Contents

Summary

Summary

- This McCormick & Company Stock Analysis is based on Q1 FY2017 financial results and outlook for the remainder of FY2017.

- MKC has increased its annual dividend for at least 30 consecutive years.

- It is the leader within the $10B global spices and seasonings industry.

- Adjusted EPS of $0.76 in Q1 2017 recently released with guidance for 2017 adjusted EPS of $4.05 - $4.13.

- I view MKC as currently overpriced. A roughly 9% drop in price from the current $97.50 to roughly $89 would be an attractive entry point.

Introduction

McCormick & Company (NYSE: MKC) is one of approximately 50 companies in the S&P 500 with more than 25 consecutive years of uninterrupted dividend increases; it has rewarded investors with annual dividend increases for just over 30 years. This places it in the exclusive Dividend Aristocrat group of companies.

In the last 5 years, MKC has returned nearly $1.7B to shareholders through dividends and share repurchases.

The reliability of an ever increasing stream of dividends has appeal to many investors. The drawback, however, is that it can lull some investors into looking beyond the underlying fundamentals of the business. This can result in some investors overpaying for a company.

McCormick’s Business

MKC was founded in 1889 when Willoughby M. McCormick and three young workers start the company in a cellar and sold their flavors and extracts door to door. The company has undergone significant transformation over the years and it now has more than 50 locations in 26 countries. Much of this growth has come from the acquisition of multiple brands and from the outright acquisition of multiple companies.

MKC manufactures, markets, and distributes spices, seasoning mixes, condiments and other products to various parts of the food industry. It markets its products to retail food, foodservice and industrial markets under a number of brands, including McCormick, Lawry's, Club House, Zatarain's, Thai Kitchen, Simply Asia, Ducros, Schwartz, Kamis, and Vahine.

In FY2016, the Consumer segment accounted for 62.5% of sales and 74.7% of operating income. About half of its consumer business is spices, herbs, and seasonings. Customers include a variety of retail outlets, including grocery, mass merchandise, warehouse clubs, and discount and drug stores. They are served directly or indirectly through distributors or wholesalers.

In addition to marketing branded products to these customers, MKC is a leading supplier of private label items, also known as store brands.

The Industrial segment accounted for about 37.5% of sales and 25.3% of segment operating income. It provides products to food manufacturers and foodservice customers. The range of products includes seasoning blends, spices and herbs, condiments, coating systems, and compound flavors.

Wal-Mart and Pepsi each accounted for roughly 11% of consolidated sales in FY2014, FY2015, and FY2016.

In FY2016, the United States accounted for 58.2% of sales, the Europe, Middle East, and Africa region (EMEA) accounted for 20.3%, and other countries accounted for 21.5%.

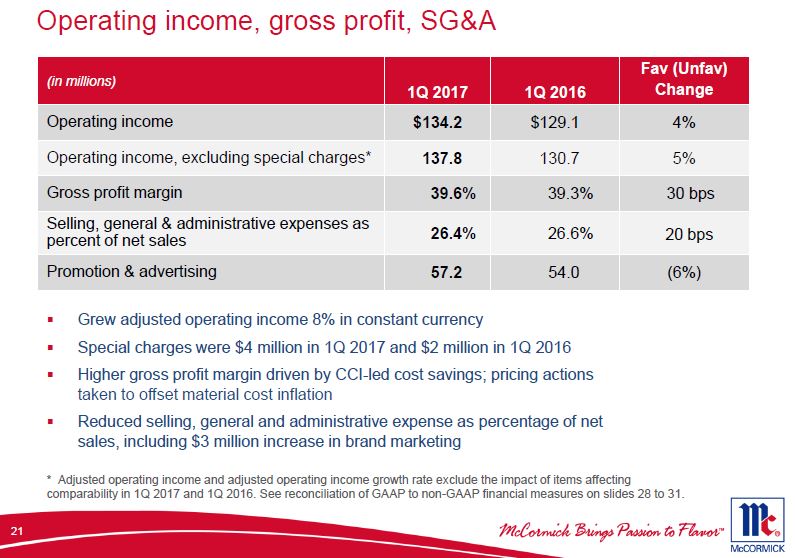

Q1 FY2017 Financial Results

On March 28, 2017, MKC reported financial results for the first quarter ended February 28, 2017 and provided its latest financial outlook for FY2017.

The following Q1 2017 results can be found in MKC’s Q1 presentation:

Net sales grew 4% with:

- Acquisitions adding 3%

- Solid growth in the industrial segment

- A double-digit increase in China

8% growth in adjusted operating income

Adjusted EPS of $0.76

MKC - Q1 2017 Gross Profit Margin

Outlook for Remainder of FY2017

MKC reaffirmed guidance for 2017 with adjusted EPS of $4.05 - $4.13 based on projected growth rates of:

- Sales 5% - 7%

- Adjusted operating income 9% - 11%

- Adjusted EPS 9% - 11%

Valuation

I, like everyone else, wish to invest in companies at a wonderful price. In this regard, I typically like a company’s PE to be sub 20. I will, however, deviate from this level if I feel a company’s competitive advantages warrant same. In the case of MKC I recognize its:

- dominance in its industry (it is the leader in the $10B global spices and seasonings industry and is 4 times the size of its next largest competitor);

- high level of brand awareness among consumers;

- highly recession-resistant business model;

- enviable dividend track record.

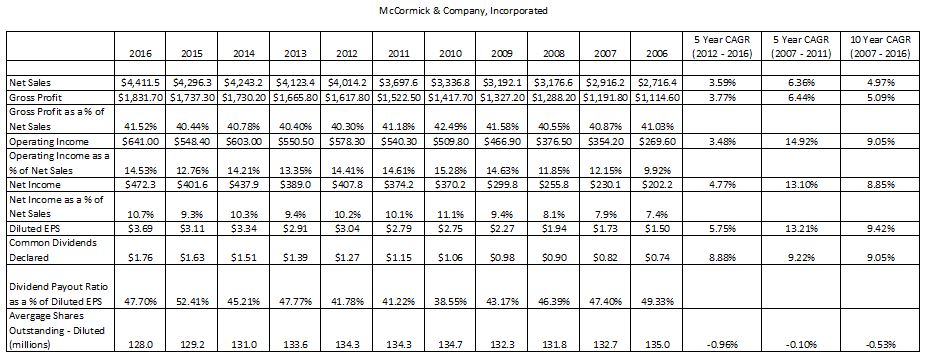

On the other hand, I draw your attention to the following MKC data for 2006 - 2016.

MKC - 5 & 10 Year CAGR 2006 - 2016

I have calculated the Compound Annual Growth Rate (CAGR) for various line items over a 10 year period as well as two 5 year periods (2007 – 2011 and 2012 – 2016). The CAGR for the most recent 5 year period has deteriorated in all metrics with the exception of shares outstanding.

MKC’s results are such that I would not categorize it as a high growth business when compared to the overall universe of publicly listed companies. While MKC certainly is a wonderful company, a PE in the mid and upper 20s is far too rich for my liking.

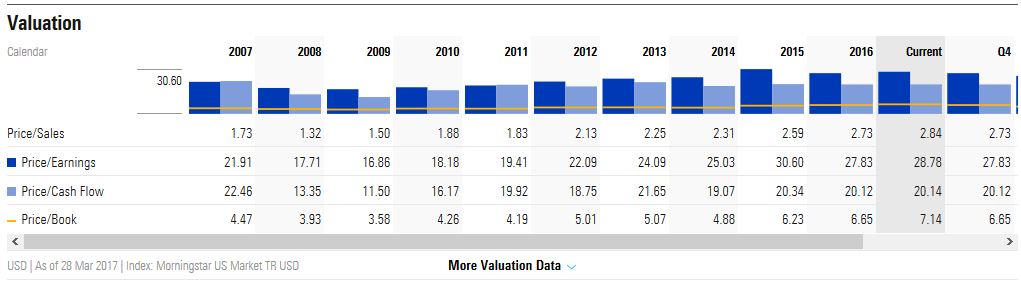

Furthermore, I draw your attention to MKC’s valuation levels for 2007 – current.

MKC - Morningstar Valuation

I recognize this period includes the Financial Crisis so the levels reflected in 2008 – 2010 are not what I would expect during typical market conditions. At the same time, MKC’s PE levels in the 2014 – current period are somewhat elevated from my perspective.

KC’s current PE is 26.5 (price just under $97.50 and FY2016’s diluted EPS of $3.69). I view a PE in the 21 – 23 range as more reasonable. If I use:

- management’s adjusted EPS of $4.05 - $4.13 forecast;

- EPS projections from several analysts of roughly $4.09 (also the mid-point of management’s estimates);

- a PE of 22.

then a price approximating $89 would be a reasonably attractive level (22 * $4.09).

MKC - TD WebBroker Annual EPS estimates

MKC currently pays a $0.47 quarterly dividend or $1.88/year. This results in a current dividend yield of ~1.9% ($1.88/$97.50).

Looking at MKC’s dividend history, I envision the quarterly dividend being increased to $0.50 with the January 2018 payment date. If this does occur, investors would end up with a dividend yield of ~2.25 using my $89 desired purchase price ($2/$89).

This $2 annual dividend represents a 49% dividend payout ratio when I use a projected adjusted EPS of $4.09. This level suggests to me that the dividend can easily be serviced/increased without undue risk.

McCormick & Company Stock Analysis - Final Thoughts

If a steadily increasing stream of dividends is of paramount importance to you, it is imperative the underlying business have the wherewithal to support these increases. In this regard, MKC fits the bill.

Other investors may view MKC’s dividend yield as being substandard and for this reason would eliminate MKC as a potential investment.

While MKC’s low dividend yield is not enough to dissuade me from acquiring shares, I am not prepared to invest in MKC at current levels.

Based on my calculations found within the Valuation section of this post, I would need MKC to retrace to the upper $80s to make it an enticing investment. Owning shares in a wonderful company appeals to me but overpaying for those shares gives me heartburn as I am not prepared to wait an inordinate amount of time to generate a reasonable return on investment.

Disclaimer: I have no knowledge of your circumstances and am not providing individualized advice or recommendations. I encourage you to conduct your own research and due diligence and to consult your financial advisor about your situation.

Disclosure: I currently have no position in MKC and am unlikely to initiate a long position within the next 72 hours.

I wrote this article myself and it expresses my opinions. I am not receiving compensation for it and have no business relationship with any company mentioned.