![]()

As a risk averse investor, I like to invest in highly profitable undervalued/fairly valued growing companies that generate strong earnings and free cash flow. Companies with no debt (or exceptionally low debt levels) are particularly attractive.

Following my analysis of Arista Networks (ANET), I acquired 200 shares @ $127.505 on December 2, 2025 in one of the ‘Core’ accounts in the FFJ Portfolio.

Industry Overview

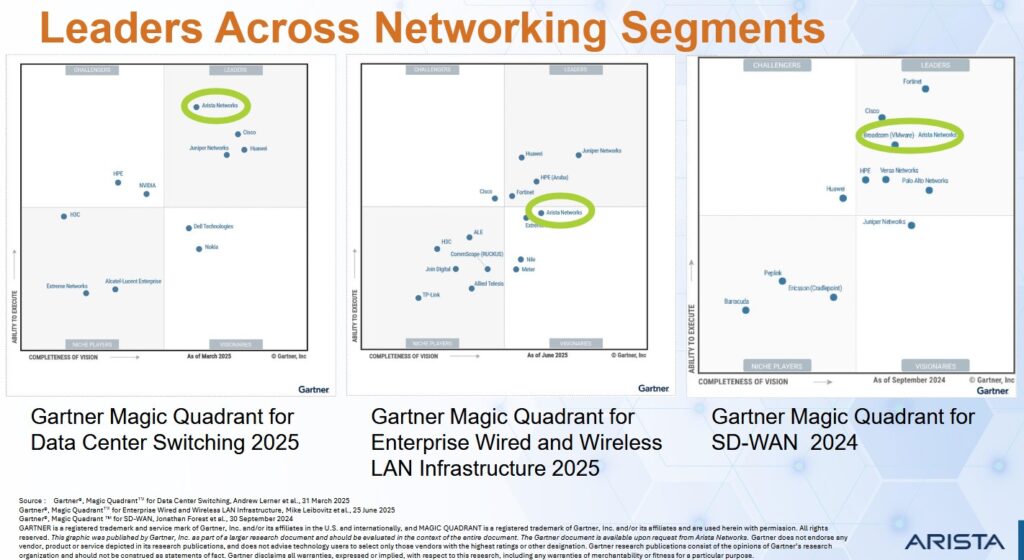

ANET operates primarily in the Data Center and Cloud Networking market. Its largest and most significant competitors, particularly in the core data center and enterprise networking segments, are:

- Cisco Systems (CSCO) which is often considered the largest overall competitor in the broader networking market. Its Nexus portfolio directly competes with ANET’s offerings in the data center.

- Juniper Networks which was acquired by Hewlett Packard Enterprise (HPE) on July 2, 2025. Juniper competes with its own switching and routing products, which are often cited for their manageability and ease of use.

- HPE’s networking division, particularly Aruba, is a strong competitor in the enterprise and campus networking markets, which ANET is increasingly targeting.

- NVIDIA (NVDA) is heavily involved in high-speed interconnects (InfiniBand and Ethernet) crucial for AI data centers. It is a key ANET competitor, particularly in the high-performance and and AI networking space.

- Other Competitors includes Dell Technologies, Extreme Networks, and Huawei (largely outside the US).

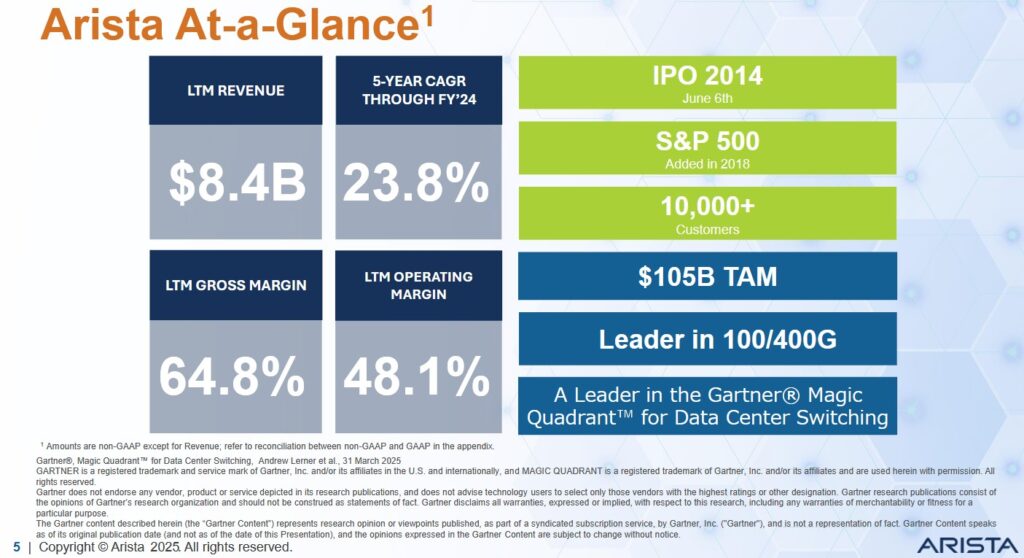

In the first 3 quarters of FY2025, ANET’s revenue was $6.517B which pales in comparison to some of its largest competitors.

- NVDA’s revenue for the first 3 quarters of the current fiscal year was $147.811B.

- In the fiscal year that ended on July 26, 2025, CSCO’s annual revenue was $56.654B.

- HPE’s revenue is the first 3 quarters of FY2025 was $24.617B.

While CSCO and HPE are profitable, their margins are typically lower than ANET’s. The reason ANET’s growth is outpacing some of its competitors is that it focuses on high-end, software-driven data center switching. CSCO’s and HPE’s business models include lower-margin legacy businesses, service provider equipment, and a heavier services component.

Business Overview

ANET is an industry leader in data-driven, client-to-cloud networking for large AI, data center, campus and routing environments. Its platforms deliver availability, agility, automation, analytics, and security through an advanced network operating stack.

A good overview of the company is found in Part 1 Item 1 in the FY2024 Form 10-K accessible through the SEC Filings section of the company’s website.

Financials

Q3 and YTD2025 Results

On November 4, ANET released its Q3 and YTD2025 results.

At the end of Q3 (September 30, 2025), ANET had cash and cash equivalents and marketable securities totaling ~$10.106B versus ~$8.304B at FYE2024 (December 31, 2024).

Total liabilities at the end of Q3 amounted to ~$6.142B of which ~$3.521B was current deferred revenue and ~$1.166B was non-current deferred revenue. If we deduct deferred revenue (funds received from customers prior to services being rendered), liabilities amount to ~$1.455B.

At FYE2024, total liabilities amounted to ~$4.049B of which ~$1.727B was current deferred revenue and ~$1.064B was non-current deferred revenue. If we deduct deferred revenue, liabilities amount to ~$1.258B.

While annual CAPEX is relatively low, developing products (research and development (R&D)) is expensive. Furthermore, the investment in product development typically involves a long payback cycle. These investments may take several years to generate positive returns, if ever.

In FY2019 – FY2024 and YTD2025, ANET incurred R&D expenses of ~$0.463B, ~$0.487B, ~$0.587B, ~$0.729B, ~$0.855B, ~$0.997B, and ~$0.889B.

ANET expects to continue to invest heavily in software development in order to expand the capabilities of its cloud networking platform and introduce new products and features. Results of operations will likely be impacted by the timing and size of these investments.

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX

In prior posts I touch upon my rationale for deducting stock-based compensation (SBC) to calculate FCF. I, therefore, dispense with explaining this again.

The following compares ANET’s FCF using the ‘conventional’ and ‘modified’ calculation methods.

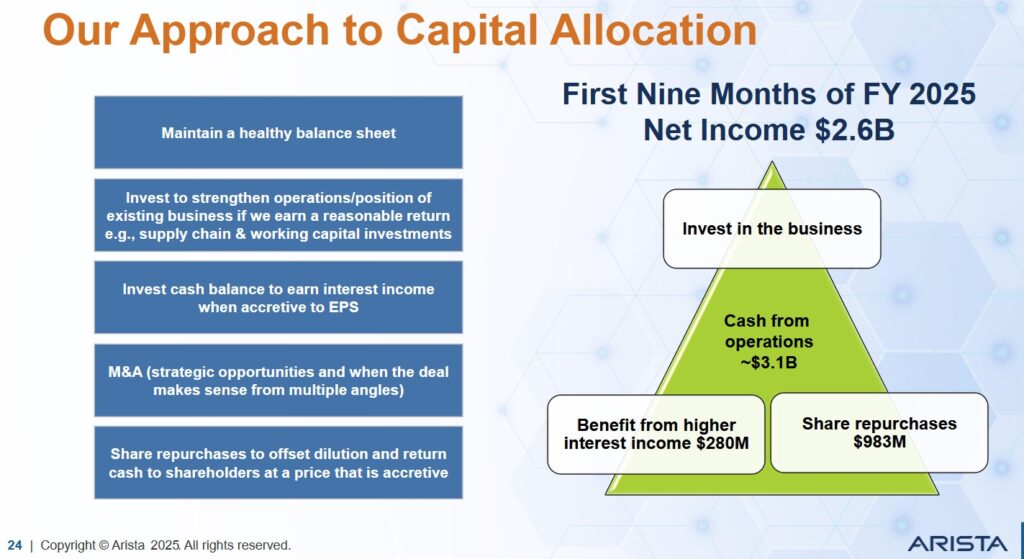

Capital Allocation

The following reflects ANET’s capital allocation priorities.

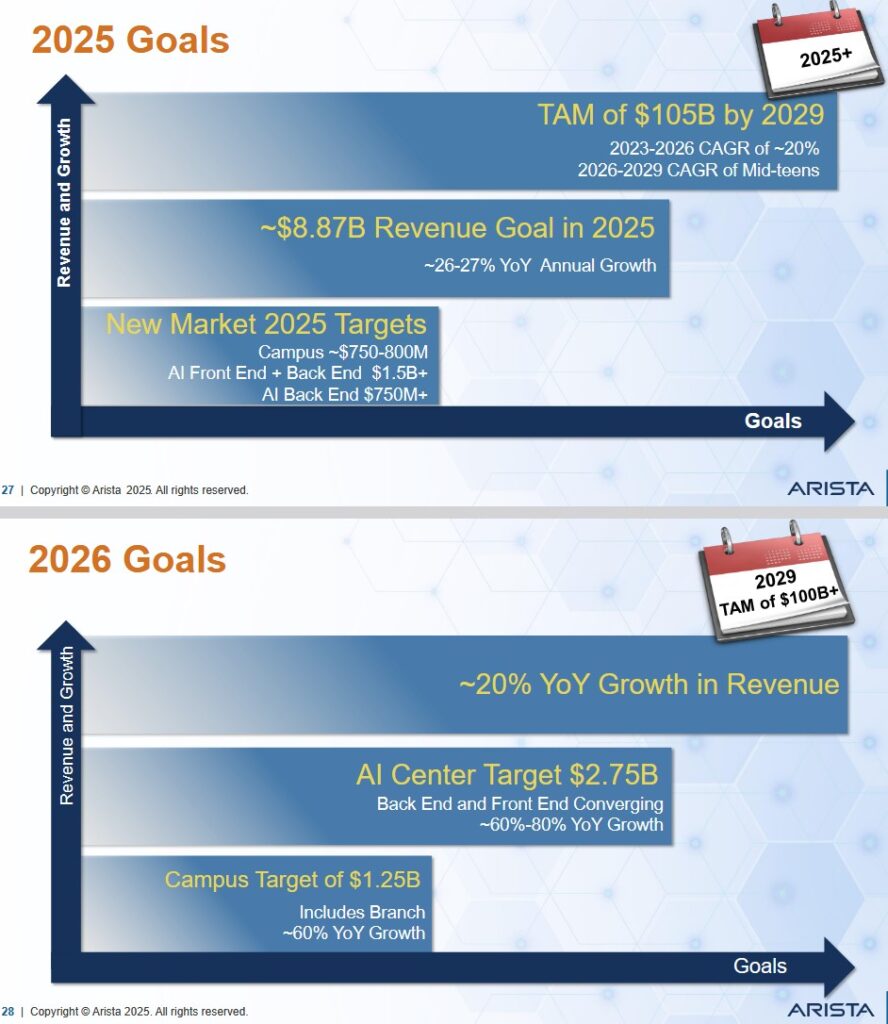

Q4 and FY2025 Goals and Preliminary FY2026 Goals

ANET’s Q4 2025 revenue outlook is ~$2.3B – ~$2.4B. The gross and operating margin forecast is ~62% – ~63% and ~47% – ~48%.

The effective tax rate is expected to be ~21.5% and management forecasts ~1.281 billion diluted shares (an increase from 1,276.6 billion in Q3 2025).

The FY2025 revenue growth outlook is ~26% to 27% or ~$8.87B at the midpoint with the FY2025 gross margin outlook at ~64%, inclusive of possible known tariff scenarios.

Management anticipates a ~48% operating margin.

The following reflects ANET’s FY2025 and FY2026 goals.

The preliminary outlook for FY2026 is:

- Revenue growth of ~20%;

- Revenue growth of ~20%, or ~$10.65B.

- Gross margin of ~62% – ~64%; and

- Operating margin of ~43% – ~45%.

Risk Assessment

ANET has no debt to rate.

Dividends and Share Repurchases

Dividend and Dividend Yield

Page 19 of 181 in the FY2024 Form 10-K reflects the following:

We have not paid dividends in the past and do not intend to pay dividends for the foreseeable future.

Stock Splits

ANET initiated a 4:1 stock split on November 18, 2021 and another 4:1 stock split on December 4, 2024.

Share Repurchases

A concern I have with ANET is the growth in its annual SBC. The company, however, repurchases shares that more than offset the number of shares being issued as part of its various employee compensation packages (see table presented in the Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX section of this post).

In May 2025, ANET completed repurchases under its prior $1.2B stock repurchase program and its Board authorized a new $1.5B stock repurchase program. This authorization allows ANET to repurchase shares of its common stock that will be funded from working capital.

ANET did not repurchase any shares during the quarter ended September 30, 2025. On page 15 of 64 in the Q3 2025 Form 10-Q we see the following:

As of September 30, 2025, the remaining authorized amount for repurchases under the new repurchase program was $1.4B.

Valuation

On December 2, 2025, I initiated a position @ $127.505. In the first 9 months of FY2025, it generated $2.00 EPS. While ANET does not provide diluted EPS guidance for the year I conservatively estimate it will generate ~$2.70 for the year despite the anticipated increase in outstanding shares. Using this estimate, the forward diluted PE is ~47.22.

Using my purchase price and the currently available adjusted diluted EPS broker estimates, ANET’s forward adjusted diluted PE levels are:

- FY2025 – 24 brokers – ~44.43 using a mean of $2.87 and low/high of $2.69 – $2.91.

- FY2026 – 24 brokers – ~38.18 using a mean of $3.34 and low/high of $3.09 – $3.71.

- FY2027 – 19 brokers – ~31.8 using a mean of $4.01 and low/high of $3.53 – $4.45.

I place very little reliance on broker estimates as much can happen to make these estimates irrelevant. Furthermore, the disparity in estimates implies that the brokers which cover ANET have very different outlooks.

Conventional FCF Calculation

In the first 9 months of FY2025, ANET generated $2.373 of FCF calculated using the conventional method of calculating FCF. If I extrapolate the YTD FCF for the first 9 months of the year, ANET should generate another $0.791 of FCF in Q4 2025 ($2.373/3 = $0.791). Adding $2.373 and $0.791 we get $3.164. If I give this a margin of safety and estimate ANET will generate ~$3.10 of FCF for the year, the forward P/FCF is ~41.

Modified FCF Calculation

In the first 9 months of FY2025, ANET generated $2.133 of FCF calculated using the modified method of calculating FCF. If I extrapolate the YTD FCF for the first 9 months of the year, ANET should generate another $0.711 of FCF in Q4 2025 ($2.133/3 = $0.711). Adding $2.133 and $0.711 we get $2.844. If I give this a margin of safety and estimate ANET will generate ~$2.78 of FCF for the year, the forward P/FCF is ~45.9.

These valuation appear to be high. ANET, however, is growing rapidly and generates strong margins. The company is also debt free and strategically repurchases shares thus ‘increasing my share of the company’.

Final Thoughts

ANET is up against much larger competitors but is gaining market share.

While not a capital intensive business from a CAPEX perspective, it must spend a considerable amount annually on research and development. Some of this expense may lead to no/miminal meaningful revenue, and therefore, I like that the company has no debt. On the contrary, it receives funds from customers prior to rendering services (~$4.687B in total deferred revenue at the end of Q3 2025).

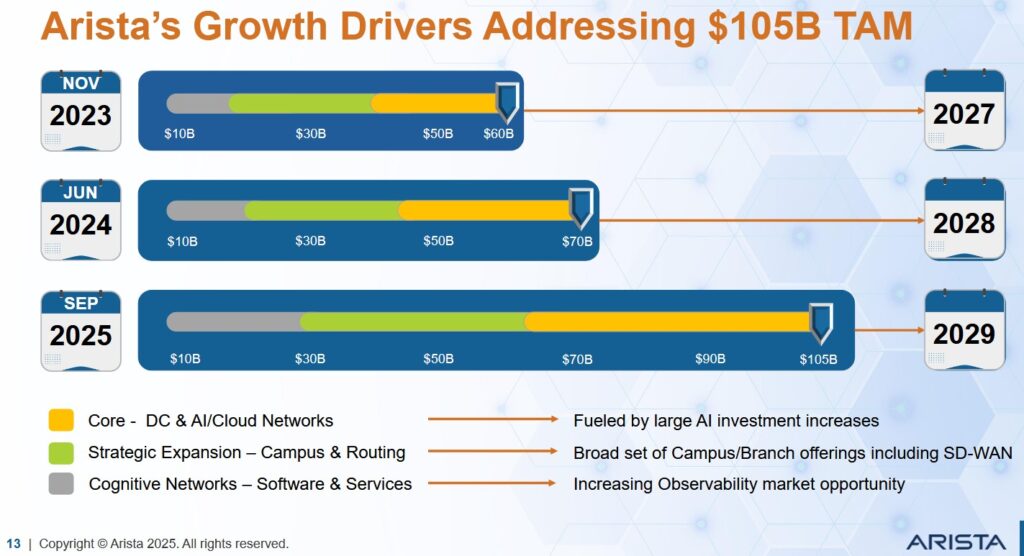

The company estimates the total addressable market should be ~$105B by 2029. If it captures a 20% market share by 2029, its annual revenue in 2029 should be ~$21B. In comparison, the company’s 2025 revenue goal is $8.87B. Doubling annual revenue by 2029 appears to be reasonable.

Being cautious, I estimate that the TAM in 2029 will be $90B and ANET will only capture a 15% market share. Using these assumptions ANET could generate ~$13.5B of annual revenue in FY2029.

The Operating Margin over the last 12 months is ~48.1%. If the ~$105B 2029 TAM materializes, the Operating Margin drops to 40%, and ANET captures a 15% market share, its operating income could be ~$6.3B (~$105B x 40% x 15%).

If the 2029 TAM drops to ~$90B, the Operating Margin drops to 40%, and ANET captures a 15% market share, its operating income could be ~$5.4B (~$90B x 40% x 15%). In comparison, ANET’s operating income in the first 3 quarters of FY2025 was ~$2.823B.

At first blush, I perceived ANET’s valuation to be rich. Stepping back and looking at the company’s:

- growth potential

- profit and FCF generating capabilities; and

- pristine Balance Sheet,

the current valuation seems reasonable.

My exposure is only 200 shares. I intend to acquire additional shares if the valuation improves.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long ANET.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.