Contents

Summary

Summary

- This TELUS Corporation stock analysis is based on Q4 and FY 2016 financial results and 2017 projections released February 9, 2017.

- TELUS is Canada’s 3rd largest telecommunications company.

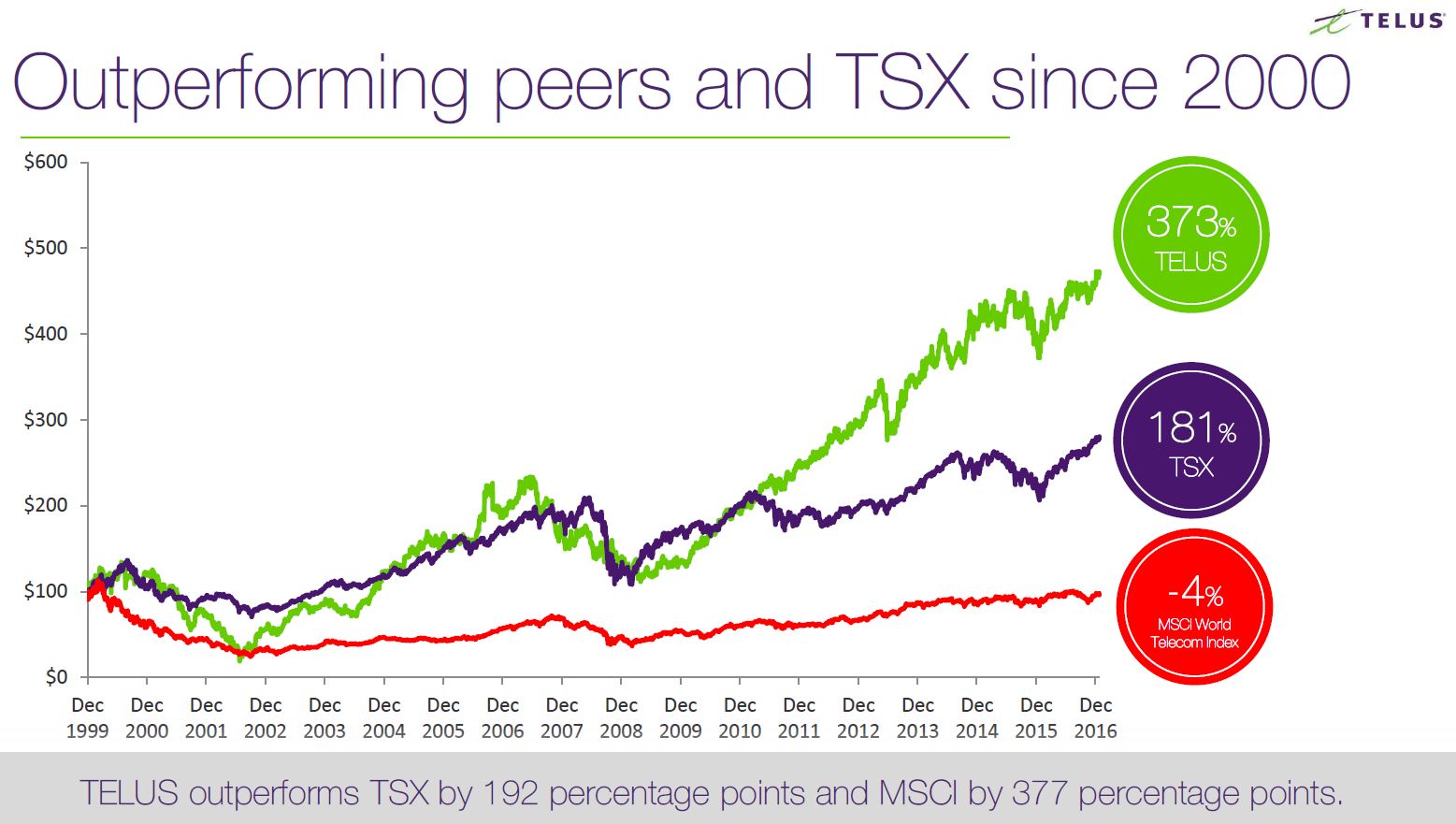

- It has outperformed its peers and the TSX from an overall return perspective over the past several years.

- It is currently investing heavily for sustainable L/T growth which has had negatively impacted debt levels and FCF. Management expects both to improve over the next few years.

- Management is projecting 5% EBITDA growth for FY2017 and 7 – 10% dividend growth over the next 3 - 4 years.

- While not on sale, TELUS represents a solid long-term investment at current levels with a dividend yield in excess of 4%.

Introduction

We currently own shares in BCE (NYSE: BCE) (TSX:BCE), AT&T (NYSE:T), and Verizon (NYSE:VZ). In this post I review TELUS (NYSE: TU) (TSX:T) to determine whether it would be a worthwhile addition to the telecommunications sector of our investment portfolio.

TU is Canada's 3rd largest telecommunications company and the incumbent in Alberta, British Columbia, and parts of Quebec. It is Canada’s fastest-growing national telecommunications company, with annual revenue of CDN $12.8B and 12.7 million subscriber connections. This total is comprised of 8.6 million wireless subscribers, 1.7 million high-speed Internet subscribers, 1.4 million residential network access lines, and more than 1.0 million TELUS TV customers.

It provides a wide range of communications products and services, including wireless, data, Internet protocol (IP), voice, television, entertainment and video, and is Canada's largest healthcare IT provider.

History

Large areas of rural Quebec, in particular the Gaspé Peninsula and the north shore of Québec, were served by an entity known as Corporation de Téléphone et de Pouvoir de Québec since 1927. This entity became known as Québec Téléphone in 1955.

In 1966, the Anglo-Canadian Telephone Company, a subsidiary of General Telephone and Electronics (GTE) of Stamford, Connecticut, became a majority shareholder in Québec Téléphone. Anglo-Canadian Telephone Company also owned BCTel.

In 1990, the government of Alberta formed TELUS Communications to facilitate the privatization of crown corporation Alberta Government Telephones Commission (AGT).

TELUS Communications acquired Edmonton Telephones Corporation (Ed Tel) from the City of Edmonton in 1995 thereby making Telus the sole provider of telephone service in Alberta.

Telus was introduced to the public as the consumer brand in 1996 thus replacing both AGT and EdTel.

The Telus and GTE-owned BCTel announced a proposed merger in 1998. This was completed in 1999 and the corporate name was slightly modified to Telus Corporation.

In 1997, Groupe QuébecTel was established to own Québec Téléphone. Following the merger of Telus in Alberta and BCTel, GTE sold its interests in Québec Téléphone to Telus in 2000. This entity was renamed Telus Québec in 2001.

Verizon, which had acquired GTE, sold to TU its 20.5% stake in TU in 2004.

Expansion Plans, 2017 Annual Targets, and Dividend Growth Plans

On March 27, 2017, Doug French, TU's EVP and CFO provided information on the company's expansion plans, 2017 annual targets, and dividend growth plans at Desjardins’ Industrials, Telecom & Consumer Conference.

The following are a few takeaways from his presentation.

- TU prefers to invest organically as opposed to undertaking major acquisitions. This provides it with more flexibility to ramp up or scale back CAPEX.

- TU is taking advantage of the low interest rate environment to fund its CAPEX initiatives. Peak leverage is expected to be reached in FY2017.

- The Debt Ratio (Net Debt to EBITDA which excludes restructuring and other costs) objective range is 2.00 – 2.50 times. Elevated CAPEX is expected to continue until 2020 – 2021 until such time as TU achieves the fiber footprint it desires. It, however, is expected to restore its Debt Ratio below the upper level of its objective range by FY2018.

- It is estimated that approximately 70% of TU’s shares are held by institutional investors and 30% by retail investors.

- TU’s employees are, collectively, the 5th largest shareholder in the company owning 2.8% of the total number of outstanding shares.

- TU has a postpaid wireless churn rate of less than 1% for 13 of the last 14 quarters. This level is significantly better than competitors.

- There are fewer customer complaints to The Commissioner for Complaints for Telecommunications Services (CCTS) by a substantial margin of all national carriers.

- In excess of one million premises in 86 communities across B.C., Alberta, and Quebec are ready to connect to TELUS PureFibre™ (fibre optic network).

- In 2016, TU signed 3 collective agreements for unionized team members in Canada. This provides cost certainty and stability to 2021.

The following historical results may have some appeal to investors seeking a relatively safe investment in a company with a strong history of dividend returns.

- 17% per cent total return in 2016, including reinvested dividends versus BCE 14%, Rogers 13%, and Quebecor 11%.

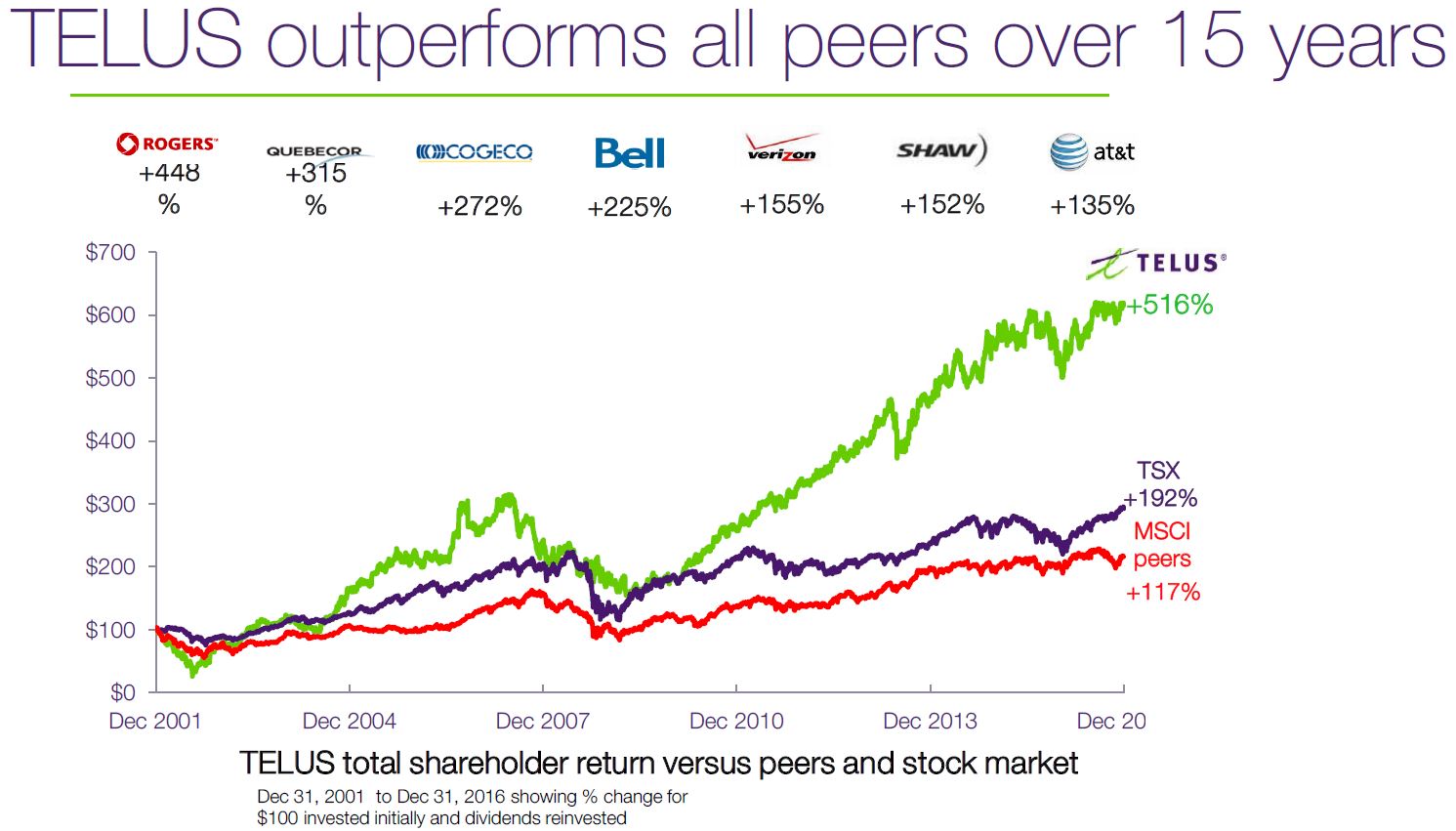

- 373% total shareholder return (2000 – early 2017). TU has outpaced its next closest global peer by 62%.

- TU has returned ~$14B ($8.7B in dividends through 19 dividend increases plus $5.2B in share purchases) to shareholders since 2004. This represents ~$24/share.

- Returned more than $1.2B to shareholders and 10% dividend growth in 2016.

- Dividend has grown on average by 10% annually since 2011. This is double that of closest telco and cable peers over 6 year period.

TELUS - Outperforming Peers and TSX since 2000

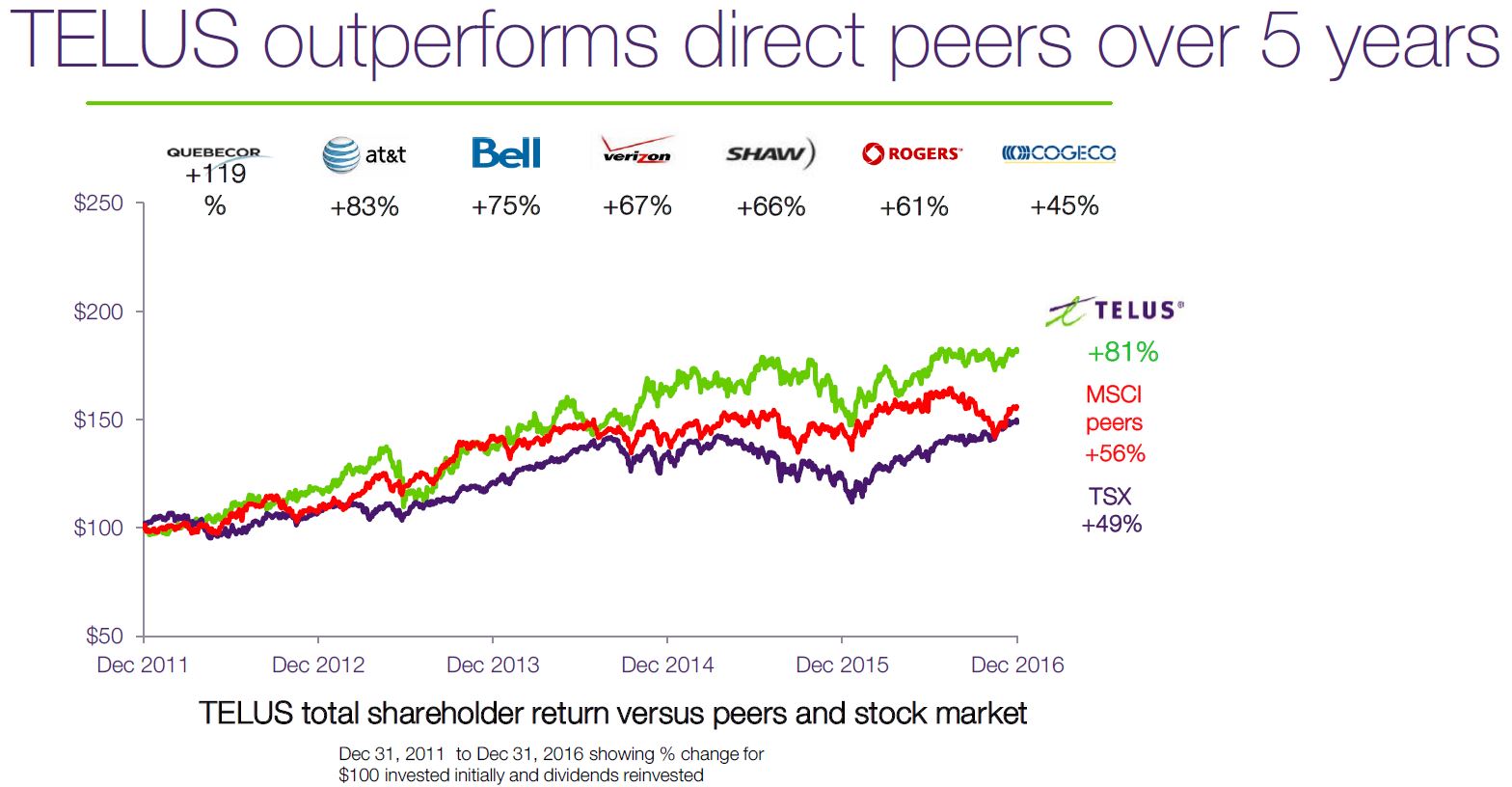

TELUS Outperforms direct peers over 5 years

TELUS Outperforms peers over 15 years

Source: TU’s April 7, 2016 Highlights of Executive Compensation – 2016 presentation.

Clearly, TU has rewarded shareholders nicely over the past several years.

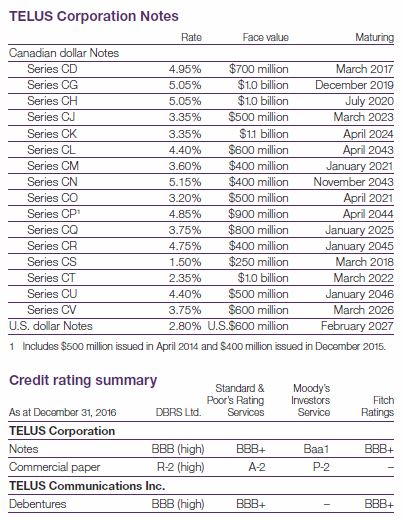

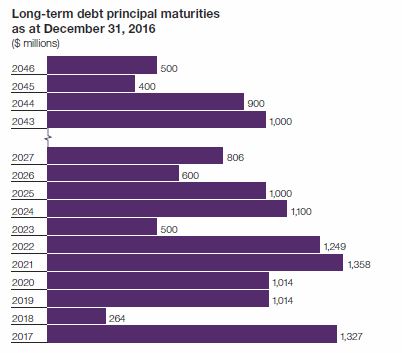

Credit Ratings and Debt Maturity Schedule

TU operates in a highly capital-intensive industry. The following schedules provide a very high level snapshot of TU’s long-term debt obligations and its credit ratings from various ratings agencies.

TELUS - Debt and Credit Ratings

TELUS - LT Debt Maturities as at December 31 2016

Source: TU’s 2016 Annual Report

NOTE: TELUS Communications Inc., a wholly owned subsidiary of TU. It is required to maintain at least a BB credit rating by DBRS Ltd., or the securitization trust may require the sale program to be wound down prior to the end of the term. TU reports that the necessary credit rating was exceeded as of February 9, 2017.

As previously noted, TU has taken advantage of the low interest rate environment to fund its CAPEX initiatives. Despite the somewhat elevated debt level, I am comfortable with the level of risk.

Q4 and FY2016 Financial Results (expressed in CDN $)

On February 9, 2017, TU reported its Q4 and FY2016 results and announced its 2017 financial targets.

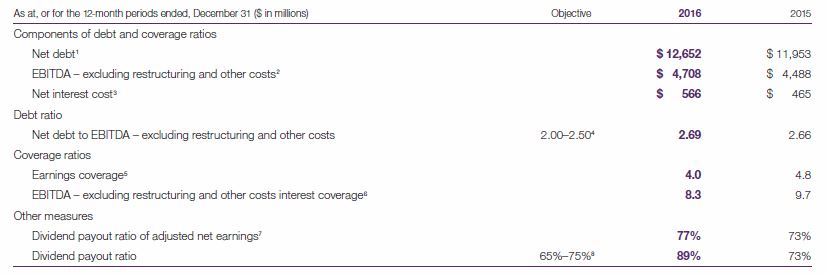

As previously noted, TU’s Debt Ratio (Net Debt to EBITDA – excluding restructuring and other costs) objective range is 2.00 – 2.50 times. The ratio as at December 31, 2016, was outside the long-term objective range. In the short term, TU may permit this ratio to go outside the objective range for long-term investment opportunities. It will, however, endeavour to return this ratio to within the objective range in the medium term.

Telus - Financial Objectives from 2016 Annual Report

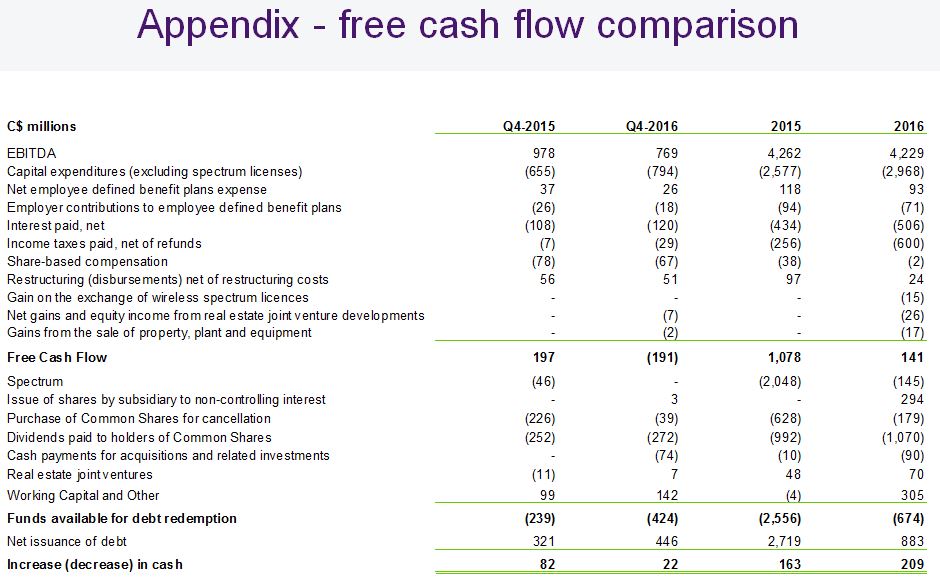

TU’s FCF was heavily impacted by a one-time employee benefits expense. $205 million and $231 million were incurred in Q4 and FY2016 mainly due to the transformative compensation expense of $305 million recorded in Q4. This transformative compensation was paid to substantially all of TU’s existing unionized and non-unionized Canadian-situated workforces.

TELUS - 2015 and 2016 FCF comparison

The one-time payment to unionized employees in Q4 represents both a one-time payment in lieu of wage increases for the period July 1, 2016 to December 31, 2018 (30 months) and a one-time payment as compensation for reductions in certain premium payments and paid time-off provisions that underpin future productivity improvements.

A similar approach with respect to salary increases was adopted for management employees. For most of current Canadian-situated management employees, there was a one-time payment in Q4 in lieu of general salary increases for 2017 and 2018.

Approximately 40% of the after-tax value of such qualifying lump-sum payments was paid in Common Shares by way of an employee benefit trust for the unionized and non-unionized workforces.

The next salary increases are planned for 2019 for substantially all of TU’s Canadian-situated employees. This arrangement will provide TU with financial flexibility to make the necessary growth and retention investments within a competitive environment.

Excluding the transformative compensation expense, employee benefits expense reflects a decrease in employee compensation of $100 million in Q4 and a $74 million decrease for FY2016.

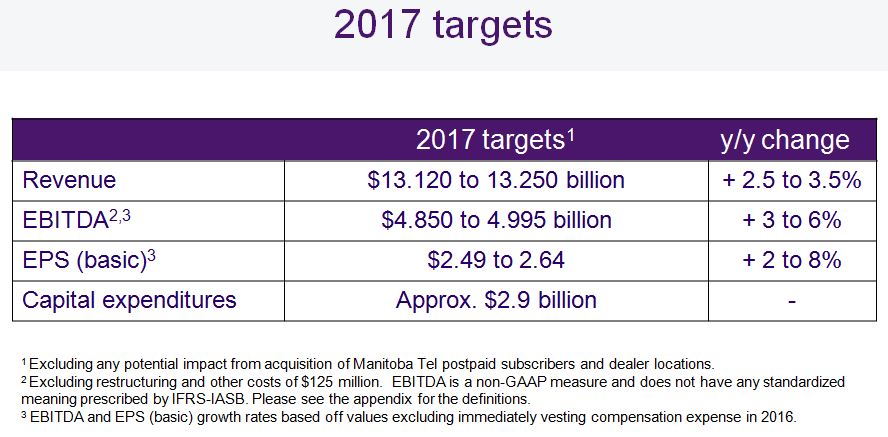

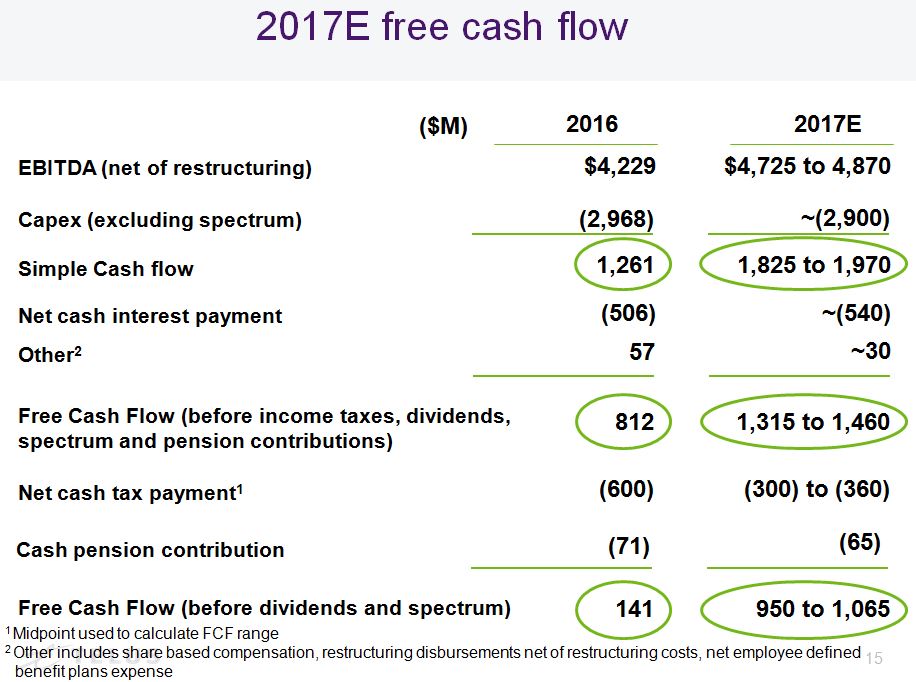

Outlook for FY2017 (expressed in CDN $)

The following screen shots were taken from TU’s February 9, 2017 investor conference call.

TELUS - 2017 targets

TELUS - 2017 estimated FCF

During Desjardins’ Industrials, Telecom & Consumer Conference held March 27, 2017, TU’s EVP and CFO reiterated TU’s 2017 targets of:

- ~5% EBITDA growth

- 7 – 10% dividend growth which is expected to occur for at least the next 3 – 4 years.

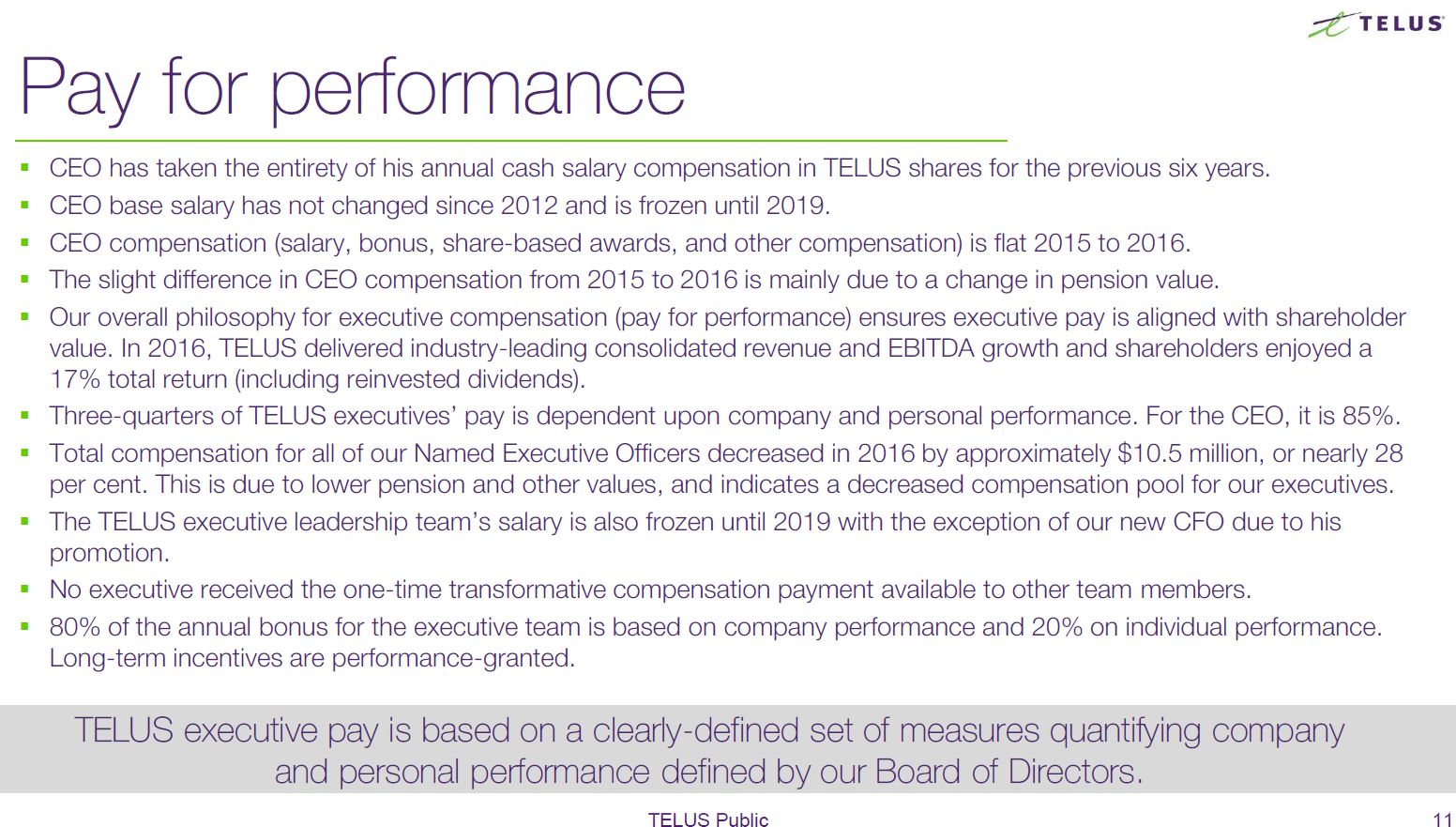

The following screen shot was obtained from TU’s Highlights of Executive Compensation - 2016 which was released April 7, 2017. It is welcoming to see that TU’s executive pay is based on a clearly-defined set of measures quantifying company and personal performance defined by the Board of Directors.

TELUS - Pay for Performance

Valuation

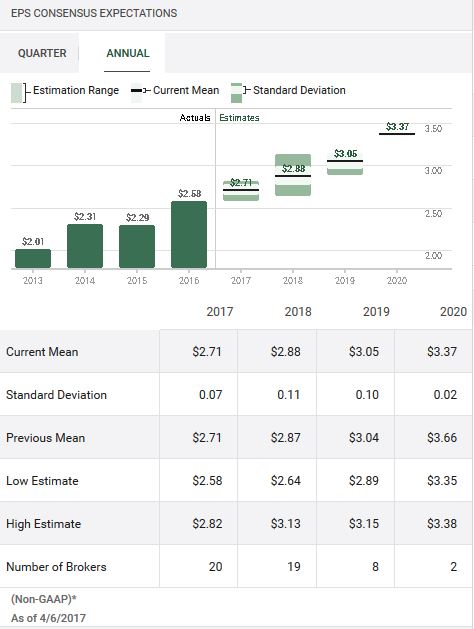

Based on my rudimentary calculations, it would appear TU is trading at a reasonable level based on 2017 estimated earnings.

The current mean adjusted EPS for FY2017 from 20 brokers is $2.71. If I use the current market price of CDN ~$44.40, I get a PE of ~16.4 which is relatively consistent with PE levels exhibited subsequent to the Financial Crisis. Using a foreign exchange conversion rate of 1.34, a reasonable US value would be ~$33.2; TU is currently trading at this level as I compose this post.

Source: TD WebBroker Annual TELUS EPS estimate

Using management’s estimated CDN $2.49 - 2.64 2017 EPS range, I get a mid-point of CDN $2.57. Using this mid-point and the current market price, TU’s PE is roughly 17.2. While definitely not a “bargain”, it would appear TU is currently fairly priced.

TU’s dividend yield is currently ~4.3% using the most recent quarterly CDN $0.48 dividend. TU, however, has been increasing its dividend by CDN $0.02 every second quarter for the last few years. Given that the April 3, 2017 dividend payment marks the second time CDN $0.48 was paid out, I envision the dividend will be increased to CDN $0.50 with the July 2017 dividend payment.

If history is any indication of what to expect, an investment at CDN ~$44.3 or USD ~$33 would provide a dividend yield of ~4.6% (based on a quarterly dividend of $0.50 for 2 quarters and $0.52 for 2 quarters). This is a reasonably attractive dividend yield from my perspective.

TELUS Corporation Stock Analysis - Final Thoughts

I have been extremely hesitant to deploy any new money given the current geopolitical conditions and what I perceive to be another period of “irrational exuberance”. In the case of TU, however, I think it is reasonably priced and it is a suitable investment based on my long-term objectives. As a result, I purchased 200 of the TSX listed shares today @ CDN $44.37. Should TU’s stock price get caught up in some form of market correction, I would very likely acquire additional shares.

I view TU as a very long-term hold as I do not envision ever requiring the need for these funds. As a result, minor daily fluctuations in TU’s market price are of little importance/concern to me. I will, therefore, be setting up the automatic reinvestment of all dividends upon receipt of these newly acquired shares.

I envision that once TU completes its current capital-intensive project to expand its fibre footprint for the purpose of having an effective 5G network, FCF will be substantial. Given this, I am willing to live with slightly elevated debt levels and lower FCF levels for the next few years.

Disclaimer: I have no knowledge of your circumstances and am not providing individualized advice or recommendations. I encourage you to conduct your own research and due diligence and to consult your financial advisor about your situation.

Disclosure: I am long TSX:T.

I wrote this article myself and it expresses my opinions. I am not receiving compensation for it and have no business relationship with any company mentioned.