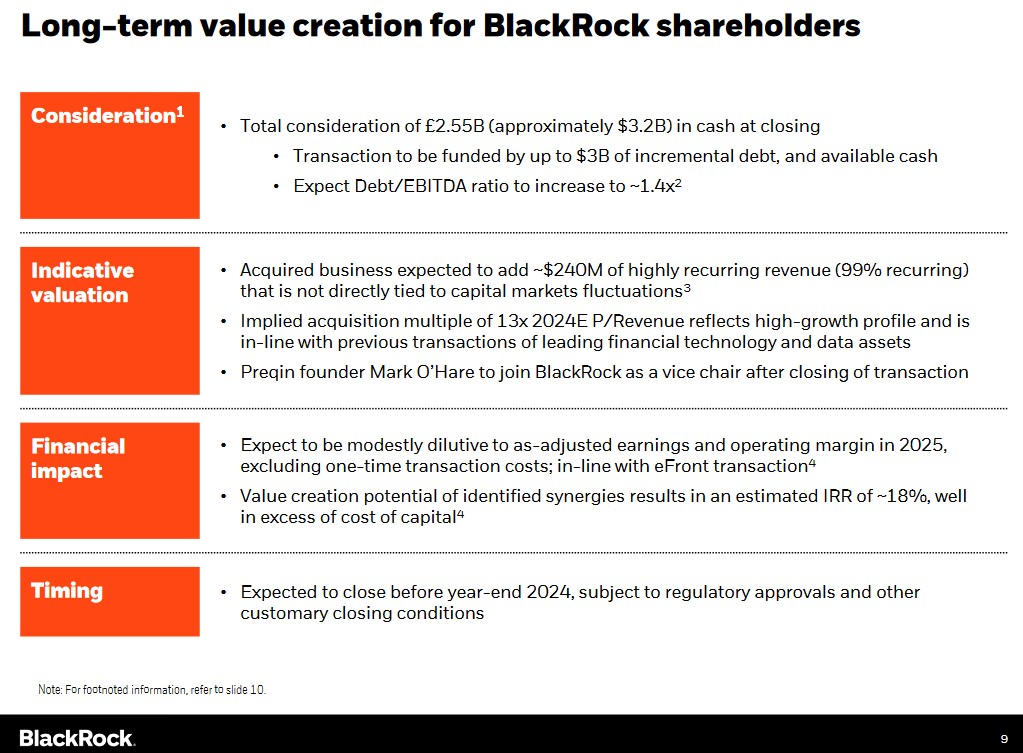

Preqin Acquisition

On June 30, BLK disclosed its intent to acquire Preqin, a leading independent provider of private markets data for £2.55B or ~$3.2B. Details of this acquisition are found here.

The proposed acquisition is an extension of BLK’s private markets capabilities and will be the launching point into the fast-growing private markets data segment; BLK expects the acquisition will accelerate the growth and revenue contribution of technology services.

The bigger longer-term opportunity is leveraging BLK’s engines in Aladdin and indexing with its capital markets expertise. It envisions that what the creation of public benchmarks did to drive stock markets (especially visible through iShares) can be replicated for private markets.

BLK Is Exploring Purchase Of Credit Firm HPS

BLK is seeking to position itself as a one-stop shop for a full range of investing options and has flagged private credit as one of its top growth priorities.

Despite the GIP and impending Preqin acquisitions, BLK lags smaller rivals (Apollo., Blackstone Inc., Ares Management Corp. and Blue Owl Capital Inc.) in the lucrative and growing world of private credit. BLK, therefore, has held discussions with HPS Investment Partners (HPS) about a potential acquisition by BLK.

HPS, founded in 2007, is among the largest independent managers in the $1.7T private-credit market. It managed $98B of assets in private credit and $19B in public credit at the end of June 2024.

If BLK were to acquire HPS, it would push it into the top ranks of the private-credit market. Despite these discussions, however, HPS is also pursuing a potential initial public offering that may value it at $10B+. These discussions, therefore, may not lead to an acquisition.

BLK and Jio Financial Services Ltd. Discussions

BLK is in discussions with Jio Financial Services Ltd. in its effort to tap the expanding direct lending opportunities in India. Should an agreement be reached, this would be BLK’s 3rd venture with the firm controlled by the richest Asian after both companies joined forces to start asset management and stock broker businesses in India; BLK and Jio received approval from India’s markets regulator to act as co-sponsors and set up a mutual fund business in the country in early October 2024.

The plan for this new 50-50 joint venture is to lend to businesses ranging from large companies to startups.

Financials

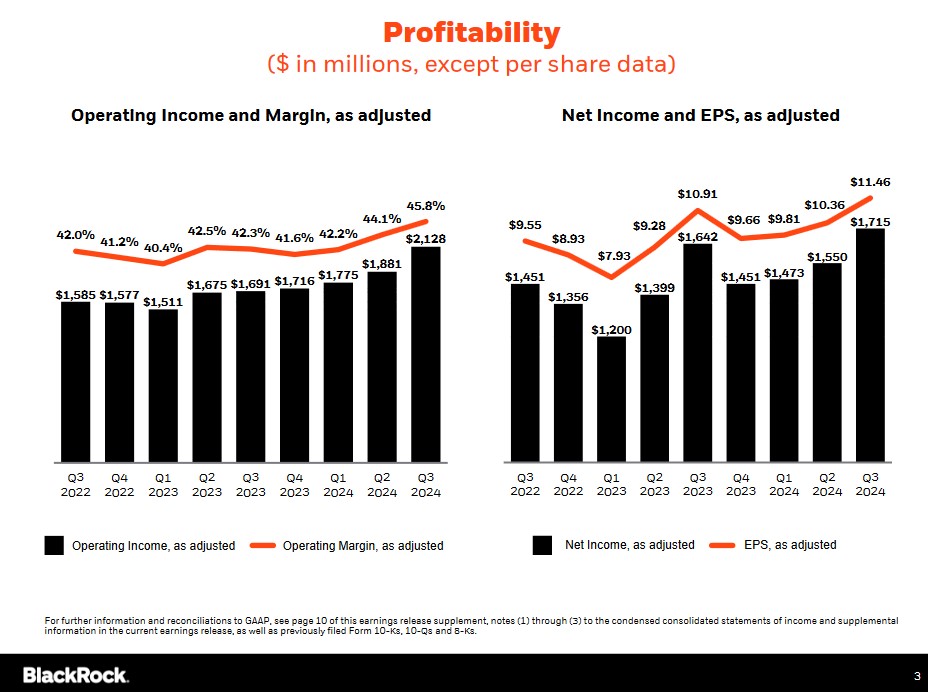

Q3 and YTD2024 Results

BLK’s Q3 and YTD2024 results are accessible here.

Source: BLK – Q3 2024 Earnings Release Supplement

Source: BLK – Q3 2024 Earnings Release Supplement

Capital Allocation

BLK’s capital management priorities are to:

- invest in the business to either scale strategic growth initiatives or drive operational efficiency;

- return excess cash to shareholders through a combination of dividends and share repurchases; and

- make inorganic investments where there is an opportunity to accelerate growth and support strategic initiatives.

FY2024 Outlook

BLK does not provide an outlook for the entire fiscal year. It does, however, state that it will either:

- continue to prioritize investments with differentiated organic growth potential; or

- that will expand operating leverage through enhanced scale.

In line with its January guidance and excluding the impact of GIP, Preqin and related transaction costs, BLK expects:

- its head count to be broadly flat in 2024; and

- a low to mid-single-digit percentage increase in 2024 core G&A expense.

BLK anticipates repurchasing at least $0.375B of shares in Q4. This is consistent with guidance provided in January.

Risk Assessment

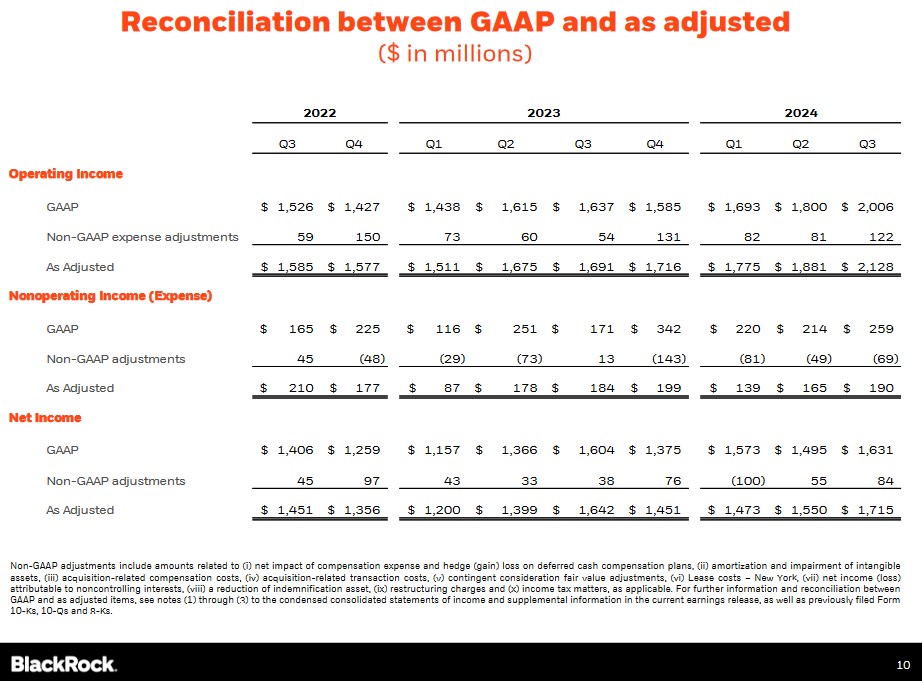

BLK’s Q3 2024 Form 10-Q is currently unavailable, and therefore, I provide the following note from BLK’s Q2 2024 Form 10-Q.

Source: BLK – Q2 2024 Form 10-Q

Moody’s has rated BLK’s domestic senior unsecured credit rating Aa3 since June 2018. The outlook is stable.

S&P Global has rated BLK’s domestic senior unsecured credit rating AA- since May 2014. The outlook is stable.

Both ratings are the bottom tier in the high-grade investment-grade category. These ratings define BLK as having a very strong capacity to meet its financial commitments. The ratings differ from the highest-rated obligors only to a small degree.

These investment-grade ratings are acceptable for my purposes.

Dividends and Share Repurchases

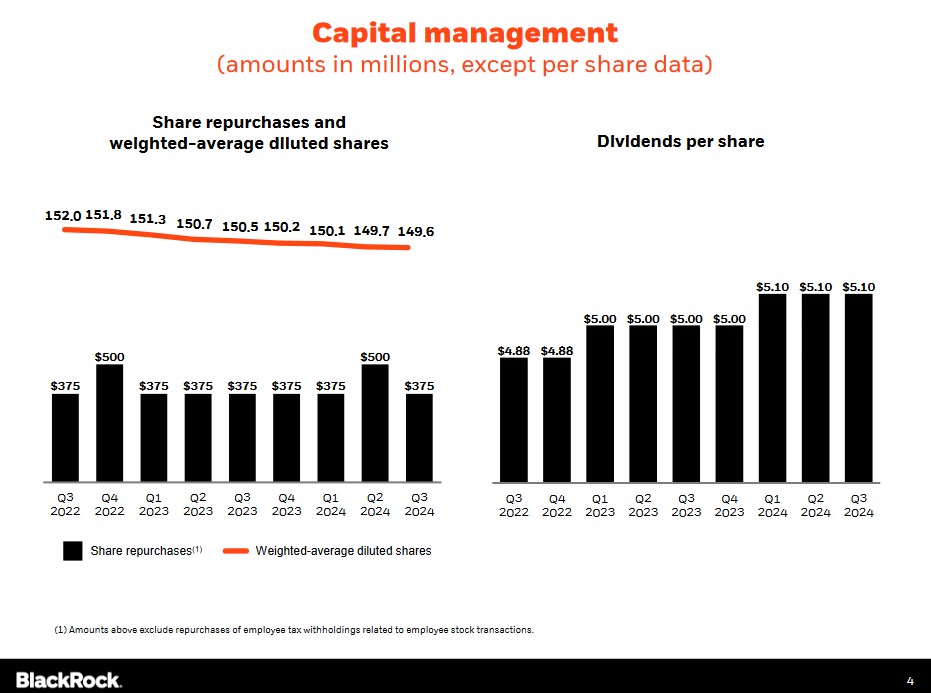

The following reflects the share repurchase and dividend distribution components of BLK’s quarterly capital allocation for the past 2 fiscal years.

Source: BLK – Q3 2024 Earnings Release Supplement

Dividend and Dividend Yield

BLK initiated a quarterly dividend in 2003 (see dividend history).

In mid November, we can expect BLK to declare its 4th consecutive $5.10 quarterly dividend for distribution in late December. I also expect BLK to increase its quarterly dividend in January by at least $0.10/share; I previously estimated a $0.05/share increase. Should this transpire, the next 4 dividend payments would total $20.70 (($5.20 x 3) + ($5.10 x 1)). Using the current ~$1015.75 share price, the forward dividend yield is ~2%.

Share Repurchases

BLK’s capital allocation priority is to invest either to scale strategic growth initiatives or drive operational efficiency. Once this is achieved, BLK returns excess cash to its shareholders through a combination of dividends and share repurchases.

In FY2014, the weighted average number of diluted outstanding shares was ~172 million. This has been reduced to ~149.6 million in Q3 2024.

In Q2, BLK repurchased $0.5B of common shares. This exceeded the planned run rate as BLK saw attractive relative valuation opportunities in its stock.

In Q3, BLK repurchased $0.375B of common shares – in line with the quarterly planned run rate.

Valuation

BLK’s FY2013 – FY2023 PE levels based on diluted EPS are 19.93, 18.57, 17.58, 20.08, 24.16, 11.30, 19.47, 24.07, 24.45, 19.60, and 34.84.

BLK’s valuation at the time of prior posts are accessible in my April 15, 2024 post. I, however, provide BLK’s forward adjusted diluted PE level when I purchased additional shares @ ~$770 on April 12 for ease of comparison.

- FY2024 – 15 brokers – mean of $41.28 and low/high of $39.41 – $43.90. Using the mean estimate: ~18.7.

- FY2025 – 15 brokers – mean of $46.57 and low/high of $42.95 – $51.15. Using the mean estimate: ~16.5.

- FY2026 – 7 brokers – mean of $52.39 and low/high of $44.62 – $56.64. Using the mean estimate: ~14.7.

In FY2023, BLK generated ~$3.821B of FCF and the weighted average diluted shares outstanding was ~150.7 million giving us ~$25.36 in FCF/share. Dividing my ~$770 purchase price by ~$25.36 and the P/FCF was ~30.36.

I last reviewed BLK in my July 16 post at which time shares were trading at ~$823. BLK’s valuations using this share price and current broker forward adjusted diluted EPS estimates were:

- FY2024 – 14 brokers – mean of $41.59 and low/high of $40.20 – $42.80. Using the mean estimate: ~19.8.

- FY2025 – 15 brokers – mean of $46.70 and low/high of $42.90 – $50.57. Using the mean estimate: ~17.6.

- FY2026 – 8 brokers – mean of $52.00 and low/high of $44.43 – $56.98. Using the mean estimate: ~15.9.

I anticipated revisions to existing analyst estimates but did not expect any meaningful changes.

BLK’s weighted average diluted shares outstanding in Q2 was 149.7 million. I envisioned the repurchase of $0.375B of its issued and outstanding shares in each of the next two quarters, thus leading me to estimate ~149.7 million as the weighted average diluted shares outstanding in FY2024.

BLK does not provide FCF guidance. Looking at the level of FCF generated in FY2017 – FY2023, however, I thought ~$3.8B of FCF in FY2024 was a reasonable assumption.

Dividing ~$3.8B by ~149.7 million shares, I arrived at ~$25.38 of FCF/share. Shares were trading at ~$823 thus resulting in a forward P/FCF of ~32.43.

Now, the following is BLK’s valuation using the current ~$1015.75 share price and current broker forward adjusted diluted EPS estimates:

- FY2024 – 13 brokers – mean of $43.28 and low/high of $42.70 – $44.90. Using the mean estimate: ~23.5.

- FY2025 – 15 brokers – mean of $49.19 and low/high of $43.85 – $54.97. Using the mean estimate: ~20.7.

- FY2026 – 11 brokers – mean of $54.76 and low/high of $47.20 – $59.87. Using the mean estimate: ~18.6.

It is likely that the weighted average diluted shares outstanding in FY2024 will be ~149.7 million (currently 149.8 million for the 9 months ending on September 30).

BLK does not provide FCF guidance. Looking at the level of FCF generated in FY2014 – FY2023 ($B rounded) (3.34, 3.33, 2.79, 3.83, 3.03, 3.24, 3.38, 3.95, 5.32, and 4.17), however, ~$4.4B of FCF in FY2024 is a reasonable assumption versus my $3.8B prior estimate.

Divide ~$4.4B by ~149.7 million shares gives us ~$29.4 of FCF/share. Using the current ~$1015.75 share price, the forward P/FCF is ~34.5.

Final Thoughts

My Final Thoughts are unchanged from those expressed in my July 16 post.

Every investor’s objectives and goals and circumstances requires a customized investment strategy. In some cases, the need for a consistent and reliable stream of dividend income is essential. This, however, is not my priority. My focus is on the potential long term total return of an investment. An attractive dividend yield is of little interest to me if the long term total investment return is likely to be in the low single digits.

Given this, I must pay attention to a company’s valuation. I, therefore,:

- try to acquire shares in wonderful companies if I perceive share price weakness to be temporary rather than because of a permanent impairment in the underlying business;

- hesitate to invest in a wonderful company if I think the company’s share price has become detached from the underlying fundamentals; and

- shy away from a company with an exceedingly attractive valuation under normal market conditions. Such companies are typically where your money ‘goes to die’.

Although I assess a company’s valuation, earnings can be manipulated or impacted by non-recurring items. I do, therefore, take much more into consideration in my investment decision making process.

BLK is already a formidable force and recent acquisitions/joint ventures (closed or in discussion) make it, in my opinion, an asset manager investment for the long term. My reluctance to immediately add to my exposure, however, lies is the firm’s current rich valuation.

BLK’s share price is volatile with the historical difference between the annual low/high share price often being significant. I remain hopeful that the share price will pullback from its current level at which time I hope to increase my exposure.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long BLK.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.