![]()

Prior to our lawyer and accountant subscribing to DocuSign (DOCU), we had to attend their offices to execute documents. Fortunately, COVID changed the manner in which business was conducted. I say fortunately because many businesses were forced to make their processes more efficient (eg. implementation of DOCU services for e-signature purposes).

I initially looked at DOCU in 2020 but was unimpressed by its poor financial performance. The company was losing money yet some investors were shelling out ~$220/share to invest in this company. As the months progressed and the share price approached $300, I became increasingly concerned that ‘all would not end well’ for some DOCU investors.

Not surprisingly, the bottom fell out of DOCU’s share price and by mid-2022, DOCU shares were trading in the $50s – $60s.

Looking at the Form 10-K and Form 10-Q SEC Filings for the past several years, it is readily apparent the company is much different from a few years ago. When I initially looked at DOCU, the company’s focus was predominantly selling products to commercial businesses and very small businesses. In recent years, DOCU has expanded its focus to target enterprise customers.

On December 4, 2025, DOCU released its Q3 2026 results thus prompting me to analyze it to ascertain whether I should initiate a position in the FFJ Portfolio.

Industry Overview

A good way to learn about the company is to read Item 1 – Business Overview in the Form 10-Ks that are accessible through the SEC Filings section of the company’s website.

The following is found within the ‘Our Competition’ section of DOCU’s FY2025 Form 10-K:

Our primary global competitor for eSignature is currently Adobe, which offers an electronic signature solution known as Adobe Acrobat Sign as well as other global software companies that have or may elect to include an electronic signature capability in their products. We also face competition from a select number of vendors that focus on specific industries, geographies, or product areas such as contract lifecycle management and advanced contract analytics. We believe Intelligent Agreement Management is a new software category without incumbent competitors, although elements of our IAM platform may compete with existing providers of contract lifecycle management, contract analytics workflow management, identity verification and other software solutions.

Other competitors in the electronic signature and agreement management market include:

- Dropbox Sign (formerly HelloSign) which is known for its ease of use and competitive pricing. It appeals in particular to Small to Medium Businesses (SMBs) and integrates well with the Dropbox file storage suite. It is generally more affordable than DOCU and its transparent pricing, with unlimited signing options on lower tiers, is attractive to SMBs.

- PandaDoc: DOCU focuses heavily on security, compliance, and core signature workflows. Its strength is in the signing and closing phase of the agreement. PandaDoc, however, is an all-in-one Document Automation Platform. Its strength lies in the entire lifecycle of a sales document, from creation to signing to payment. Its all-in-one platform for proposals, quotes, contracts, and payments, is often favored by sales teams.

- OneSpan Sign: DOCU has superior brand recognition and overall market share. OneSpan Sign, however, competes by delivering a strong focus on security, compliance, and best-in-class customer support, excelling in enterprise deployments for highly regulated industries like banking.

Other notable competitors and alternatives in the broader digital signature and contract management space include:

- SignNow (part of airSlate) targets the SMB and value-conscious market segments with a highly functional and more affordable solution.

- Zoho Sign focuses on a specific market segment and unique value proposition. It is generally considered a good DOCU alternative for businesses already using the Zoho ecosystem and for cost-conscious SMBs.

- Foxit eSign is often positioned as the best alternative for businesses looking for better value, transparent pricing, and robust compliance features without the high cost of DOCU’s premium tiers. Foxit is a publicly traded Chinese software company, and therefore, some US companies may be highly reluctant to subscribe to its products and services.

- SignEasy headquartered in India is primarily for the segment of the market that prioritizes simplicity, mobile functionality, and predictable, budget-friendly pricing. This is privately held business without external VC funding.

- Oneflow doesn’t just focus on the e-signature part of the agreement but on the entire Contract Lifecycle Management with dynamic, digital-native contracts.

None of these competitors are stagnant. Just because one competitor has a superior offering does not mean this will last in perpetuity.

While some industry participants might have relatively modest annual CAPEX, they typically invest heavily in research and development (R&D). In FY2023 – FY2025 and the first 3 quarters of FY2026, for example, DOCU’s R&D expenditures amounted to ~$0.481B, ~$0.540B, ~$0.589B, and ~$0.497B. In FY2022 – FY2024 and the first 3 quarters of FY2025, Adobe’s (ADBE) R&D expenditures amounted to ~$3B, ~$3.5B, ~$4B, and ~$3.2B.

Business Overview

DOCU states that:

- it has ~1.8 million customers and more than 1 billion users in over 180 countries; and

- ~95% of Fortune 500 companies are its customers.

It is arguably the enterprise leader in e-signatures and sets the global standard for secure electronic signatures. The company has, however, evolved beyond a mere e-signature company.

DOCU now streamlines document workflows for businesses of all sizes while still maintaining enterprise-grade security and compliance standards.

The DOCU platform supports complex workflows with advanced API integrations for seamless automation of document processing.

Advanced API integrations involve complex, real-time, two-way communication and sophisticated logic to automate entire business processes across multiple and often fundamentally different systems. They are designed for scalability, high reliability, and enhanced security to support critical enterprise workflows.

Key features include real time tracking thus allowing a user to monitor document status with automated reminders that help reduce turnaround time. It also has a robust audit trail and multi-factor authentication to ensure documents can be used in court. Furthermore, DOCU’s services tie in with Salesforce, Microsoft products, Google Workspace, and 350 additional platforms.

The company is rapidly adding new features to DocuSign IAM, as it matures from a single product company into a platform in agreement management. Just recently, DOCU launched Agreement Desk, an internal central workspace that keeps teams aligned so agreements are processed faster.

On the Q3 analyst call, management states:

Models trained on the best data deliver the best, most accurate results to customers. One of our biggest differentiators is our enormous library of consented, private agreements, covering a wide variety of contract types, clauses, customer segments, languages, and verticals. We estimate that by training IAM on this rich body of private data, we can achieve a 15% improvement in precision and recall compared to our models trained on public contract data.

Financials

Q3 and YTD2026 Results

DOCU’s Q3 and YTD2026 Form 10-Q is accessible here. The earnings slides, prepared remarks, and earnings call transcript are accessible here.

In Q3 2026, it reported 14% YoY international revenue growth and 30% of total revenue was derived from outside the US.

Total liabilities amounted to ~$2.001B of which ~$1.445B was current contract liabilities and $0.028B was noncurrent contract liabilities. Contract liabilities consist of deferred revenue and payments received in advance of performance under the contract with such amounts generally recognized as revenue over the contractual period. For the nine months ended October 31, 2025 and 2024, DOCU recognized revenue of $1.3B and $1.2B that was included in the corresponding contract liability balance at the beginning of the periods presented.

DOCU’s liabilities amount to ~$0.528B at the end of Q3 when we deduct the contract liabilities from total liabilities. The company’s ~$0.840B cash and cash equivalents and current investments and ~$0.209B in non-current investments exceed all liabilities after backing out deferred revenue.

In essence, the receipt of client funds in advance of rendering services improves DOCU’s liquidity and reduces the need to rely on external financing.

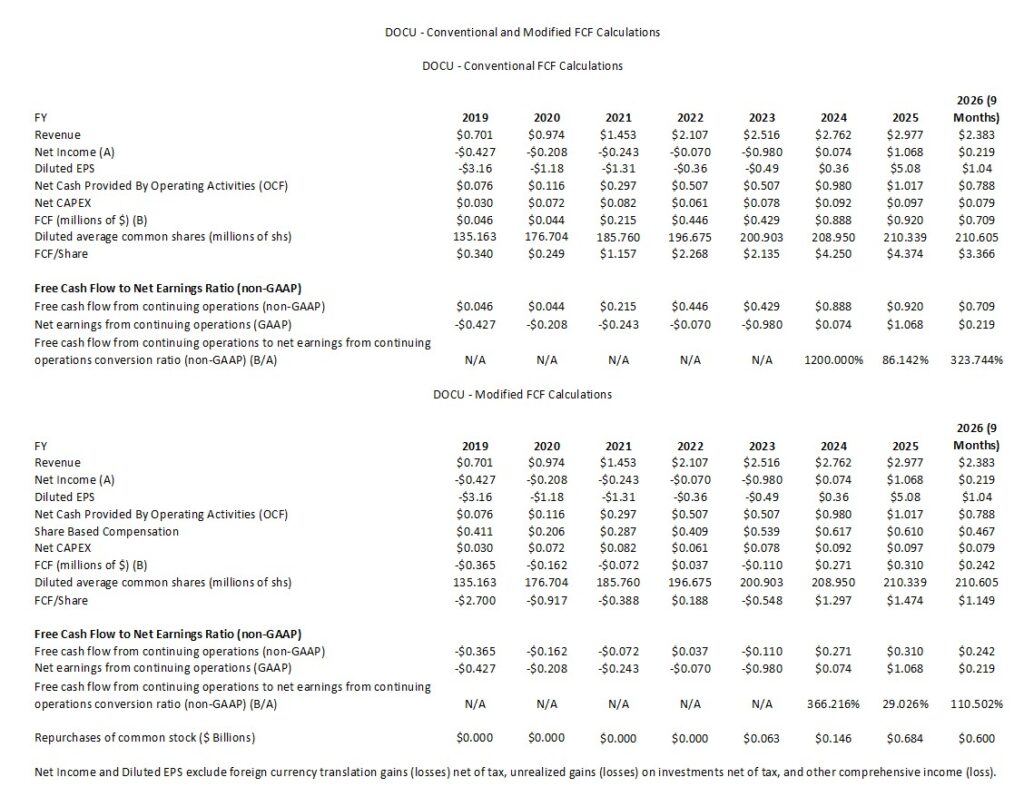

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX

In prior posts I touch upon my rationale for deducting stock-based compensation (SBC) to calculate FCF. I, therefore, dispense with explaining this again.

The following compares DOCU’s FCF using the ‘conventional’ and ‘modified’ calculation methods.

Capital Allocation

DOCU’s capital allocation priority is to reinvest in the business (organic growth and/or acquisitions). Share repurchases are the next priority.

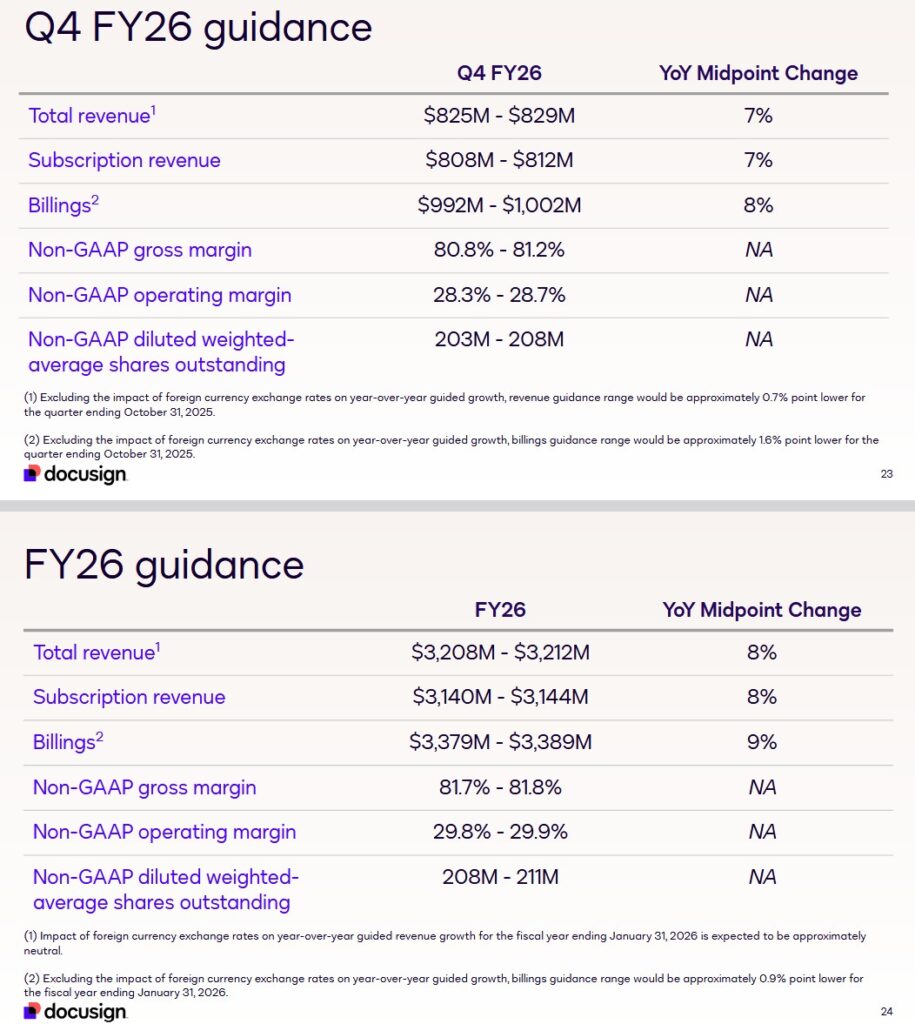

Q4 and FY2026 Guidance

The following guidance was provided on December 4.

For full-year revenue, the annual guidance midpoint is increasing by $15 million from full year guidance provided in Q2. The majority of the increase is driven by Q3 outperformance and the expectation that some of these trends will continue to the fiscal year end.

For full-year billings, the annual guidance midpoint is increasing by $44 million from full year guidance provided in Q2. This increase reflects a portion of the non-timing impact from Q3 business strength.

Interestingly, on the Q3 earnings call, management states that some roles are being shifted to cash compensation from equity. I hope this will alleviate some of my concern about the pace at which SBC has been growing.

Risk Assessment

DOCU has no debt to rate.

Dividends and Share Repurchases

Dividend and Dividend Yield

Page 91 of 135 in the FY2025 Form 10-K reflects that DOCU has not declared nor does it expect to declare dividends.

Stock Splits

DOCU has not had a stock split.

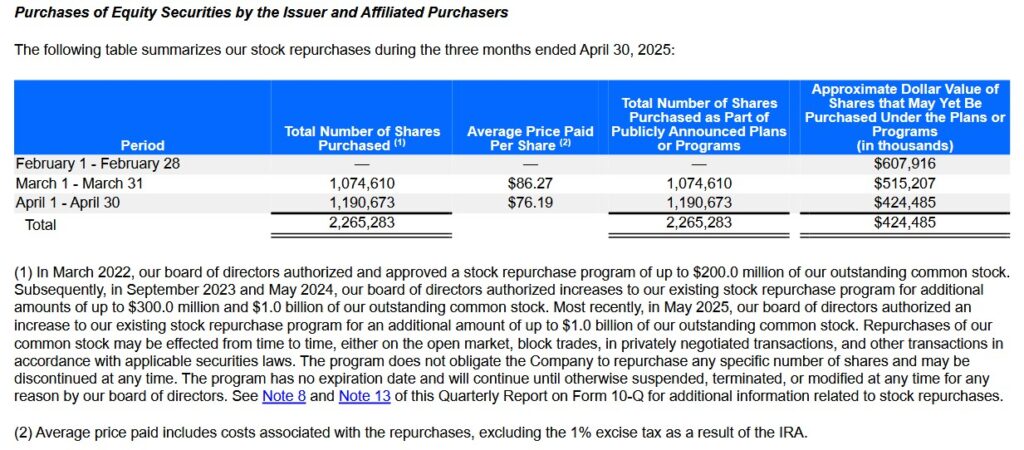

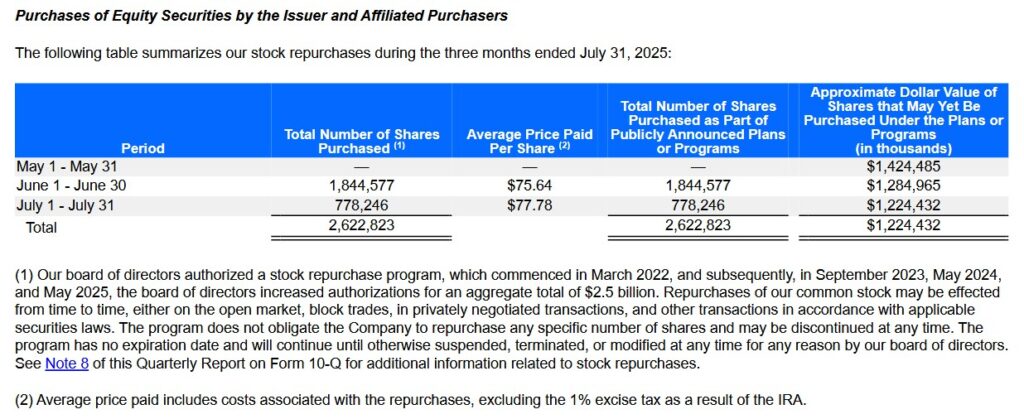

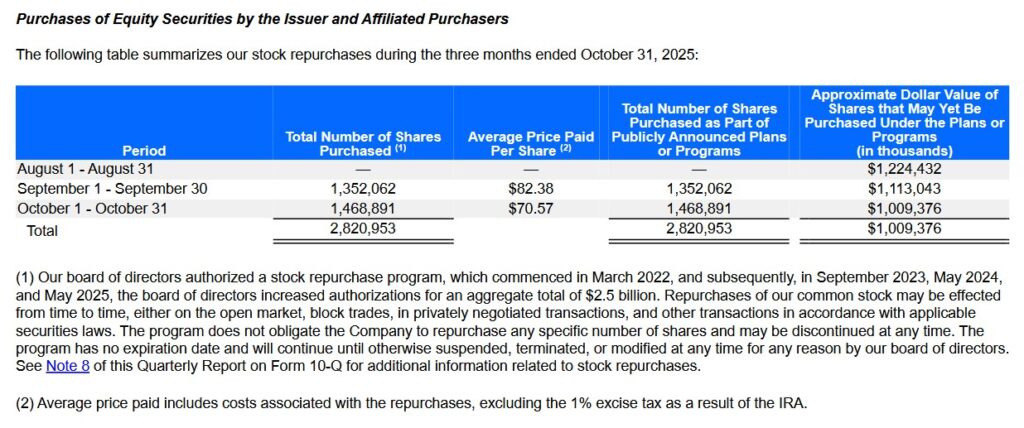

Share Repurchases

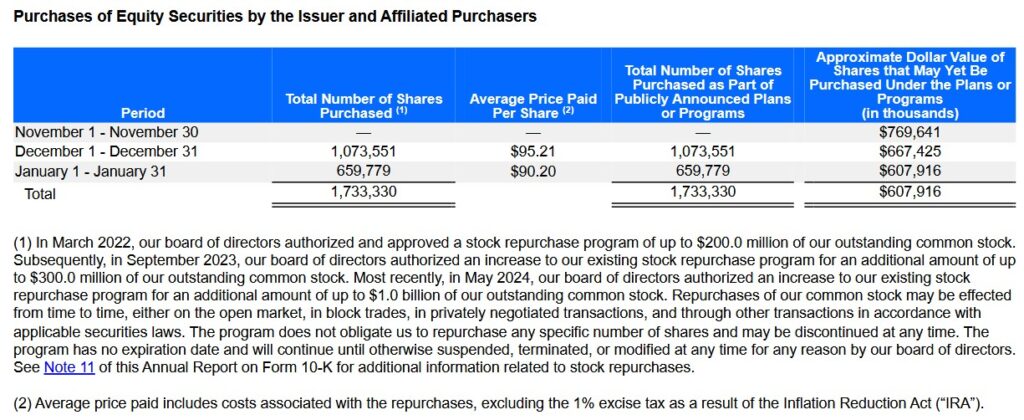

DOCU did not have the wherewithal to repurchase any shares until relatively recently (see table in the Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX section of this post).

Looking at the average price paid per share in each of the last 3 quarters, we see they are well in excess of the current $65.67 share price. I view this as a destruction of shareholder value.

In Q3, DOCU increased the pace of its buyback activity and repurchased $0.215B in shares. This was its single-largest quarterly dollar buyback in the company’s history. Management indicates the plan is to opportunistically repurchase shares with over $1B in remaining buyback authorization.

Valuation

Using the current $65.67 share price and the currently available adjusted diluted EPS broker estimates, DOCU’s forward adjusted diluted PE levels are:

- FY2026 – 20 brokers – ~19 using a mean of $3.75 and low/high of $3.61 – $3.85.

- FY2027 – 20 brokers – ~16 using a mean of $4.11 and low/high of $3.73 – $4.40.

- FY2028 – 13 brokers – ~14.5 using a mean of $4.54 and low/high of $4.05 – $5.13.

I place very little reliance on broker estimates as much can happen to make these estimates irrelevant. Furthermore, the disparity in estimates implies that the brokers which cover the company have very different outlooks.

Conventional FCF Calculation

In the first 9 months of FY2026, DOCU generated $3.366 of FCF calculated using the conventional method of calculating FCF. The diluted weighted-average shares used in computing net income per share in Q3 2026 was 208.069 million. The outlook for Q4 is 203 – 208 million. I estimate DOCU’s FY2026 FCF will be ~$4.52 – ~$4.62. Using the current $65.67 share price, the forward P/FCF will likely be ~14.2 – ~14.5.

Modified FCF Calculation

In the first 9 months of FY2025, DOCU generated $1.149 of FCF calculated using the modified method of calculating FCF. DOCU’s SBC is significant, and therefore, FCF in FY2026 is likely to be ~$1.56 – ~$1.66. Using the current $65.67 share price, the forward P/FCF will likely be ~39.6 – ~42.1.

Final Thoughts

DOCU’s results are improving but I do not intend to initiate a position for the following reasons:

- The company operates in a highly competitive space. Industry consolidation is likely to occur over time and I am unable to determine if DOCU will be a ‘survivor’.

- At first blush, DOCU appears to be generating strong FCF. Deducting stock-based compensation expense from net cash provided by operating activities, however, paints a different picture.

- DOCU’s track record for improving shareholder value through share repurchases is questionable. The current share price is $65.67 but DOCU has repurchased shares throughout the past 4 quarters at average prices well in excess of the current share price.

There are other investment opportunities that have the potential to generate superior returns, and therefore, I have no immediate plan to initiate a DOCU Position.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I have no DOCU exposure and do not intend to initiate a position.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.