In my June 9, 2025 post I disclose my decision to acquire an additional 500 shares in Howard Hughes Holdings (HHH) after disclosing a 500 share position in the FFJ Portfolio in my June 3 post.

In my June 9, 2025 post I disclose my decision to acquire an additional 500 shares in Howard Hughes Holdings (HHH) after disclosing a 500 share position in the FFJ Portfolio in my June 3 post.

In these two posts I touch upon how HHH is about to undergo a radical transformation. This transformation includes either building an insurance company from scratch or the acquisition of an established insurance company. Creating an insurance company from ‘scratch’, is time consuming. Bill Ackman (Executive Chairman) and his Pershing Square Holdings senior executive team’s preference, therefore, is to acquire an established insurance company.

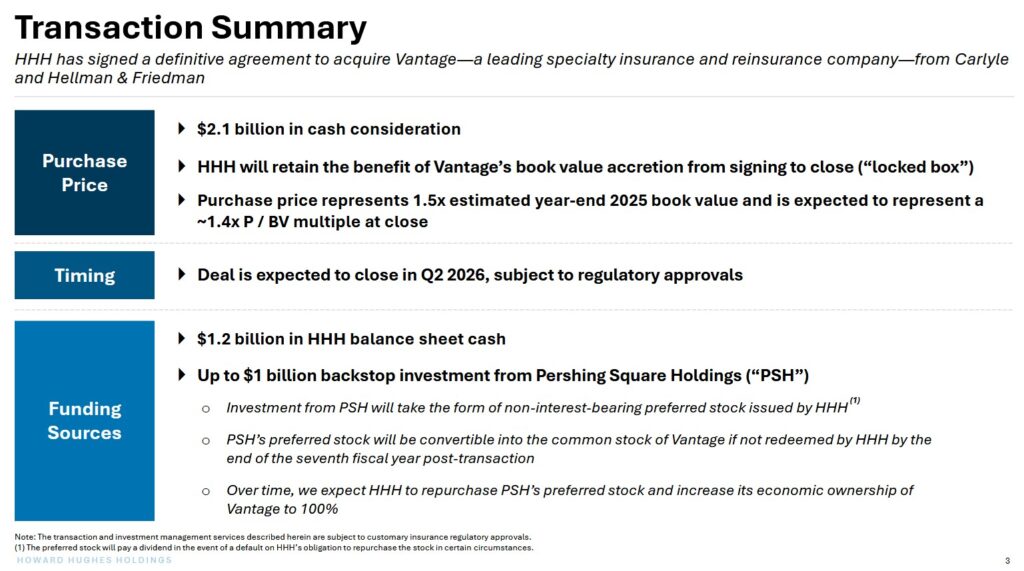

Fast forward to December 18 and HHH announces that it has entered into a definitive agreement to acquire 100% of Vantage Group Holdings Ltd. (‘Vantage’), a privately held leading specialty insurance and reinsurance company backed by Carlyle and Hellman & Friedman, for ~$2.1B. The transaction is expected to close in Q2 2026. Upon closing, Vantage will anchor HHH’s transformation into a diversified holding company.

Following this announcement, I acquired an additional 500 shares @ $78.98 on December 22. My current HHH exposure is 1500 shares.

Business Overview

As noted in my prior posts, the historical HHH will look very different from the HHH of the future.

Historically, HHH’s business has been in the development and operation of master planned communities (MPCs) in the United States. The company has consisted of the Operating Assets, MPC, and Strategic Developments business segments. The Operating Assets segment acquires or develops retail, office, and multifamily properties, as well as invests in other real estate properties. The MPC segment develops and sells land in large-scale and long-term community development projects in and around Las Vegas, Nevada; Houston, Texas; and Phoenix, Arizona to homebuilders and developers. The Strategic Developments segment develops residential condominium and commercial property projects, as well as various other properties.

The plan is to transform HHH so that it closely resembles a Berkshire Hathaway (BRK-a and BRK-b). Analyzing HHH’s historical results, therefore, adds little value to my investment decision making process.

Nevertheless, I recommend reviewing the company’s website and Part 1 Item 1 in the FY2024 Form 10-K to understand the current nature of HHH’s business operations.

A series of videos on the HHH website provide a good overview of HHH’s current operations.

Pershing Square’s comprehensive presentation pertaining to the increase in its HHH investment is accessible here.

HHH’s Acquisition of Vantage Group Holdings

The following, extracted from the December 18, 2025 presentation, provides a very high level overview of the proposed acquisition of Vantage. Considerably more detail is included in this presentation, and therefore, I recommend reviewing it.

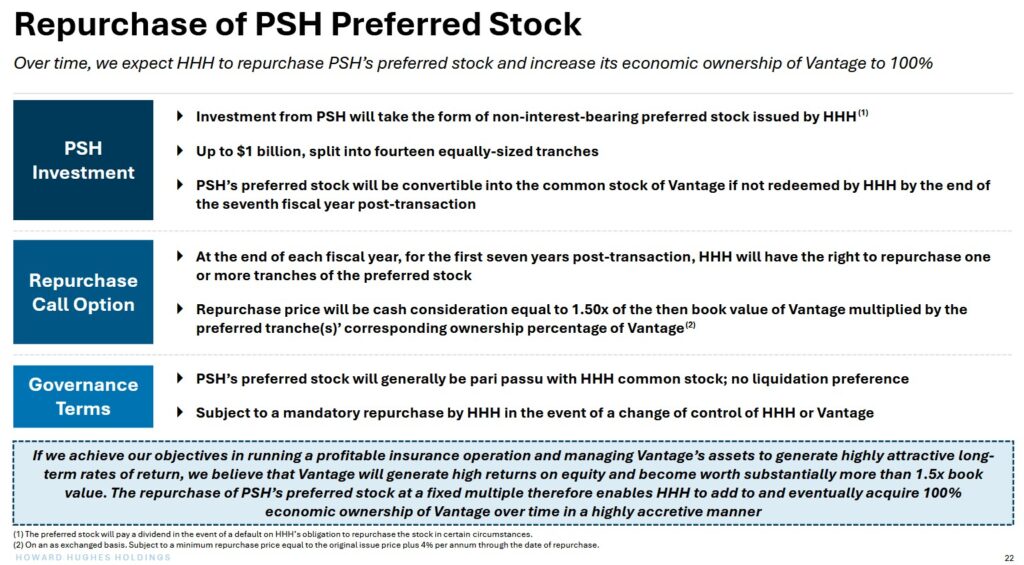

HHH will avail itself of the cash on its Balance Sheet to finance the acquisition. In addition, Pershing Square Holdings (PSH) will provide financing in the form of non-interest-bearing preferred stock. The structure of the PSH investment, however, permits HHH to repurchase this preferred stock over time.

Financials

On November 10, 2025, HHH released its financial results for the 3rd quarter ended September 30, 2025. There is little point in reviewing HHH’s historical results since it is undergoing such a radical transformation that historical results are likely to differ significantly from future results.

Risk Assessment

As noted in several prior posts, I am not prepared to expose myself to a permanent capital impairment. I, therefore, pay particularly close attention to the risk aspect of my investments. This includes a review of the risk ratings (and reasoning for same) assigned to a company’s unsecured domestic debt.

As an equity investor, my risk exceeds that of unsecured creditors. I, therefore, generally refrain from investing in a company if the unsecured domestic debt ratings are BBB- / Baa3 or worse. The BBB- / Baa3 ratings are the lowest investment grade tier, and therefore, my risk as an equity investor is non-investment grade.

On December 19, 2025, S&P Global placed The Howard Hughes Corporation’s current (B) domestic long-term unsecured credit rating under review with a positive outlook. This current rating is the middle tier of the Highly Speculative non-investment grade category.

On December 19, 2025, S&P Global placed Vantage Group’s BBB- long-term unsecured credit rating under review with negative implications. Following the Vantage acquisition, I anticipate that HHH’s domestic long-term unsecured credit rating could improve to a non-investment grade speculative rating (BB- to BB+). Over the long-term, I envision HHH’s domestic long-term unsecured credit rating will improve to investment grade.

Moody’s continues to reflect a Ba3 rating for The Howard Hughes Corporation; this rating was downgraded from Ba2 on April 25, 2023. This is the bottom tier of the non-investment grade speculative non-investment grade ratings. On August 11, 2023, however, Howard Hughes Holdings Inc., a new holding company, replaced The Howard Hughes Corporation (HHC) as the public company trading on the New York Stock Exchange. Existing shares of common stock of HHC were automatically converted, on a one-for-one basis, into shares of common stock of HHH, with the same designations, rights, powers, and preferences, and the same qualifications, limitations, and restrictions, as the shares of HHC common stock immediately prior to the reorganization.

On December 15, 2025, Fitch affirmed the BB Long Term Issuer Default Rating issued to Howard Hughes Holdings Inc.. This is the middle tier of the non-investment grade speculative non-investment grade ratings. This was done before the announcement of HHH’s proposed acquisition of Vantage.

On December 23, 2025 Fitch published the following:

Howard Hughes Holdings (HHH) has announced a definitive agreement to acquire private insurance company, Vantage Group Holdings Ltd. for $2.1 billion. Fitch Ratings has anticipated a transaction of this type since Pershing Square Holdings, Ltd. (PSH) invested $900 million into HHH’s common equity in May 2025. Fitch views the transaction as moderately positive for HHH’s ‘BB’ Issuer Default Rating. It will improve revenue diversification while maintaining a similar leverage level even if Fitch does not give equity credit to the preferred stock component of the transaction funding.

Fitch does not expect the Vantage transaction to affect HHH’s rating. Fitch contemplated such a transaction in its most recent affirmation of HHH’s rating, and this announcement aligns with our expectations. The transaction will not significantly affect HHH’s leverage.

PSH’s (BBB+/Stable) common equity infusion into HHH marked the starting point for transforming Howard Hughes into a diversified holding company. HHH will retain its real estate assets and add an insurance business, which will create diversification. Pershing Square has searched for an insurance business since its incremental equity investment in HHH and aimed to announce a deal by year-end 2025. HHH expects to close the Vantage acquisition in second-quarter 2026.

The $2.1 billion purchase price combines $1.2 billion cash from HHH’s balance sheet and up to $1.0 billion in preferred stock issued by HHH to PSH. This preferred stock will be non-interest-bearing. PSH’s preferred stock will convert into Vantage common stock if HHH does not redeem it by the end of the seventh year post-transaction (2033 if the deal closes by June 30, 2026). Fitch would not treat this preferred stock as equity in its leverage calculations due to the anticipated change of control as well as its expected non-permanent nature. HHH expects to repurchase PSH’s preferred stock over time and increase its economic ownership of Vantage to 100%.

I anticipate that HHH’s domestic unsecured credit ratings will gradually improve over time.

Dividend and Dividend Yield

HHH distributes no dividend and it is unlikely a dividend will be distributed in the foreseeable future.

The vision is to transform HHH into a diversified holding company by acquiring controlling stakes in high-quality, durable growth public and private operating companies while continuing to invest in and grow the Company’s core real estate development and Master Planned Communities business. Investors should not anticipate share repurchases in the foreseeable future.

Valuation

There is little point in trying to determine HHH’s value since the current form of HHH will differ significantly from that in another few quarters.

Final Thoughts

My final thoughts are the same as in my prior HHH posts.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long HHH.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.