![]() I last reviewed Veeva Systems (VEEV) in this November 21, 2025 post at which time the Q3 and YTD2026 results had just been released following the November 20, 2025 market close. At the end of Q3, the company had ~$1.66B in cash and cash equivalents and ~$4.977B in short-term investments. Meanwhile, its total liabilities amounted to $0.234B when we exclude ~$0.823B in short-term deferred revenue (funds received from clients prior to providing services).

I last reviewed Veeva Systems (VEEV) in this November 21, 2025 post at which time the Q3 and YTD2026 results had just been released following the November 20, 2025 market close. At the end of Q3, the company had ~$1.66B in cash and cash equivalents and ~$4.977B in short-term investments. Meanwhile, its total liabilities amounted to $0.234B when we exclude ~$0.823B in short-term deferred revenue (funds received from clients prior to providing services).

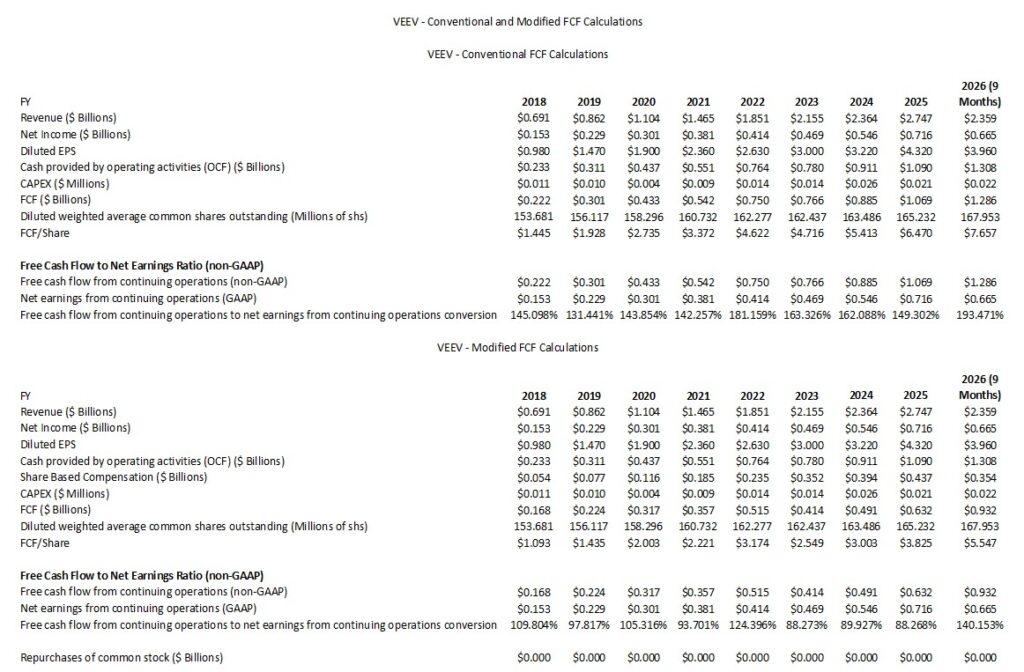

My thoughts were that VEEV has the financial flexibility to initiate a share repurchase program to offset the increase in the weighted average number of diluted shares outstanding which has crept up from 158.296 million in FY2020 to 167.953 in Q3 FY2026. This increase is the result of shares being issued under the company’s various share-based compensation programs. The following table shows the extent to which VEEV’s weighted average number of diluted outstanding shares has increased over the past several years.

New Share Repurchase Program

On January 5, 2025, VEEV announced a $2B share repurchase program.

If VEEV were to repurchase ~$2B of its issued and outstanding shares at an average ~$250 share repurchase price, it could repurchase ~8 million shares. Were this to happen, the diluted weighted average number of outstanding shares could retrace to the FY2022 level. Meanwhile, the company’s financial metrics have improved since FY2022.

Valuation

In my prior post, I reflect the following:

Following the share price pullback after the release of Q3 and YTD2026 results and the increase in management’s guidance, VEEV’s valuation is attractive. I have, therefore, acquired an additional 100 shares in a ‘Core’ account in the FFJ Portfolio @ ~$239.1772 on November 21, 2025.

Valuation Based On FCF Estimates

The company’s FY2026 Non-GAAP Fully Diluted Net Income per Share outlook is ~$7.93. The non-GAAP and GAAP diluted EPS values in FY2022 – FY2025 reflect an increasing variance between GAAP and non-GAAP earnings.

- In FY2025, VEEV generated $6.60 and $4.32 of non-GAAP and GAAP earnings per share, a variance of $2.28.

- In FY2024, VEEV generated $4.84 and $3.22 of non-GAAP and GAAP earnings per share, a variance of $1.62.

- In FY2023, VEEV generated $4.28 and $3.00 of non-GAAP and GAAP earnings per share, a variance of $1.28.

- In FY2022, VEEV generated $3.73 and $2.63 of non-GAAP and GAAP earnings per share, a variance of $1.10.

In the first 9 months of FY2026, VEEV generated $6.00 and $3.96 of non-GAAP and GAAP earnings per share for a variance of $2.04.

If the variance continues at the same pace as in the first 3 quarters, the variance for the entire year could be ~$2.80. Deduct ~$2.80 from the ~$7.93 FY2026 non-GAAP outlook and the FY2026 GAAP EPS could be ~$5.13.

If we apply a 140% FCF to net earnings ratio (to be somewhat consistent with prior years), VEEV’s FCF/share could be ~$7.18 (~$5.13 x 140%) when calculated under the conventional method.

If we apply a 95% FCF to net earnings ratio (to be somewhat consistent with prior years), VEEV’s FCF/share would be ~$4.87 (~$5.13 x 95%) when calculated under the modified method.

VEEV’s share price has plunged of late yet the company is still performing well. As a result, I acquired 100 additional shares @ ~$239.1772 on November 21, 2025. Using this purchase price, VEEV’s P/FCF is ~33.3 if we use ~$7.18 or ~49.1 if we use ~$4.87.

These valuations are far superior to those reflected in my prior post.

Valuation Based On Adjusted Diluted EPS Broker Estimates

Broker earnings estimates are currently under revision. At the moment, however, the following are VEEV’s forward adjusted diluted PE levels using the current broker estimates and my ~$239.1772 purchase price.

- FY2026 – 30 brokers – mean of $7.89 and low/high of $7.78 – $8.04. Using the mean estimate, the forward adjusted diluted PE is ~30.3.

- FY2027 – 30 brokers – mean of $8.49 and low/high of $7.55 – $8.91. Using the mean estimate, the forward adjusted diluted PE is ~28.2.

- FY2028 – 22 brokers – mean of $9.71 and low/high of $8.54 – $13.42. Using the mean estimate, the forward adjusted diluted PE is ~24.6.

In my August 28, 2025 post I reflect the following:

Valuation Based On FCF Estimates

The company’s FY2026 Non-GAAP Fully Diluted Net Income per Share outlook is ~$7.78. The non-GAAP and GAAP diluted EPS values in FY2022 – FY2025 reflect an increasing variance between GAAP and non-GAAP earnings.

- In FY2025, VEEV generated $6.60 and $4.32 of non-GAAP and GAAP earnings per share, a variance of $2.28.

- In FY2024, VEEV generated $4.84 and $3.22 of non-GAAP and GAAP earnings per share, a variance of $1.62.

- In FY2023, VEEV generated $4.28 and $3.00 of non-GAAP and GAAP earnings per share, a variance of $1.28.

- In FY2022, VEEV generated $3.73 and $2.63 of non-GAAP and GAAP earnings per share, a variance of $1.10.

In the first half of FY2025, VEEV generated $3.12 and $2.02 of non-GAAP and GAAP earnings per share, a variance of $1.10. In comparison, VEEV generated $3.96 and $2.56 of non-GAAP and GAAP earnings per share (a $1.40 variance) in the first half of FY2026.

If the variance in the second half of FY2026 is similar to that in the first half, the variance for the entire year could be ~$2.80. Deduct ~$2.80 from the ~$7.78 FY2026 non-GAAP outlook and the FY2026 GAAP EPS could be ~$4.98.

If we apply a 140% FCF to net earnings ratio (to be somewhat consistent with prior years), VEEV’s FCF/share could be ~$6.97 (~$4.98 x 140%) when calculated under the conventional method.

If we apply a 95% FCF to net earnings ratio (to be somewhat consistent with prior years), VEEV’s FCF/share would be ~$4.73 (~$4.98 x 95%) when calculated under the modified method.

With shares trading at ~$278 as I compose this post, VEEV’s P/FCF is ~40 if we use ~$6.97 or ~58.8 if we use ~$4.73.

At the time of my May 29, 2025 post, VEEV’s share price was ~$279. My calculations suggested that VEEV’s forward P/FCF was ~39.5 and ~66.6 calculated using the conventional and modified FCF.

Valuation Based On Adjusted Diluted EPS Broker Estimates

Broker earnings estimates are currently under revision. At the moment, however, the following are VEEV’s forward adjusted diluted PE levels using the current broker estimates and a ~$278 share price.

- FY2026 – 30 brokers – mean of $7.75 and low/high of $7.62 – $7.93. Using the mean estimate, the forward adjusted diluted PE is ~35.9.

- FY2027 – 30 brokers – mean of $8.42 and low/high of $7.55 – $8.96. Using the mean estimate, the forward adjusted diluted PE is ~33.

- FY2028 – 18 brokers – mean of $9.66 and low/high of $8.24 – $13.78. Using the mean estimate, the forward adjusted diluted PE is ~28.8.

At the time of my May 29, 2025 post, the following were VEEV’s forward adjusted diluted PE levels using the current broker estimates and a ~$279 share price.

- FY2026 – 29 brokers – mean of $7.50 and low/high of $7.17 – $7.76. Using the mean estimate, the forward adjusted diluted PE is ~37.2.

- FY2027 – 29 brokers – mean of $8.24 and low/high of $7.58 – $8.69. Using the mean estimate, the forward adjusted diluted PE is ~33.9.

- FY2028 – 12 brokers – mean of $9.38 and low/high of $8.56 – $10.10. Using the mean estimate, the forward adjusted diluted PE is ~29.7.

On January 6, 2026, I acquired an additional 100 shares @ ~$234.115. When I wrote my prior post, I disclosed the purchase of additional shares @ ~$239.1772 on November 21, 2025.

Now that my purchase price is lower and the adjusted diluted EPS broker estimates are higher, VEEV’s valuation using more current metrics is:

- FY2026 – 27 brokers – mean of $7.94 and low/high of $7.92 – $8.04. Using the mean estimate, the forward adjusted diluted PE is ~29.5.

- FY2027 – 27 brokers – mean of $8.57 and low/high of $8.23 – $8.93. Using the mean estimate, the forward adjusted diluted PE is ~27.3.

- FY2028 – 22 brokers – mean of $9.78 and low/high of $8.54 – $14.21. Using the mean estimate, the forward adjusted diluted PE is ~24.

VEEV’s valuation using broker estimates is more favorable than at the time of my last review.

If the share price is lower and I make no adjustments to my FCF estimates, its stands to reason that its valuation is superior to that at the time of my prior review.

Final Thoughts

I continue to like the company’s long-term outlook and am confident management’s $6B revenue goal by FY2030 is realistic; VEEV set an ambitious target in 2019 of achieving $3B of annual revenue by 2025 and achieved this target.

Despite liking VEEV’s long-term outlook, my concern was the increase in the weighted average diluted shares outstanding. This is the reason why I refrained from increasing my exposure in mid-December 2025 when the share price dropped below ~$220.

On January 5, 2026, however, VEEV announced a $2B share repurchase program. This has led to a share price surge on January 6. Despite this surge, I think VEEV remains undervalued. I, therefore, acquired an additional 100 shares @ ~$234.115 bringing my VEEV exposure to 700 shares in a ‘Core’ account in the FFJ Portfolio.

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long VEEV.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.