I last reviewed Copart (CPRT) in this May 28, 2025 post at which time the most current financial information was for Q3 and YTD2025. I, however, disclosed in my June 18 Copart’s Valuation Improves post, an additional increase in my CPRT exposure.

With the release of Q4 and FY2025 results following the September 4 market close, I take this opportunity to revisit this existing holding.

Business Overview

CPRT, the largest online salvage vehicle auction operator in the US, was founded in 1982. Since 2003, however, all auctions are been online. By holding all auctions online, CPRT is able to connect buyers and sellers around the world.

In my May 28, 2025 post, I provide a brief business overview. I, therefore, dispense with another overview in this post.

Section 1 of CPRT’s Form 10-K provides a good overview of the company (refer SEC Filings). It has ~300,000 paying registered members from virtually every non-sanctioned country. International members account for ~40% of all vehicles sold at US auctions, comprising almost half of auction proceeds. This is because international buyers generally purchase vehicles that are more valuable than those acquired by domestic buyers.

The top 10 individual vehicle buyers collectively purchase a low single-digit percentage of all the vehicles sold at US auctions.

Financials

Q4 and FY2025 Results

CPRT’s financial results are available through the SEC Filings section of the company’s website. The FY2025 Form 10-K, however, is unavailable as I compose this post.

The company’s cash, cash equivalents, and restricted cash and investment in held to maturity securities increased to ~$4.789B at FYE2025 versus ~$3.422B at FYE2024 (July 31). This increase is despite FY2025 net CAPEX of ~$0.537B!

In addition to its cash, CPRT has an unused revolving credit facility of ~$1.2B.

Net cash provided by operating activities in FY2025 was ~$1.8B versus ~$1.473B in FY2024.

CPRT has much less tariff related exposure than just about every other US auto-related company.

FY2025 revenue and gross profit rose by 9.7% and 10.1%, respectively from FY2024 levels. FY2025 total operating expenses, however, rose ~10.7%.

Capital intensive companies (eg. railroads, auto manufacturers, etc.) often reflect annual depreciation and amortization that is somewhat comparable to annual CAPEX. Such highly capital intensive companies often rely on debt to finance their CAPEX requirements.

CPRT’s annual ‘purchases of property and equipment’ typically exceed annual ‘depreciation and amortization’ by a considerable margin on the Consolidated Statement of Cash Flows. It, however, has NO debt. What we have in CPRT, is a company that reinvests heavily to fuel future growth using cash flow and earnings generated from normal business operations. It does not need debt!

Mergers and Acquisitions

The company continually scours the globe for opportunities to enhance its service proposition. For the vast majority of companies CPRT would ever entertain acquiring, it could easily finance it either with the balance sheet or by taking on debt. Acquisitions, therefore, are not dependent on CPRT’s cash levels.

German Market

CPRT Germany updated its fee schedule in January 2025, making several pricing changes affecting members and buyers. Notable adjustments include increases in lot retrieval, document handling, and guest fees, along with a revised relist fee structure and a clear distinction between basic and premier membership costs.

By shifting some operational practices to more consignment-based auction models, CPRT can expand its margins and improve operational efficiency

Land Acquisition

In prior posts I touch upon the number of facilities CPRT has in various regions (see locations).

Property purchases during the year are reflected under ‘Purchases of property and equipment’ on the Consolidated Statements of Cash Flows.

CPRT continually expands its land capacity in the US and internationally and ensures it has adequate staffing levels so as to provide strong customer service on short notice. It emphasizes capacity expansion in areas that are susceptible to natural disasters.

In my prior post, I touch upon the acquisition of hundreds of acres of land in South Florida. In July, it acquired 33 acres of undeveloped land near its existing facility in Franklin, Wisconsin for ~$2.3 million.

The company typically incurs a loss in areas affected by a severe natural disaster as labor and sub-haul costs exceed revenue from additional vehicle volume. Management is prepared to incur a short-term loss so it can provide excellent customer service thus enabling it to foster stronger insurance relationships and future volume growth. This strategy has proven to be highly successful.

The land CPRT acquires does not serve much purpose unless there is the appropriate infrastructure to operate a yard. These infrastructure investments are a significant component of the property and equipment expenditures.

Given the number of CPRT locations, it is impressive that CPRT can fund its property and equipment needs without availing itself of debt.

Q4 2025 Earnings Call Transcript

The following is CPRT’s CEO commentary from the Q4 2025 earnings call which addresses key topics that impact CPRT’s performance and outlook.

Accident frequency has declined virtually every year since Copart’s inception and almost certainly for decades preceding that. These declines have generally occurred very gradually as new safety technologies such as anti-lock brakes in the 1970s and 1980s penetrate the installed base with each vintage of newly manufactured vehicles. Over those same long-term horizons, however, total loss frequency has generally increased at a rate far exceeding the decline in accident frequency itself. And in fact, for the quarter, total loss frequency has continued its long-term upward trend consistent with, again, the entire history of our company. In the United States, total loss frequency for the second calendar quarter of 2025 was 22.2%, up from 21.5% in the same quarter in 2024.

As vehicle complexity increases, parts and labor cost increase as well. We’ve also talked at length about how total loss itself becomes more attractive as growing economies seek more and more U.S. salvaged vehicles to satisfy their demand for more mobility.

On recent earnings calls, we’ve talked at great length about the importance of our differentiated service offerings, including our efforts to help insurance companies mitigate their advanced charges, the decision support tools we provide to help them make calls quicker and better as well as a range of titling and loan payoff services we offer to them. But we also know that, above all else, the critical value we provide sellers at Copart is that our auction platform will find the highest and best use of every vehicle anywhere in the world.

Capital Allocation Strategy

CPRT doe not distribute a dividend. Reinvesting in the business is CPRT’s capital allocation priority with share repurchases ranking second.

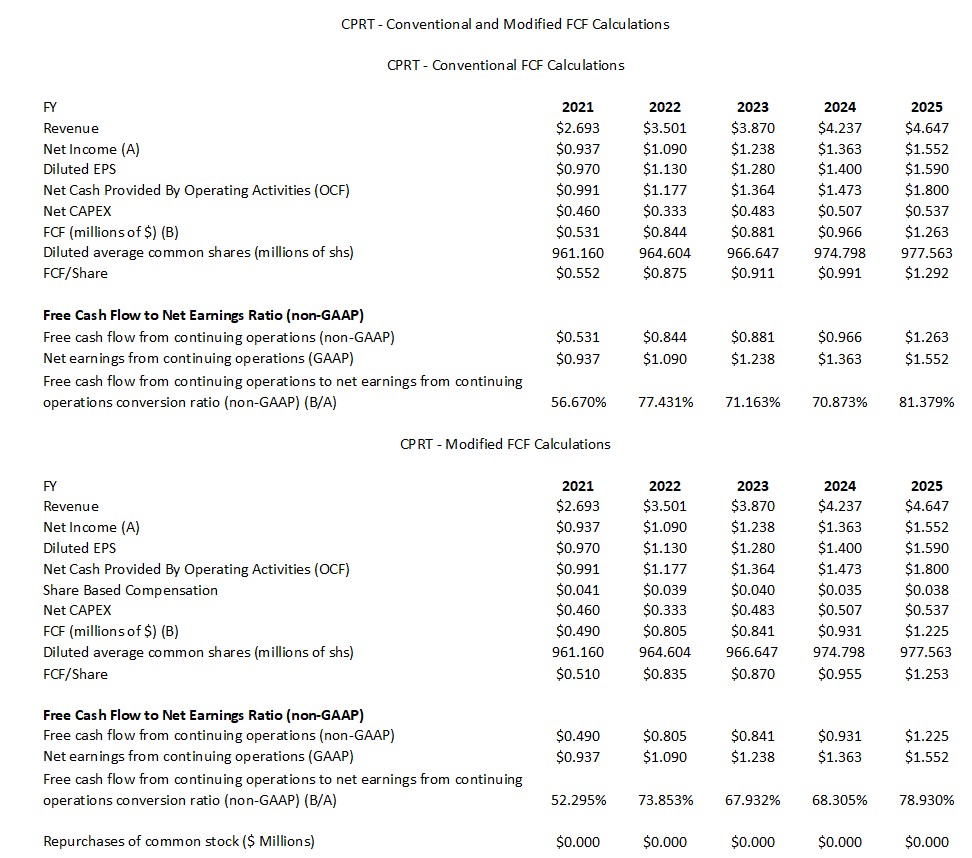

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX

In various prior posts, I deduct stock-based compensation (SBC) when determining a company’s net cash provided by operating activities. This is particularly important when a significant component of a company’s employee compensation is in the form of SBC.

Let’s suppose a company grants a significant number of company shares to employees as part of its various compensation packages. This form of remuneration is not reflected on the Income Statement to determine Net Earnings. If the company did not grant this SBC, however, you would think it would need to boost salaries/wages in order to retain its employees. These higher wages/salaries WOULD be reflected within the Income Statement thus having an impact on earnings.

Some investors may resort to the argument that a company is issuing shares to its employees but is often offsetting these new shares by repurchasing an equal or greater number of shares.

Having looked at countless Form 10-Ks over the years, I see companies granting stock options at prices that are often far below current share prices. So….you have a company repurchasing a boatload of shares at $X but it is issuing shares to employees (with a significant component to senior management) at a small fraction of $X. As a retail investor with an insufficient number of shares to sway the decision making at the Board level, I have no choice but to watch my investment in a company being eroded while insiders and employees are being enriched.

CPRT is unlike companies in the technology sector that have a substantial component of its employee remuneration in the form of share-based compensation. It issues shares to its employees but the annual SBC is negligible. This explains the reason for the moderate FCF variance using the conventional and modified calculation methods.

In FY2025, net cash provided by operating activities was ~$1.8B. Subtract ~$0.032B in Proceeds from sale of property and equipment from Purchases of property and equipment (~$0.569B) and we get Net CAPEX of $0.537B thus giving us FY2025 FCF of ~$1.263B.

I previously forecast FY2025 diluted weighted average common shares outstanding of ~980 million. The actual total was 977.563 million.

FY2025 Outlook

CPRT does not provide any outlook.

Risk Assessment

CPRT has no debt to rate.

Dividend and Dividend Yield

CPRT has not paid a cash dividend since becoming a public company in 1994.

Stock Splits

Since becoming a shareholder on January 18, 2022, CPRT has had two 2 for 1 stock splits (November 3, 2022 and August 21, 2023).

In FY2013 – FY2025, CPRT’s weighted average number of outstanding shares (in millions of shares rounded) was 1,038, 1,050, 1,051, 977, 948, 968, 962, 955, 961, 965, 967, 975, and 978.

On September 22, 2011, CPRT’s Board authorized a 320 million share increase in the stock repurchase program, bringing the total current authorization to 784 million shares.

On the Q4 2025 earnings call, management states that over the long-term, share buybacks will likely remain the mechanism by which the company will return cash to shareholders. The last time CPRT repurchased any shares, however, was in FY2019 when it repurchased $364.997 million. CPRT has subsequently opted to reinvest in the company to fuel growth.

Valuation

In FY2025, CPRT generated $1.59 in diluted EPS. As I compose this post on September 8, the share price is ~$47.88 giving us a PE of ~30.1.

Based on the annual diluted EPS growth in FY2021 – FY2025, I estimate CPRT’s FY2026 diluted EPS will be ~$1.72. This ~$0.13 increase from the FY2025 level is roughly the average annual diluted EPS increase in FY2021 – FY2025. Using my estimate and a ~$47.88 share price, the forward diluted PE is ~27.8.

Using the current broker estimates and share price, the forward-adjusted diluted PE levels are:

- FY2026 – 12 brokers – ~27.8 based on the mean of $1.72 and low/high of $1.65 – $1.80.

- FY2027 – 12 brokers – ~25.2 based on the mean of $1.90 and low/high of $1.80 – $2.09.

NOTE: These broker estimates are likely to be revised over the next several days.

In FY2025, CPRT generated $1.292 and $1.253 of FCF calculated using the conventional and modified methods (see Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX section in this post) resulting in a P/FCF of ~37 and ~38.2.

Looking at CPRT’s FCF trend over the past few years, it is not unreasonable to expect ~$1.30 of FCF in FY2026. At this level, the current P/FCF is ~36.8.

In my May 28, 2025 post, I reflect the following:

In the first 3 quarters of FY2025, CPRT generated $1.18 EPS versus $1.07 in the same period in FY2024.

Using the current broker estimates and my May 28 ~$52.13 purchase price, the forward-adjusted diluted PE levels are:

- FY2025 – 11 brokers – ~33.4 based on the mean of $1.56 and low/high of $1.52 – $1.64.

- FY2026 – 11 brokers – ~29.9 based on the mean of $1.75 and low/high of $1.65 – $1.91.

- FY2027 – 6 brokers – ~26.3 based on the mean of $1.98 and low/high of $1.80 – $2.23.

As noted earlier, I estimate CPRT will generate ~$1.20 and ~$1.16 of FCF in FY2025 calculated under the conventional and modified methods. Using my recent ~$52.13 purchase price, CPRT’s P/FCF is ~43.4 and ~45.

CPRT’s valuation appears rich until we consider its dominant industry position, fortress balance sheet, and growth opportunities. Many investors, however, may have no interest in CPRT because:

- the industry is unappealing;

- it issues no dividend; and/or

- it is not a technology company.

While CPRT is not a technology company, it has revolutionized the salvage industry by employing technology.

Final Thoughts

At FYE2025, CPRT had ~$4.8B in cash and held-to-maturity securities, a ~$1.2B revolving credit facility, and $0 debt. The strength of CPRT’s Balance Sheet provides it with several options to enhance shareholder value. It can continue to reinvest in the company to further distance itself from the competition and/or it can repurchase shares to offset the increase in the weighted average number of shares outstanding that has transpired over the past several years.

If a decision is made to repurchase shares, existing shareholders should WANT CPRT’s share price to remain depressed. With any luck, CPRT will remain attractively valued for a prolonged period thus providing management with ample opportunity to repurchase a significant number of shares without the risk of these repurchases driving up the share price.

Based on the currently available information, I think a fair valuation is ~$55. This represents a ~14.9% return (($55 – $47.88)/$47.88) if the share price appreciates to the ~$55 level.

I currently hold 3200 shares in ‘Core’ accounts and 940 shares in ‘Side’ accounts in the FFJ Portfolio and it was my 16th largest holding when I completed my 2025 Mid-Year Portfolio Review. Young investors I am helping on their journey to financial freedom also have CPRT exposure.

Despite shares being undervalued, I am satisfied with my current exposure and do not intend to acquire additional shares.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long CPRT.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.