In my June 3, 2025 post, I disclose my rationale for initiating a 500 share position in Howard Hughes Holdings (HHH) in one of the ‘Core’ accounts in the FFJ Portfolio. I subsequently increased my exposure to 1000 shares and disclosed this in my June 9, 2025 post; my average cost is ~$67.90.

In this brief post, I provide an update on HHH’s transformation progress.

Business Overview

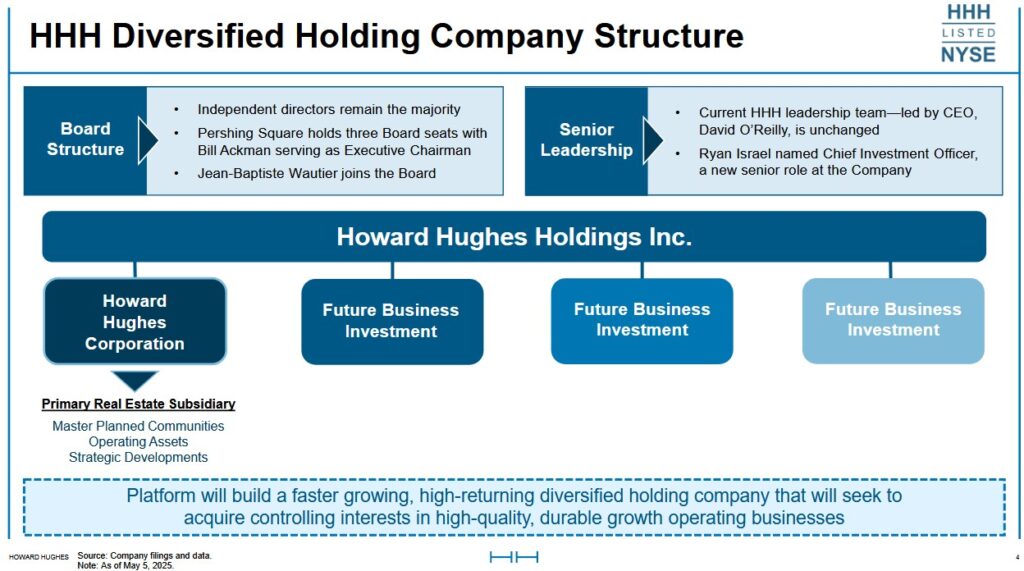

HHH operates through three business segments: Operating Assets, Master Planned Communities (MPCs), and Strategic Developments. It owns and operates one of the US’s largest portfolios of MPCs spanning ~101,000 gross acres, as well as operating properties, strategic developments, and other assets across five states (Texas, Nevada, Arizona, Hawaii, and Maryland).

As noted in my June 3 post, the HHH of the future will differ significantly from the HHH of the past.

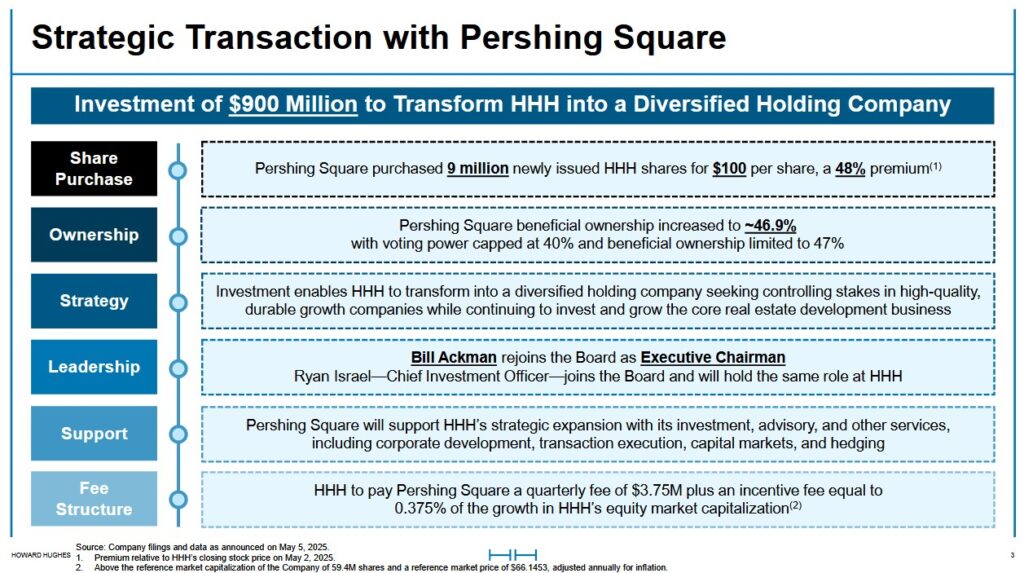

The reason for the change is that Pershing Square Holdco, L.P. and its wholly owned subsidiary, Pershing Square Capital Management, L.P. recently invested $0.9B in HHH with plans to transform it into a diversified holding company.

Despite this impending transformation, investors should review the company’s website and Part 1 Item 1 in the FY2024 Form 10-K to understand the current nature of HHH’s business operations given that the existing HHH will remain a key component of the ‘new’ HHH.

A series of videos on the HHH website provide a good overview of HHH’s current operations.

Pershing Square’s comprehensive presentation pertaining to the increase in its HHH investment is accessible here.

When I wrote my June 3 post, there was some thought of creating an insurance company versus acquiring an insurance company. On the Q2 2025 earnings call, however, Bill Ackman (Founder and CEO of Pershing Square Capital Management) disclosed that the recent principal focus has been in identifying and doing due diligence on a potential insurance company acquisition.

This has been a very high priority because a well managed insurance business is a cash generative business. It will write an insurance policy and will receive cash upfront which can then be invested. If the company is well managed, the premiums can be invested to generate very attractive returns on equity over a long period of time. If done properly, HHH should be able to grow at an attractive rate over time without having to raise equity capital.

A typical insurance company writes about as much premium as equity capital every year. It then invests this ‘float’ primarily in fixed income investments. It, however, uses a fair amount of leverage to get an attractive return. A balance sheet structure for insurance operation typically has ~3x the assets relative to equity. These assets are, for the most part, invested in low risk fixed income securities.

The plan, however, is to run a very low leverage insurance company. Instead of writing premiums equal to equity every year, the plan is to write premiums equal to 20% – 40% of equity in any one year. 100% of the insurance premium float will be invested in very low risk assets (eg. very short term US treasuries). Roughly 100% of the equity of the insurance operation, however, will be invested in common stocks of very high quality durable growth companies of the kind that Pershing Square has identified and invested in over time.

This is different from the typical insurance company. Typically, insurance companies do not have the investment skills on the common stock side and they tend to focus on maximizing the profitability of the insurer.

On the Q2 2025 earnings call, Bill Ackman states:

The asset side of the balance sheet is a bit of an afterthought. And part of that is insurance companies have difficulty recruiting, kind of best in class talent to run a successful, investment operation, particularly one that invests in equities. One of the things that we bring to this transaction with Howard Hughes is an investment operation, and that investment operation comes for free, if you will, to the insurance subsidiary. So the plan would be we acquire insurer, we run it at a low leverage insurer. We’re conservative, extremely conservative in the way we invest the insurance company float. And then Pershing Square, Pershing Square team invests, the, assets of that insurance the assets equal to about the equity of the insurer, in a common stock portfolio that we manage for the company, for free.

Financials

Q2 and YTD2025

On August 6, 2025, HHH released its Q2 and YTD2025 results.

With the plan to acquire an insurance company as opposed to building one from scratch, we should see an acceleration in HHH’s transformation. There is, therefore, little point in reviewing HHH’s historical results as they are not indicative of future performance.

The historical financial results, however, are accessible here if you wish to review them.

Risk Assessment

S&P Global last reviewed HHH on May 29, 2025 and affirmed its B rating with a stable outlook. This is the middle tier of the highly speculative non-investment grade ratings.

Fitch last reviewed HHH on March 20, 2025 and affirmed its BB rating. This is the middle tier of the non-investment grade speculative non-investment grade ratings.

Moody’s continues to reflect a Ba3 rating for The Howard Hughes Corporation; this rating was downgraded from Ba2 on April 25, 2023. On August 11, 2023, however, Howard Hughes Holdings Inc., a new holding company, replaced The Howard Hughes Corporation (HHC) as the public company trading on the New York Stock Exchange (NYSE). Existing shares of common stock of HHC were automatically converted, on a one-for-one basis, into shares of common stock of HHH, with the same designations, rights, powers, and preferences, and the same qualifications, limitations, and restrictions, as the shares of HHC common stock immediately prior to the reorganization.

Despite Pershing Square’s significant equity infusion, it appears the 3 rating agencies are adopting a ‘wait and see’ attitude before revisiting the current ratings.

Interestingly, S&P Global upgraded Pershing Square Holdings Ltd.’s domestic long-term credit rating to A- from BBB+ on May 20, 2025 with a stable outlook. Fitch affirmed its BBB+ long-term issues default rating at BBB+ on February 28, 2025.

I avoid companies whose long-term domestic issuer credit ratings are ‘junk’. Based on Bill Ackman’s vision for HHH, however, I anticipate credit rating upgrades to investment grade within 2 years.

Dividend and Dividend Yield

HHH distributes no dividend. A dividend distribution in the foreseeable future is unlikely.

The vision is to transform HHH into a diversified holding company by acquiring controlling stakes in high-quality, durable growth public and private operating companies while continuing to invest in and grow the Company’s core real estate development and MPC business. Share repurchases are unlikely in the foreseeable future.

Valuation

There is little point in trying to determine HHH’s value given that it is about to undergo a radical transformation. It is, however, reassuring that Pershing Square’s acquisition of $0.9B of newly issued HHH common stock for $100.00/share was for a ~48% premium of HHH’s closing share price on Friday, May 2, 2025.

Final Thoughts

My decision to invest in HHH was made primarily because of Bill Ackman’s track record of success. I also take comfort that my average cost is 67.9% of Pershing Square’s $100 purchase price.

Ackman and his team at Pershing have taken a page from Berkshire Hathaway (BRK). BRK began as a merger between two New England textile companies, Hathaway Manufacturing Company (incorporated in 1888) and Berkshire Fine Spinning Associates (formerly Berkshire Cotton Manufacturing Company) in 1955. In 1962, Warren Buffett began buying shares and ultimately gained control in 1965. Under Buffett’s leadership, BRK shifted away from textiles and into a diversified holding company with investments in insurance, railroads, energy, and various other industries.

Ackman’s vision is to transform HHH into a diversified holding company much like Buffett’s did with BRK. The plan is to acquire an insurance company; a number of insurance company acquisition opportunities are presently under review. On the Q2 2025 earnings call, Ackman states the hope is to announce a transaction by the Fall of 2025 and preferably by September 30 at which time HHH’s Annual General meeting will be held.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long HHH and BRK-b.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.