Following the release of Accenture’s (ACN) Q3 and YTD2025 results on June 20, 2025, the share price plunged to ~$284 from the prior day’s ~$306.50 closing share price. This prompted me to look at its results and outlook. Based on my analysis, I initiated a 200 share position @ ~$284.58 in one of the ‘Core’ accounts in the FFJ Portfolio. In addition, two young investors on their journey to financial freedom acquired ACN shares at a similar price.

In several previous posts, I indicate my desire to acquire shares in great companies that are experiencing/likely to experience short-term headwinds. Such companies typically fall out of favor with short-term investors thus often leading to share price weakness and an improvement in their valuation. For the majority of the last few years, ACN’s valuation has been ‘rich’. Just recently, however, its valuation has retraced to a ‘fair’ level.

There is no disputing that increased economic volatility and geopolitical uncertainty are likely to present near-term challenges. Investors should, therefore, anticipate a soft bookings trend for both ACN’s consulting and managed services segments. My intention is to increase my exposure should ACN experience ‘soft’ results and its valuation improve further.

For now, I provide my thoughts on why I have added ACN to the FFJ Portfolio.

Business Overview

ACN is a leading global professional services company that provides a broad range of services and solutions across Strategy & Consulting, Technology, Operations, Industry X, and Song. An explanation of each is found in the FY2024 Form 10-K that is accessible through the SEC Filings section of the company’s website. Further details regarding its capabilities and the industries it serves is found on the company’s website.

On ACN’s Q3 earnings call, however, it noted that artificial intelligence (AI) presents the firm with the greatest opportunity for creating new demand. In order to maximize AI’s potential, ACN is consolidating its Strategy and Consulting, Song, Technology, and Operations services into a single unit known as ‘Reinvention Services’ starting September 1, 2025.

- ACN is working with Italian shipbuilding company Fincantieri to launch the first AI-powered ship in 2025 which will be able to ‘predict its maintenance, manage its energy use on its own, and talk to the dock’ before it arrives at its destination;

- It is working to modernize the manufacturing process for Bel, maker of Laughing Cow cheese;

- It is collaborating with Brazilian mining company Vale to expedite environmental licensing and permits;

- ACN is creating AI-generated 3D avatars of physical products for coffee brands like Nescafé, Dolce Gusto, and Nespresso to reduce the time and cost of developing marketing campaigns.

ACN serves clients in three geographic markets:

- the Americas (51%);

- EMEA (Europe, Middle East and Africa) (35%); and

- Asia Pacific (14%).

These percent of revenues are for the 3 months ending May 31, 2025.

The company combines its strength in technology and leadership in cloud, data and artificial intelligence (AI) with unmatched industry experience, functional expertise and global delivery capability to help the world’s leading businesses, governments and other organizations build their digital core, optimize their operations, accelerate revenue growth and enhance citizen services.

ACN employed ~791,000 employees in Q3 2025 and had operations in more than 120 countries. This workforce level is down from a record 801,000 at the end of February as staff are leaving voluntarily.

Relatively recently, ACN has established a new location adjacent to a highway I periodically travel. Upon further investigation, I learned that the ACN location in question houses part of Eclipse Automation’s operations; ACN acquired Eclipse in August 2022. Eclipse’s website provides a good overview of the company’s capabilities.

Exhibit 21.1 in the FY2024 Form 10-K pages 137 – 153 reflects ACN’s subsidiaries at FYE2024.

Research and Development

I view ACN as the best-of-breed IT services company. This is thanks to its prominent reputation, established customer base, and deep technological expertise.

In order to remain at the forefront, ACN invests heavily in research and development (R&D). In FY2020 – FY2024 , R&D expenses were $0.871B, $1.118B, $1.123B, $1.299B, and $1.150B.

Capital Expenditures

Given the magnitude of ACN’s international operations, it is not surprising that it incurs significant annual CAPEX. Purchases of property and equipment in FY2020 – FY2024 amounted to $0.599B, $0.58B, $0.718B, $0.528B, and $0.517B. In the first 3 quarters of FY2025, ACN invested $0.492B.

Annual purchases of businesses and investments (net of cash acquired) are even more significant. In FY2020 – FY2024, ACN invested $1.532B, $4.171B, $3.448B, $2.531B, and $6.583B. In the first 3 quarters of FY2025, ACN invested $0.790B.

Financials

Q3 and YTD2025 Results

ACN’s Q3 and YTD2025 results are reflected in the Form 8-K and Q3 2025 Form 10-Q that were uploaded to the SEC Filings section of ACN’s website on June 20.

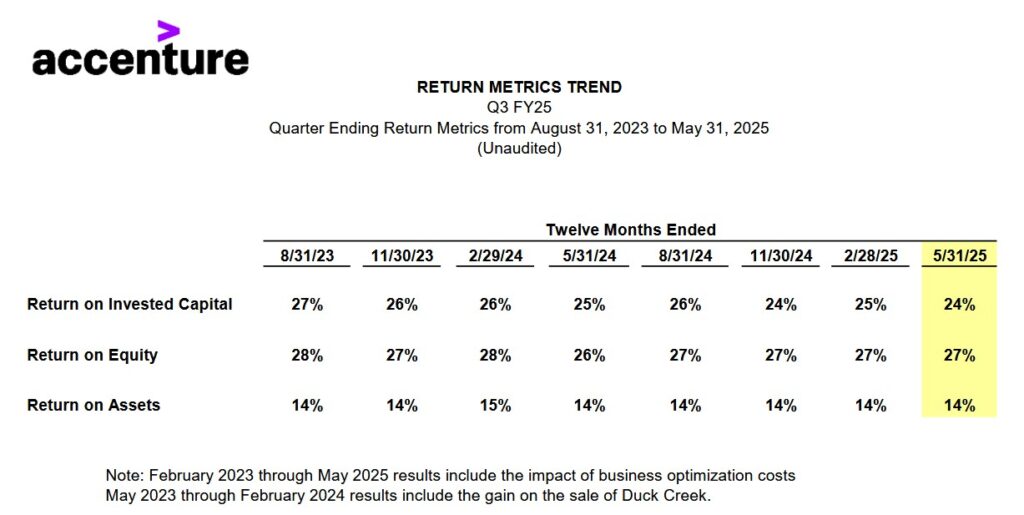

Additional important information, such as the following, is provided in supporting materials.

On the Q3 earnings call, ACN’s CEO stated:

We continue to see a significantly elevated level of uncertainty in the global economic and geopolitical environment as compared to calendar year 2024. In every boardroom, in every industry, our clients are not facing a single challenge. They’re facing everything at once: economic volatility, geopolitical complexity and changing customer behavior.

This elevated level of economic and geopolitical uncertainty is causing business leaders to hold off on hiring consultants for some new projects.

Slowdown At Accenture Federal Services

The US federal government accounts for ~8% of ACN’s revenues.

This segment of the company has contracts with the US government that have been affected by the Trump administration’s efforts to reduce spending. Existing contracts are being cancelled and a slowdown in new work present a headwind for revenue growth in Q4.

ACN is one of 10 consulting firms (Booz Allen Hamilton, Deloitte, Leidos, Ernst and Young, McKinsey, and Guidehouse are others) that was specifically asked to relinquish contracts or cut prices to save the government money. 28 ACN contracts have been ‘terminated for convenience’ since Trump’s inauguration in January. These include four large umbrella contracts that together authorize ~$1B in spending from the health and human services, interior and Treasury departments.

As evidence of the sharp slowdown in new work from the US Federal government, ACN is set to be paid $0.643B for work commissioned in Q3 2025 which is a little more than half in Q3 2024.

ACN states that it is premature to make assumptions about FY2026.

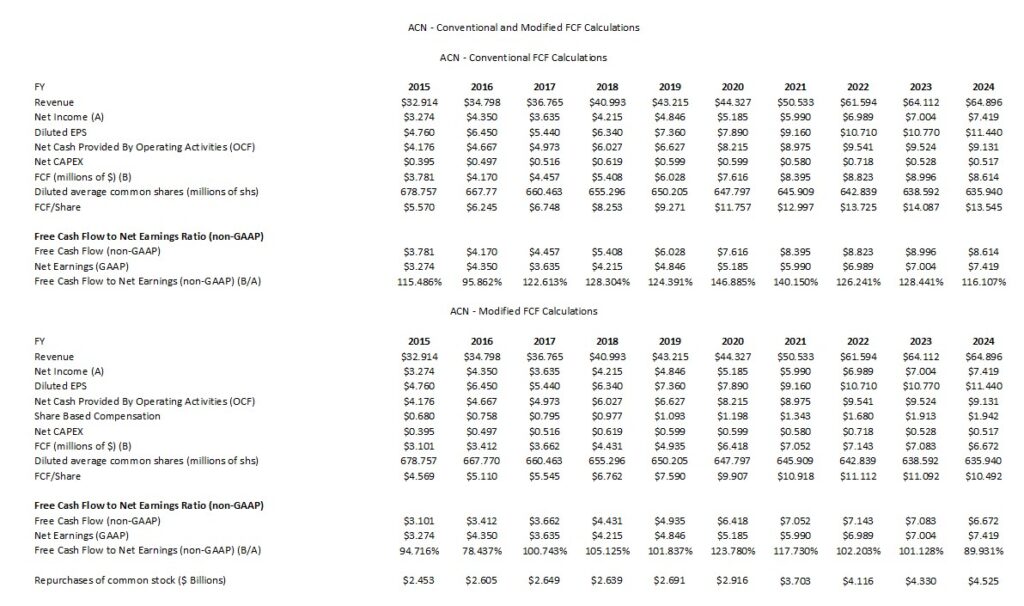

Conventional And Modified Free Cash Flow (FCF) Calculations (FY2015 – FY2024)

In my September 28, 2024 How Stock Based Compensation Distorts Free Cash Flow post, I touch upon how a company’s FCF can be distorted. In several subsequent posts, I take a conservative approach when looking at a company’s FCF.

FCF is a non-GAAP measure, and therefore, the manner in which it is computed is open to debate. Most companies subtract capital expenditures (CAPEX) from Net Cash Provided by Operating Activities found in the Consolidated Statement of Cash Flows. They do not, however, deduct share-based compensation (SBC). Given the magnitude of ACN’s SBC, I think it is prudent to deduct it.

We see that the magnitude of ACN’s SBC has a material impact on the company’s FCF.

In the first 3 quarters of FY2025, ACN’s Net Cash Provided By Operating Activities amounted to $7.56B and CAPEX was $0.492B giving us $7.068B YTD FCF calculated under the conventional method. YTD SBC is $1.654B thus lowering YTD FCF to $5.414B when calculated under the modified method.

ACN is aggressively repurchasing shares with $4.146B repurchased YTD2025; the diluted average common shares outstanding (Class A) is 630.457 million versus 635.94 million in FY2024. ACN also has 302,818 Class X shares outstanding at June 9, 2025. There is no trading market for Accenture plc Class X ordinary shares. As of September 30, 2024, there were 14 holders of record of Accenture plc Class X ordinary shares.

Every year, ACN’s income statement reflects a modest amount of Net income attributable to non-controlling interests in Accenture Canada Holdings Inc. and Net income attributable to non-controlling interests – other. ACN’s diluted EPS assumes the exchange of all Accenture Canada Holdings Inc. exchangeable shares for Accenture plc Class A ordinary shares on a one-for-one basis. The income

effect does not take into account ‘Net income attributable to non-controlling interests – other’,

since those shares are not redeemable or exchangeable for Accenture plc Class A ordinary shares.

The Net Income reported on the Consolidated Cash Flow Statements reflects the Net Income reported on the Income Statement BEFORE what is typically under $0.15B of net income attributable to non-controlling interest. In the grand scheme of matters, $0.15B is relatively immaterial. I, therefore, make no adjustment to the Net Income ACN reports on its Consolidated Cash Flow Statements.

FY2025 Outlook

ACN expects Q4 revenues to be $17B – $17.6B. This outlook includes a ~2.5% positive FX impact compared to Q4 2024. It also reflects an estimated 1% – 5% growth in local currency.

ACN’s US federal business experienced an immaterial impact to overall Q3 growth and the company’s best estimates now include a ~2% headwind in Q4.

The company currently expects FY2025 revenue to be 6% – 7% growth in local currency versus FY2024 with inorganic contribution for FY2025 being ~3%.

The FY2025 outlook calls for:

- ~$1B – ~$1.5B in acquisitions.

- an operating margin of ~15.6% which is 10 bps expansion over adjusted FY2024 results.

- an annual effective tax rate of ~23% – ~24% versus an adjusted effective tax rate of 23.6% in FY2024.

The current FY2025 diluted EPS outlook is $12.77 – $12.89 or 7% – 8% growth over adjusted FY2024 results.

FY2025 operating cash flow will likely be $9.6B – $10.3B (calculated without deducting SBC) and annual property and equipment additions will be ~$0.6B for a FCF range of ~$9B – ~$9.7B. This ‘conventional’ FCF guidance continues to reflect a free cash flow to net income ratio of 1.1 – 1.2.

Management expects to return at least $8.3B through dividends and share repurchases in FY2025. In the first 3 quarters of FY2025 it has returned ~$6.924B.

Risk Assessment

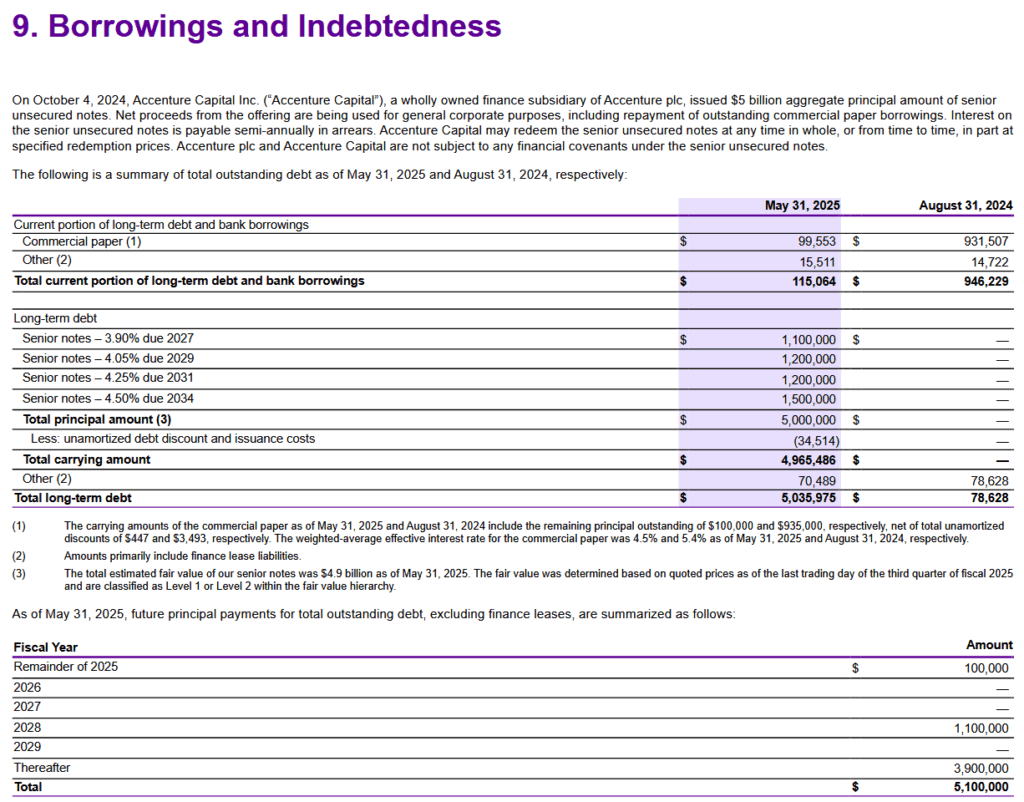

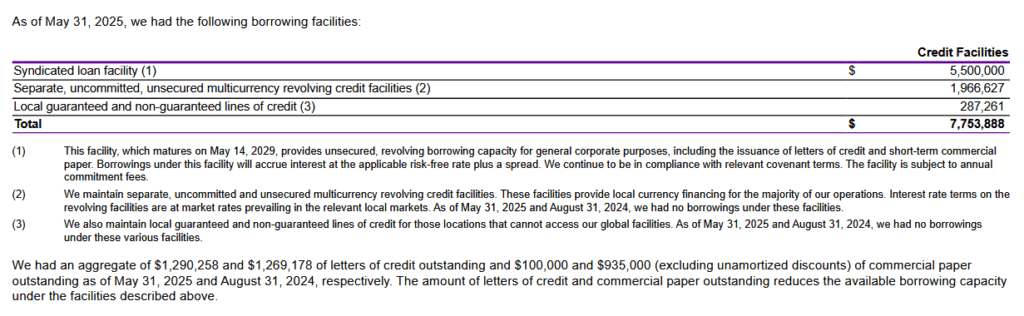

The potential return of an investment is important but so is the risk aspect. This is why I am particularly interested in the maturity schedule of a company’s long-term debt as well as the interest rates (amongst other things).

Unless ACN’s ability to generate strong cash flow takes a dramatic turn for the worse, meeting the staggered long-debt debt maturities should pose no issue.

ACN’s Aa3 long term issuer rating was affirmed by Moody’s on October 1, 2024 with a stable outlook. This is the bottom tier of the high grade investment grade category.

S&P last reviewed ACN on April 24, 2025 at which time it affirmed its AA- rating with a stable outlook. This is the bottom tier of the high grade investment grade category.

On October 1, 2024, Fitch affirmed ACN’s long term issuer default rating of A+ with a stable outlook. This is the top tier of the upper medium grade investment grade category. This rating is one tier lower than the ratings assigned by Moody’s and S&P Global.

Moody’s and S&P Global define ACN as having a very strong capacity to meet its financial commitments. It differs from the highest-rated obligors only to a small degree.

Fitch defines ACN as having a strong capacity to meet its financial commitments. It is somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

Dividends

ACN distributes a quarterly dividend (see history). Investors, however, would be wise not to fixate and/or invest based on dividend metrics. The focus should be on total potential shareholder return and the company’s ability to effectively allocate capital.

Share Repurchases

Looking at the table reflected in the Conventional And Modified Free Cash Flow (FCF) Calculations (FY2015 – FY2024) section of this post, we see that the diluted weighted average shares outstanding in FY2015 was 678.757 million. In FY2024, this had been reduced to 635.94 million. In Q3 2025, this had been further reduced to 630.457 million. This reduction is impressive considering the magnitude of the shares ACN issues as part of its various employee compensation packages (see SBC in each year).

Valuation

In the first 9 months of FY2025, ACN generated $9.90 of diluted EPS and the current FY2025 diluted EPS outlook is $12.77 – $12.89. Using my recent ~$284.58 purchase price, the forward diluted PE range is ~22.1 – ~22.3.

Using the current broker adjusted diluted EPS estimates, ACN’s forward-adjusted diluted PE levels are:

- FY2025 – 19 brokers – ~22.1 based on a mean of $12.88 and low/high of $12.81 – $13.02.

- FY2026 – 20 brokers – ~20.6 based on a mean of $13.80 and low/high of $13.48 – $14.16.

- FY2027 – 13 brokers – ~19 based on a mean of $14.97 and low/high of $14.37- $15.55.

Although I look at brokers’ earnings estimates, all estimates beyond the current fiscal year have no bearing on my investment decision making process. My reasoning is that I have no confidence that anybody can consistently and accurately determine a company’s performance as we go further out on the calendar. The variance in the brokers’ earnings estimates clearly indicates there is no consensus on ACN’s future performance.

EPS can also be distorted by various means. My preference, therefore, is to gauge a company’s valuation using FCF.

ACN’s FY2025 FCF outlook is ~$9B – ~$9.7B (calculated under the conventional method). In FY2023, FY2024 and Q3 2025, the diluted weighted average shares outstanding was 638.592 million, 635.94 million, and 630.457 million. ACN plans to acquire additional shares in Q4 so if the FY2025 weighted average is reduced to ~632 million, we can expect ACN’s FY2025 FCF/share to be ~$14.24 – ~$15.35. Using my recent ~$284.58 purchase price, the P/FCF is ~18.5 – ~20.

As noted earlier, however, my preference is to calculate P/FCF using the ‘modified FCF’ method which takes into consideration SBC.

ACN’s YTD2025 SBC is ~$1.654B or ~$0.551B/quarter. If ACN’s FY2025 SBC amounts to $2.205B (~$1.654B + ~$0.551B) and we deduct this from management’s ~$9B – ~$9.7B FY2025 FCF outlook, the FY2025 FCF is ~$6.795B – ~$7.495B. We arrive at FCF ~$10.75 – ~$11.86 when we divide this range by ~632 million shares. Using my recent ~$284.58 purchase price, the P/FCF is ~24 – ~26.5.

Final Thoughts

At ~$284.58, ACN’s valuation is fair. I would prefer, however, to acquire undervalued shares but ACN is very rarely undervalued.

I view ACN as one of the best professional services providers with a prominent reputation, established customer base, and deep technological expertise. The company has the capability/expertise to deliver end-to-end business solutions thus eliminating the need for customers to source different services from several suppliers which can potentially lead to project delays and cost overruns.

The US Federal government has expressed the need to reduce consulting expenditures which will impact ACN to some extent. The company, however, should fare better than many of its competitors given its expertise and diverse customer base.

As AI is introduced in the workforce, it poses significant threats to lower-end information technology (IT) services, such as infrastructure management and business process outsourcing. The reasoning is that AI is apt to perform better in handling repetitive and mechanical business processes. ACN’s strength, however, is in higher-end services (ie. consulting and system integration) since a relatively high level of human input is required to tailor solutions for customers.

I anticipate that ACN will remain a dominant player in the IT services industry. As noted earlier, ACN employs ~791,000 employees and has operations in more than 120 countries. If there is to be any industry consolidation, I envision ACN’s position of strength growing over time.

ACN’s annual revenue was relatively stagnant in FY2022 – FY2024 ($61.594B, $64.112B, and $64.896B). It has, however, generated $52.077B of YTD2025 revenue and the forecast is for an additional $17B – $17.6B in Q4. If this materializes, this would raise ACN’s FY2025 revenue to ~$69.077B – ~$69.677B. Despite increased economic volatility and geopolitical uncertainty that can lead to IT spending delays, ACN’s annual revenue in FY2030 could reach ~$80B – ~$82B.

ACN is a new holding and my current exposure is only 200 shares. It will not, therefore, come close to being a top 30 holding when I complete my 2025 Mid-Year End Review in early July. I do, however, like the company’s long-term outlook and short-term headwinds do not concern me. If ACN’s valuation improves, I hope to be in a position to increase my exposure. The same applies to the two young investors who also recently purchased ACN shares.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long ACN.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation. I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.