![]()

I like to invest in highly profitable undervalued/fairly valued growing companies that generate strong earnings and free cash flow. Companies with no debt (or exceptionally low debt levels) are particularly attractive.

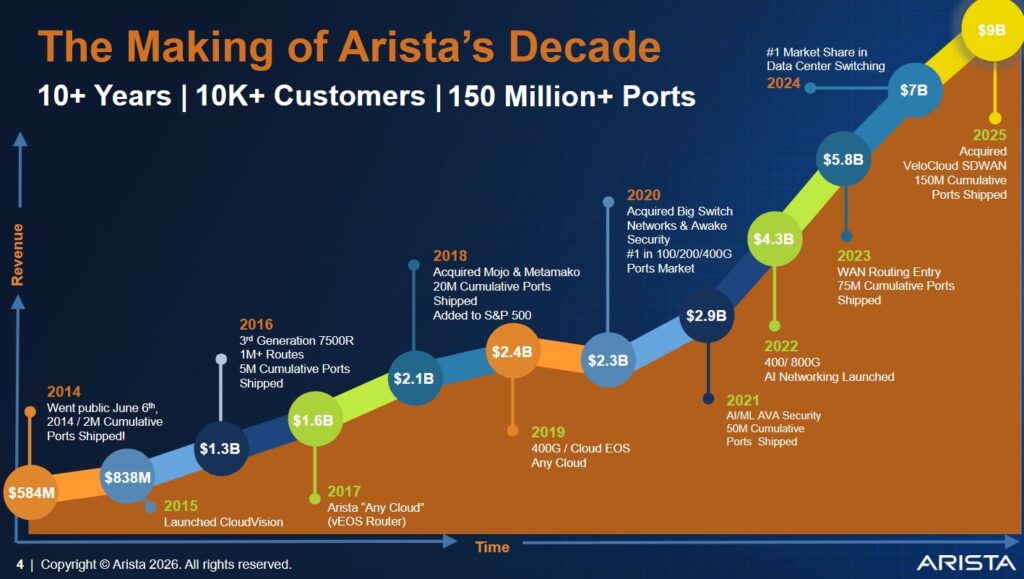

Following my December 2025 analysis of Arista Networks (ANET), I acquired 200 shares @ $127.505 on December 2, 2025 in one of the ‘Core’ accounts in the FFJ Portfolio.

This is an opportune time to revisit this holding given the February 12, 2026 release of Q4 and FY2025 results and FY2026 outlook.

Business Overview

My December 3, 2025 post includes a high level company overview.

The company’s website and in Part 1 Item 1 in the FY2024 Form 10-K accessible through the SEC Filings section of the company’s website are great sources of information.

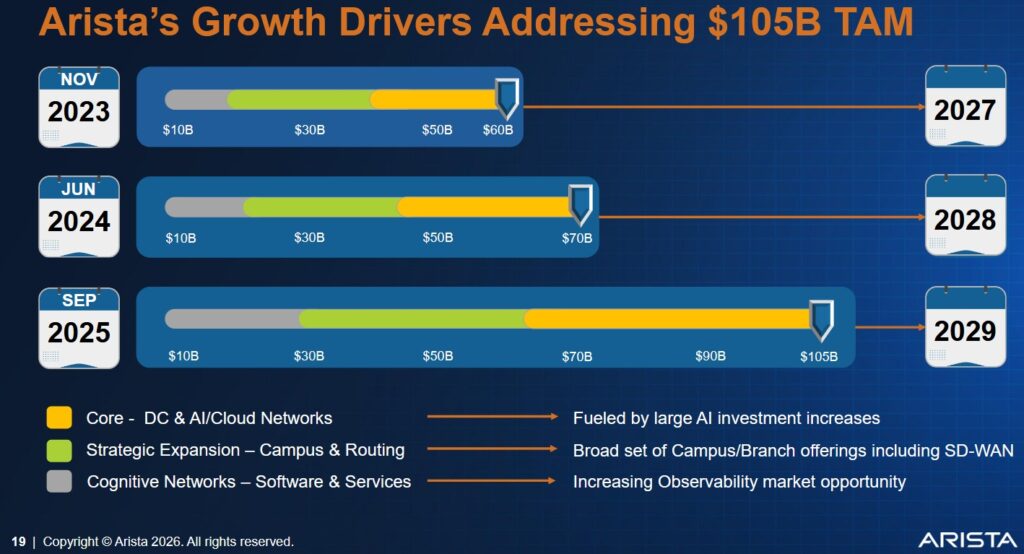

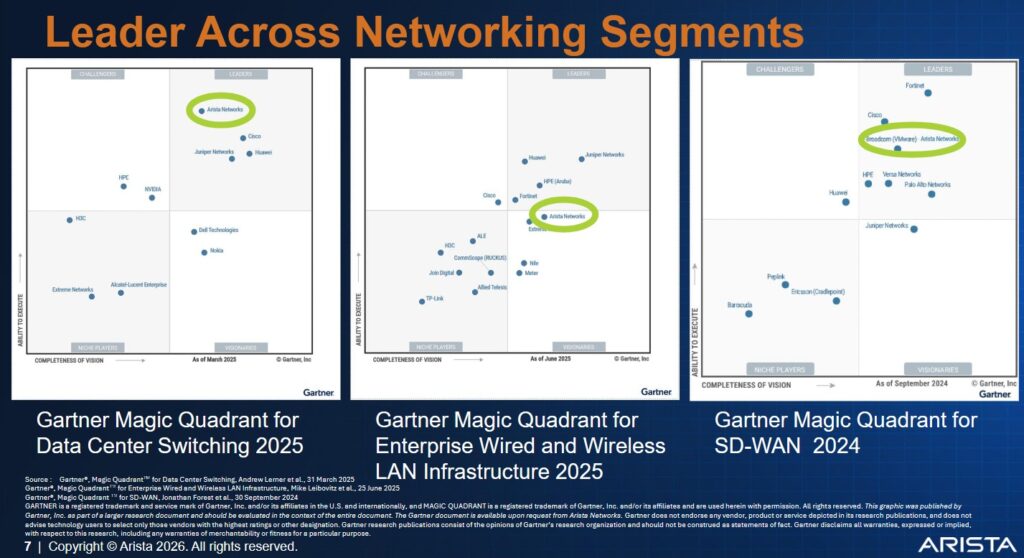

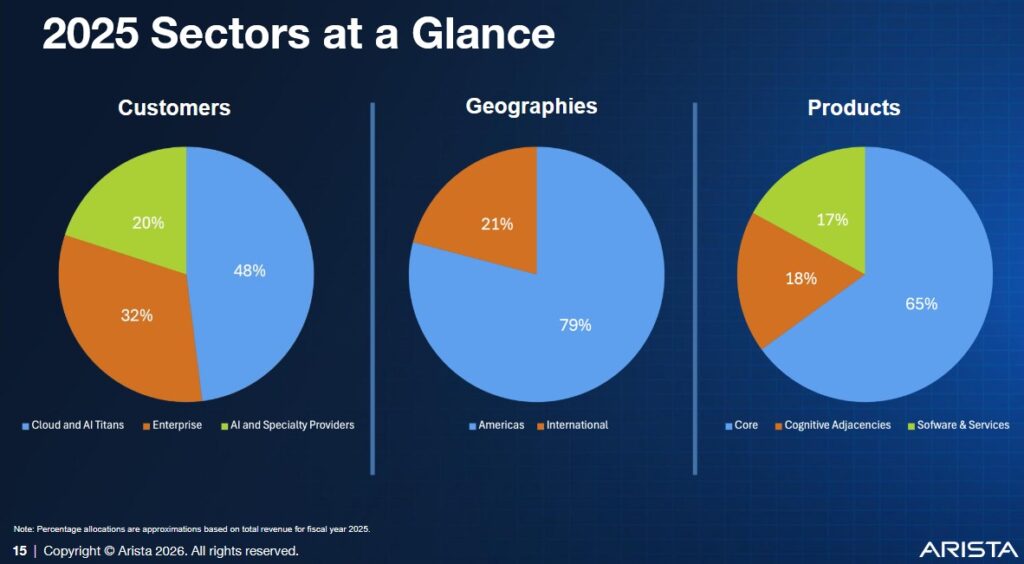

The February 2026 Investor Presentation from which the following are extracted is another excellent source of information.

Financials

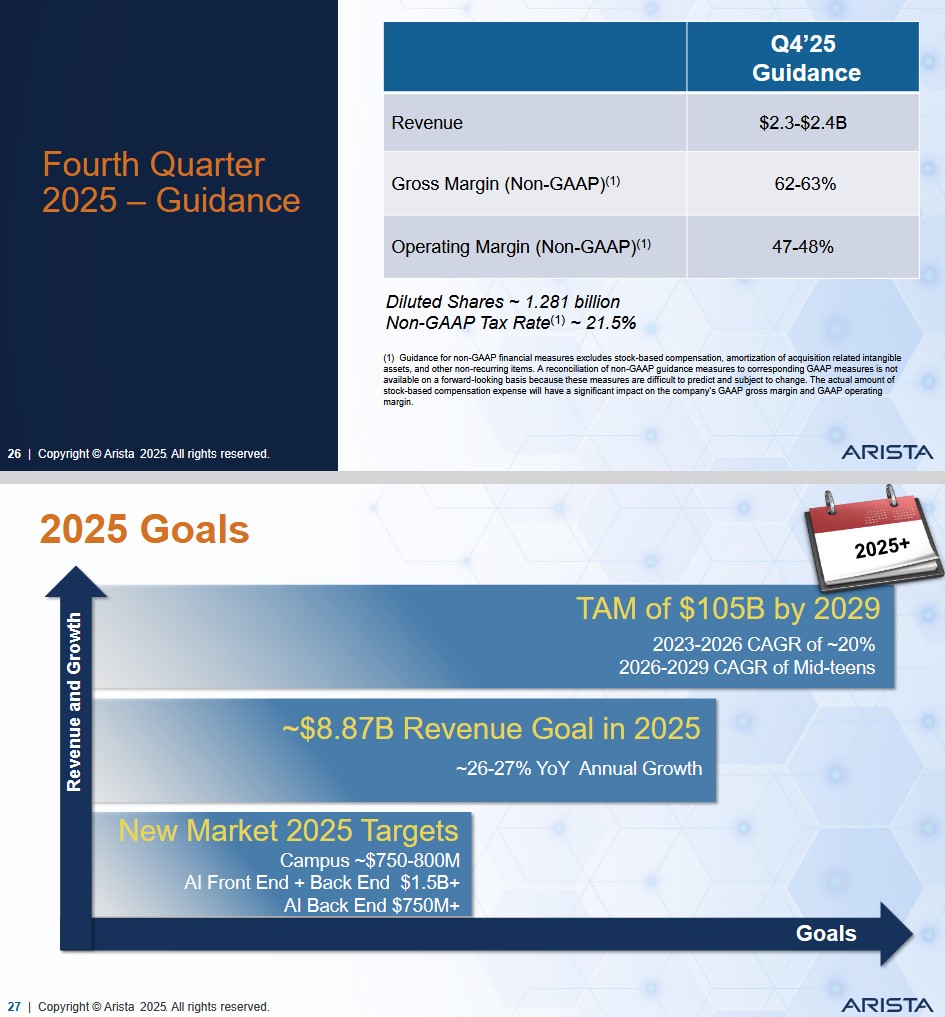

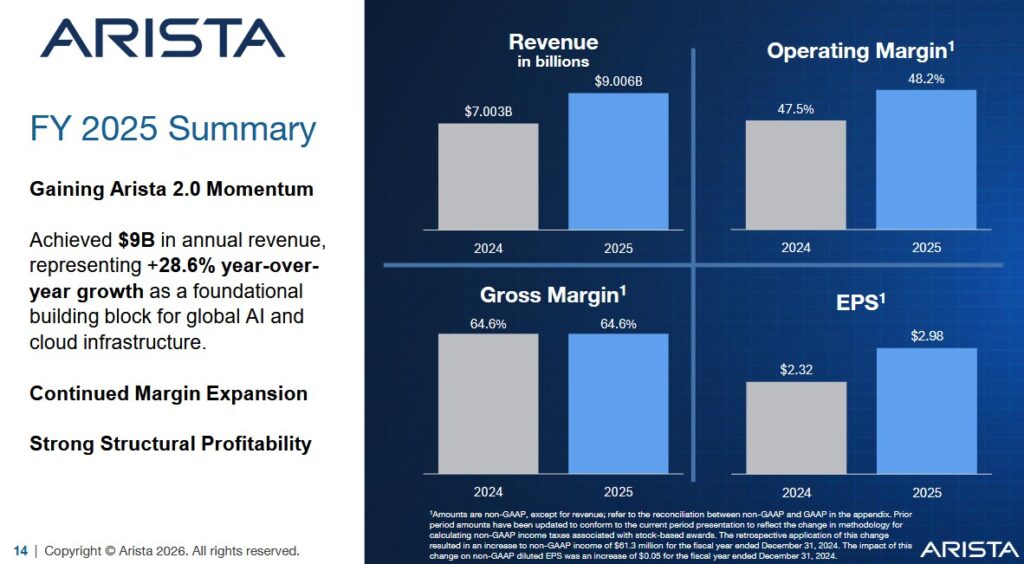

Q4 and FY2025 Results

At the time of my prior post, the following were ANET’s Q4 2025 guidance and FY2025 goals.

On February 12, 2026, ANET released its Q4 and FY2025 results.

- ANET’s $9.006B in revenue exceeded its ~$8.87B FY2025 revenue goal.

- Its Non-GAAP gross margin of 64.6% exceeded the 62% – 63% target.

- The 47.5% operating margin was in line with the 47% – 48% target.

- Diluted shares were to be ~1.281B. Actual diluted shares in FY2026 were 1.2757B.

At FYE2025 (December 31, 2025), ANET’s cash and cash equivalents and marketable securities was ~$10.743B versus ~$8.304B at FYE2024 (December 31, 2024).

Total liabilities at FYE2025 were ~$7.078B of which ~$4.003B was current deferred revenue and ~$1.370B was non-current deferred revenue. Deduct deferred revenue (funds received from customers prior to services being rendered) and liabilities amount to ~$1.705B.

At FYE2024, total liabilities were ~$4.049B of which ~$1.727B was current deferred revenue and ~$1.064B was non-current deferred revenue. Liabilities amount to ~$1.258B when we deduct deferred revenue.

Annual CAPEX is relatively low but developing products (research and development (R&D)) is expensive. In FY2019 – FY2025, ANET’s R&D expenses were ~$0.463B, ~$0.487B, ~$0.587B, ~$0.729B, ~$0.855B, ~$0.997B, and ~$1.237B. Furthermore, the investment in product development typically involves a long payback cycle. These investments may take several years to generate positive returns, if ever.

ANET expects to continue to invest heavily in software development to expand the capabilities of its cloud networking platform and to introduce new products and features. Results of operations will likely be impacted by the timing and size of these investments.

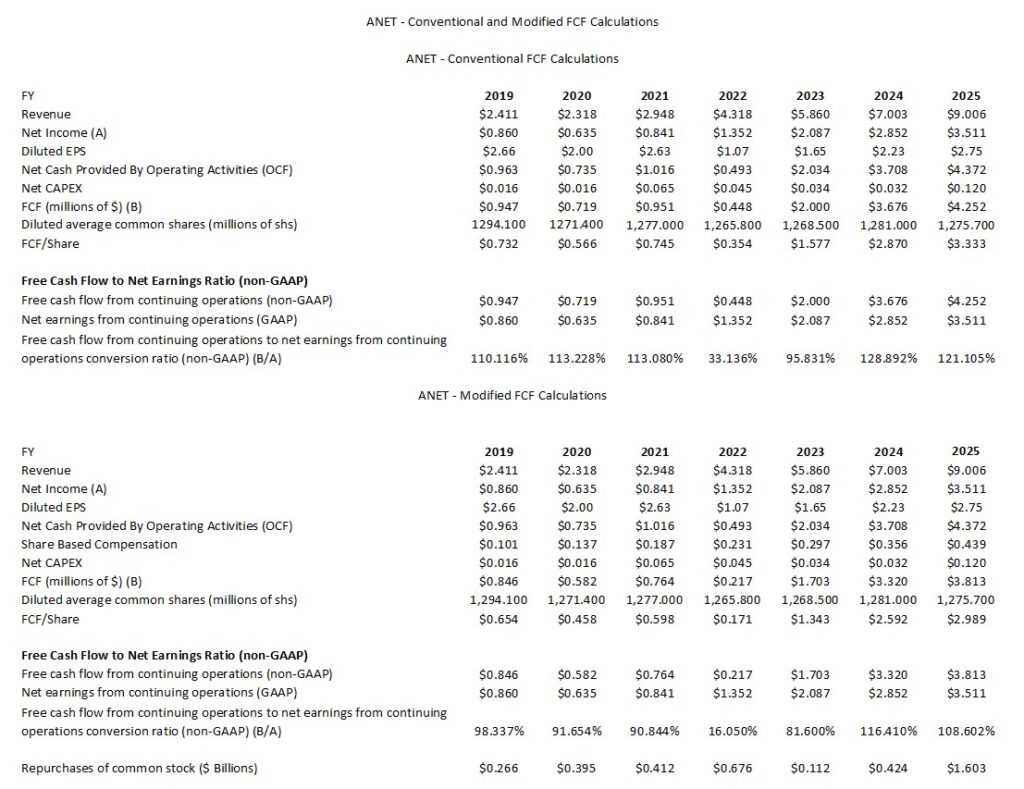

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX (FY2019 – FY2025)

In prior posts I touch upon my rationale for deducting stock-based compensation (SBC) to calculate FCF. I, therefore, dispense with explaining this again.

The following compares ANET’s FCF using the ‘conventional’ and ‘modified’ calculation methods.

Capital Allocation

During the Q4 2025 earnings call, ANET’s management outlined a capital allocation strategy focused on maintaining their operational model while fueling the aggressive 25% growth target for 2026. With over $10.7B in cash and marketable securities, it has significant ‘dry powder’.

ANET’s priorities for FY2026 fall into four main categories:

Aggressive R&D and ‘Co-Engineering’

The primary priority is organic growth through innovation and the company is shifting capital toward the 1.6T (Terabit) switching transition.

Significant capital is being allocated to the “Ethernet for Scale-Up” initiative and the development of AI rack systems.

Funding for software (EOS and NetDL) to improve AI workload performance, ensuring they remain the ‘standard’ for the back-end AI network.

Strategic M&A (The ‘VeloCloud’ Blueprint)

Management is looking for more ‘technology-tuck-ins’ following the July 2025 acquisition of VeloCloud from Broadcom. ANET is specifically looking for acquisitions in Network Identity, Cybersecurity, and Cognitive Campus technologies. The company is not interested in ‘distressed assets’ but rather high-quality technologies that can be integrated into the single-image EOS (Extensible Operating System) architecture.

Supply Chain Inventory and Purchase Commitments

Due to ongoing constraints in the High Bandwidth Memory (HBM) and advanced optics markets, ANET is using its cash to secure its future. It has increased its purchase commitments to ensure they can meet the $11.25 billion revenue goal for 2026. In addition, ANET is intentionally maintaining higher-than-normal inventory levels (~$2.25B at FYE2025) to insulate against potential supply shocks in the AI sector.

Opportunistic Buybacks

ANET continues to prefer share buybacks over dividends. Although there is no set schedule for buybacks, management’s policy is to opportunistically repurchase shares to offset dilution from stock-based compensation.

The company remains in a high-growth phase where reinvesting in the business yields the highest return.

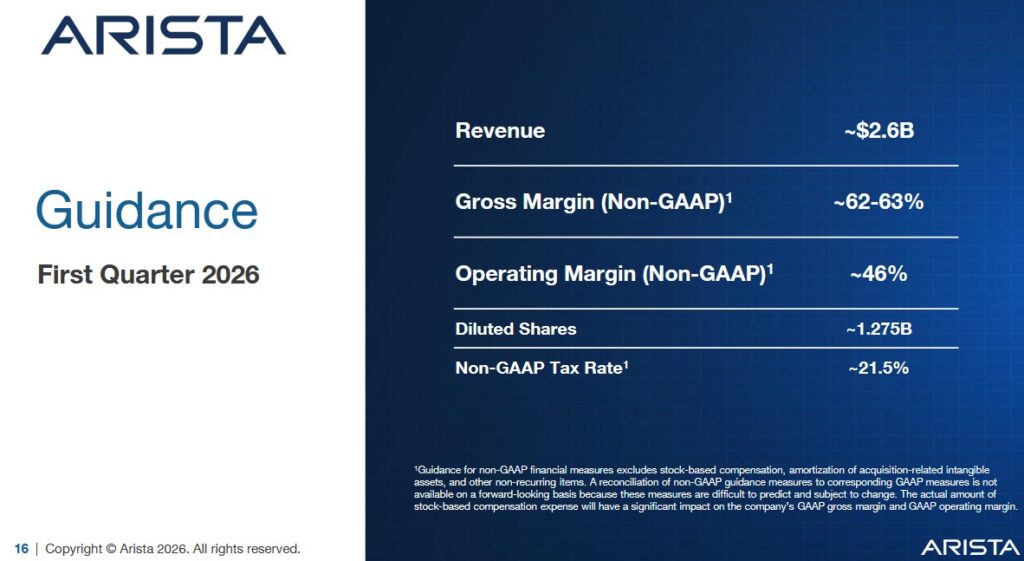

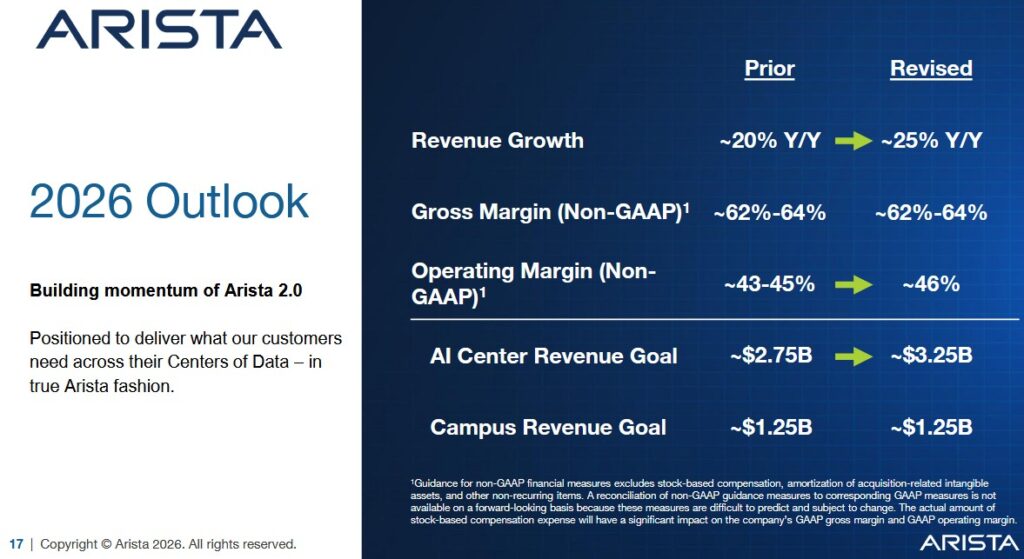

Q1 Guidance and FY2026 Outlook

The preliminary outlook when I published my December 3, 2025 post was:

- Revenue growth of ~20%;

- Revenue growth of ~20%, or ~$10.65B.

- Gross margin of ~62% – ~64%; and

- Operating margin of ~43% – ~45%.

The following is ANET’s current Q1 2026 guidance and FY2026 outlook.

ROIC and WACC

Return on Invested Capital (ROIC) provides an indication of a company’s efficiency. In essence, is a company actually creating value or ‘burning’ cash for the sake of growth?

A company with a higher ROIC is mathematically worth more because it requires less reinvestment to achieve that growth.

A good indication of how well a company is performing is to compare ROIC to the Weighted Average Cost of Capital (WACC). WACC, however, is not a metric officially reported by ANET but it can be roughly estimated based on the company’s credit profile and market conditions.

The generally accepted high-level formula used by Wall Street is:

ROIC = NOPAT/Average Invested Capital

with the Net Operating Profit After Tax (NOPAT) formula being Operating Income (EBIT) x (1-tax rate)

This shows how much profit the core business makes while ignoring how much debt the company has.

The Average Invested Capital is the total money tied up in the business.

- The Operating Approach formula is

- The Financing Approach is

One shortcoming with ROIC is that it is a non-GAAP metric meaning the input data plugged into the ROIC formula is inconsistent.

Analyzing ANET’s ROIC and WACC reveals a company that is not just growing, but generating massive ‘excess returns’. It remains one of the most efficient capital allocators in the technology sector with most analyst models placing ANET’s ROIC between 35% – 45% (adjusted for excess cash). This is exceptionally high for a hardware-adjacent company.

Its WACC, on the other hand, is ~9% – ~11% because the company has no debt on its balance sheet.

Given these metrics, the spread between ANET’s ROIC and WACC is~25% – ~35%.

Calculating a precise ROIC, however, is difficult because of ANET has $10.74 billion in cash and marketable securities on its FYE2025 Balance Sheet.

In a standard ROIC formula (NOPAT / Total Assets – Current Liabilities), the $10.7B in cash is included in the denominator. Cash, however, earns a low rate of return compared to the core business (selling 800G switches). This, therefore, negatively affects the reported ROIC.

If we want to determine the true efficiency of the business, analysts use Invested Capital (excluding cash). Removing this cash from the denominator leads to an increase in ANET’s ROIC from the mid-teens to over 40%.

The other complication is the level of deferred revenue ($5.4B at FYE2025).

Deferred revenue is cash ANET has already collected from customers (for services like CloudVision or maintenance) but has not yet earned as accounting revenue.

Because this is a ‘non-interest bearing liability’, it is a source of free capital. ANET is essentially using its customers’ money to fund its own R&D.

Unless we treat deferred revenue as an operating liability rather than capital, we will overestimate the amount of equity/debt actually needed to run the business, thereby understating the ROIC.

ANET’s high ROIC is a direct result of its ‘asset light’ model. ANET outsources all manufacturing this keeping Invested Capital very low. Furthermore, its EOS software is a single image across all products so their R&D is highly efficient because they do not need to reinvent the wheel for every new switch speed.

Risk Assessment

ANET has no debt to rate.

Dividends and Share Repurchases

Dividend and Dividend Yield

Page 19 of 181 in the FY2024 Form 10-K reflects the following:

We have not paid dividends in the past and do not intend to pay dividends for the foreseeable future.

Stock Splits

ANET initiated a 4:1 stock split on December 4, 2024.

Share Repurchases

When I initiated a position in ANET I indicated one area of concern was the growth in its annual SBC. The company, however, repurchases shares that more than offset the number of shares being issued as part of its various employee compensation packages (see table presented in the Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX section of this post). The exception is FY2023 when SBC exceeded share repurchases by ~$0.185B.

In May 2025, ANET completed repurchases under its prior $1.2B stock repurchase program and its Board authorized a new $1.5B stock repurchase program. This authorization allows ANET to repurchase shares of its common stock that will be funded from working capital.

The FYE2025 Condensed Consolidated Statements of Cash Flows reflects $1.6031B of share repurchases versus $0.4392B of SBC.

ANET repurchased $620.1 million of its common stock at an average price of $127.84/share in Q4.

It repurchased $1.6B of its common stock at an average price of $100.63/share in FY2025.

Valuation

The February 13 closing share price is ~$141.59.

The following broker adjusted diluted earnings estimates are likely to change slightly over the coming days.

- FY2026 – 24 brokers – ~41.04 using a mean of $3.45 and low/high of $3.24 – $3.81.

- FY2027 – 22 brokers – ~34 using a mean of $4.17 and low/high of $3.70 – $5.24.

- FY2028 – 10 brokers – ~27.4 using a mean of $5.16 and low/high of $4.42 – $6.47.

ANET’s FCF/share exceeds GAAP EPS the past couple of years. I anticipate this will be the case in FY2026.

If ANET generates $2.90 of GAAP EPS and we use a ~110% conversion ratio, the FY2026 FCF should be ~$3.19 (modified calculation method). Divide ~$141.59 by $3.19 and the P/FCF is ~44.4.

In my December 3, 2025 post, I wrote:

On December 2, 2025, I initiated a position @ $127.505. In the first 9 months of FY2025, it generated $2.00 EPS. While ANET does not provide diluted EPS guidance for the year I conservatively estimate it will generate ~$2.70 for the year despite the anticipated increase in outstanding shares. Using this estimate, the forward diluted PE is ~47.22.

Using my purchase price and the currently available adjusted diluted EPS broker estimates, ANET’s forward adjusted diluted PE levels are:

- FY2025 – 24 brokers – ~44.43 using a mean of $2.87 and low/high of $2.69 – $2.91.

- FY2026 – 24 brokers – ~38.18 using a mean of $3.34 and low/high of $3.09 – $3.71.

- FY2027 – 19 brokers – ~31.8 using a mean of $4.01 and low/high of $3.53 – $4.45.

I place very little reliance on broker estimates as much can happen to make these estimates irrelevant. Furthermore, the disparity in estimates implies that the brokers which cover ANET have very different outlooks.

Conventional FCF Calculation

In the first 9 months of FY2025, ANET generated $2.373 of FCF calculated using the conventional method of calculating FCF. If I extrapolate the YTD FCF for the first 9 months of the year, ANET should generate another $0.791 of FCF in Q4 2025 ($2.373/3 = $0.791). Adding $2.373 and $0.791 we get $3.164. If I give this a margin of safety and estimate ANET will generate ~$3.10 of FCF for the year, the forward P/FCF is ~41.

Modified FCF Calculation

In the first 9 months of FY2025, ANET generated $2.133 of FCF calculated using the modified method of calculating FCF. If I extrapolate the YTD FCF for the first 9 months of the year, ANET should generate another $0.711 of FCF in Q4 2025 ($2.133/3 = $0.711). Adding $2.133 and $0.711 we get $2.844. If I give this a margin of safety and estimate ANET will generate ~$2.78 of FCF for the year, the forward P/FCF is ~45.9.

These valuation appear to be high. ANET, however, is growing rapidly and generates strong margins. The company is also debt free and strategically repurchases shares thus ‘increasing my share of the company’.

Final Thoughts

My current ANET exposure consists of 500 shares at an average cost of $126.6619 in a ‘Core’ account in the FFJ Portfolio.

The following Final Thoughts are in addition to those in my December 3, 2025 post.

ANET has moved from a conservative growth stance to an aggressive expansion phase. It has officially doubled its AI networking revenue goal to $3.25B for FY2026 – an increase from $1.5B in FY2025.

Management has signaled for the first time that 25% annual revenue growth is the new baseline through 2026; the FY2026 revenue target is $11.25B.

The primary driver of ANET’s long-term health is the industry-wide validation of Ethernet for AI. Historically, Nvidia’s (NVDA) proprietary InfiniBand was the only way to connect thousands of GPUs. Hyperscalers such as Meta, Microsoft, Amazon (AWS), and Alphabet have proven that Ethernet (RoCE) provides equivalent performance at a significantly lower total cost of ownership.

ANET’s new Etherlink portfolio (supporting 800G and 1.6T speeds) is designed to replace InfiniBand. Because it is an open standard, customers are not ‘locked in’ to NVDA’s ecosystem, making ANET the preferred neutral supplier.

To maintain a high ROIC over the next decade, ANET is aggressively moving into higher-margin territory. ANET is no longer just for massive data centers. It is on track to hit $1.25B in Campus revenue in 2026, taking direct market share from Cisco in the corporate office and branch space.

Through its CloudVision and NetDL platforms, ANET is increasing its ‘recurring revenue’ mix. Software and services now account for nearly 17% of total revenue, providing a buffer against hardware cycle volatility.

Although ANET has a bullish outlook, there are risks:

- The likes of Meta, Microsoft, Amazon (AWS), and Alphabet make up nearly 50% of revenue. Their massive buying power forces ANET to give volume discounts which is why management has guided 2026 operating margins down slightly to 46% from the historic 48%+ highs.

- NVDA is not ceding the Ethernet market. Its Spectrum-X Ethernet platform is a direct competitor to ANET.

- Shares trade at ~40 – ~45 times forward adjusted diluted EPS. ANET had better meet/exceed expectations. Any hiccup in the AI spending cycle could lead to significant short-term stock volatility, even if the long-term business remains strong.

I intend to increase my ANET exposure but am cautiously optimistic volatile market conditions may present an opportunity to acquire additional shares at a better valuation.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long ANET.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.